KEY

TAKEAWAYS

- If treasury yields get away greater, think about promoting the breakouts of bear flags and consider short-term declines as promoting alternatives

- If yields break down decrease, think about shopping for bull flags and setups.

- There’s an opportunity that yields may push greater earlier than correcting.

In our final piece, we offered a long run/secular outlook for intermediate-term Treasuries, the place we concluded that the structural break above the secular downtrend from the September 1981 excessive, coupled with the push above the November 2018 pivot @ 3.25%, has modified the long-term secular development from decrease (a bull market) to impartial. Extra work is required to maneuver the secular development from impartial to bearish. On this piece, we’ll assess how the weekly chart would possibly work together with the month-to-month chart, after which start to consider how buyers can react to numerous situations as they’re arrange over the course of the subsequent a number of weeks and months.

As a warning, my evaluation of the shorter perspective timeframe did not depart me with an actionable commerce or perhaps a clear expectation for a possible final result over the subsequent few weeks. I believe the market is able to transfer away from the present congestion zone, and I believe that the path out of the zone will present shorter-term merchants with ample alternative for entries. This evaluation has allowed me to determine the necessary chart factors/zones round which I’ll pay specific consideration to behaviors and market construction, and to outline applicable buying and selling plans.

10-12 months Treasury Yield: Annual Perspective

The chart under is the yearly perspective of the 10-12 months Treasury word (INDX).

Chart 1: Annual Chart of the 10-12 months Treasury Yield

Notice the break of the secular downtrend and the push above the three.35% pivot. It is value noting that the Shifting Common Convergence/Divergence (MACD) oscillator has turned greater for the primary time since 1985.

Bear in mind the next factors:

- The essential definition of an uptrend is a market constantly defining greater highs and better lows. As an example, a fantastic instance of a downtrend may be seen within the annual 10-year Treasury chart, the place, over a number of a long time, yields constantly made decrease lows and decrease highs, defining a really clear and apparent bull market (yields down/costs up).

- For bonds to start defining a secular bear (bond costs down/yields up), it’ll require yield to set again from a excessive pivot, outline the next low pivot, and subsequently make a substantive new excessive. From that time, you’ll be able to draw tentative annual and month-to-month trendlines, and channel projections. You may also make Fibonacci and point-and-figure worth projections. Importantly, this construction would outline a secular bear and place weekly and month-to-month momentum harmoniously with annual momentum. I anticipate this transition to happen over the subsequent 12–18 months.

- The largest query in my thoughts is whether or not final October’s 4.98% excessive print marked the terminal level for the bearish construction that has constructed for the reason that 0.40% low. I believe that’s certainly the case and that, by mid-year, yields can be falling. Nonetheless, there may be additionally an inexpensive case for one closing push greater into the stronger resistance zone at round 5.25%, earlier than subsequently setting again and defining the upper low. Given this view, the evolution of the weekly chart over the subsequent few months turns into notably necessary.

10-12 months Treasury Yield: Weekly Perspective

Beneath is a weekly chart of the 10-12 months US Treasury Yield ($TNX).

Chart 2: Weekly Chart of the 10-12 months Treasury Yields Notice the next factors of the chart:

- Bonds usually construct dependable channels and trendlines, however the transfer from 0.40% is atypical in {that a} strong trendline or channel is troublesome to seek out.

- For the reason that transfer from the low would not present a strong trendline or channel, I’m centered on the two.52–3.25% (A-B) development line. The decline from 4.98% since final October has repeatedly weakened it, and the bounce from the trendline has been very modest.

- The lack of the trendline to generate promoting (greater yields/decrease costs) means that the strain is not robust.

- It’s probably {that a} decline under the three.79% pivot would probably stretch again to the three.25% pivot, with the next probability of the world round 2.65% (retracing roughly 1/2 of the 0.40% to 4.98% transfer).

- The transfer from 3.79% has usually offered as a bull (decrease yield/greater worth) flag. Flags are normally corrective towards the development. Notice that quantity in the course of the interval has declined considerably (as can be anticipated), albeit from the extraordinarily excessive volumes that developed in the course of the transfer to final October’s excessive.

- Certainly one of my favourite patterns is the “three drives to a excessive or low.” Whereas this chart could technically qualify (3.48% –> 4.33% –> 4.98%) the push to three.48% solely barely qualifies, as it is not proportional to the primary two thrusts. This chart is doubtlessly arrange for a closing drive greater to finish the sequence, maybe into the robust resistance on the 5.25–5.35% space.

- I will even be monitoring the value for a secondary take a look at of 4.98%. A accomplished secondary take a look at would arrange for a major bull (yield down/worth up) market.

The stability of the structural proof on the weekly chart favors decrease yields, but it surely’s a detailed name and never notably actionable from these ranges.

Wanting At Momentum

The multiple-screen momentum perspective under is a fast filtering methodology I exploit. Importantly, momentum is fractal (sturdy throughout time frames and markets). I desire to derive the development by way of the tape, so I solely use the oscillators as a fast filter.

The chart under shows the annual, month-to-month, weekly, and each day charts of the 10-12 months Treasury Yield. Notice that on the chart, we transfer again to yield once more.

Chart 3: Annual, Month-to-month, Weekly, and Each day Charts of the 10-12 months Treasury Yield

An necessary level to recollect: Rising yields = lower cost.

- Yearly momentum has turned towards greater yield/lower cost.

- Month-to-month momentum has turned towards decrease yield/greater worth. A slight damaging divergence has shaped, and the month-to-month is at odds with the yearly.

- Weekly momentum is combined/impartial, however making an attempt to show to greater yield/lower cost. This wrestle across the zero line means that behaviors over the subsequent few weeks will probably outline the path of the subsequent 25–50 foundation level motion.

I’m most within the weekly development (in charges, the weekly perspective is a very powerful), so I usually defer to the development of 1 greater diploma. On this case, the month-to-month is on a decrease yield/greater worth sign and is simply now shifting into the MACD quadrant, the place vital declines (in yields) are more likely to happen; Odds are higher that the weekly will even flip to decrease yield/greater worth to be in concord. However, once more, the proof is combined. Typically, you simply must let the value motion evolve earlier than drawing a strong conclusion.

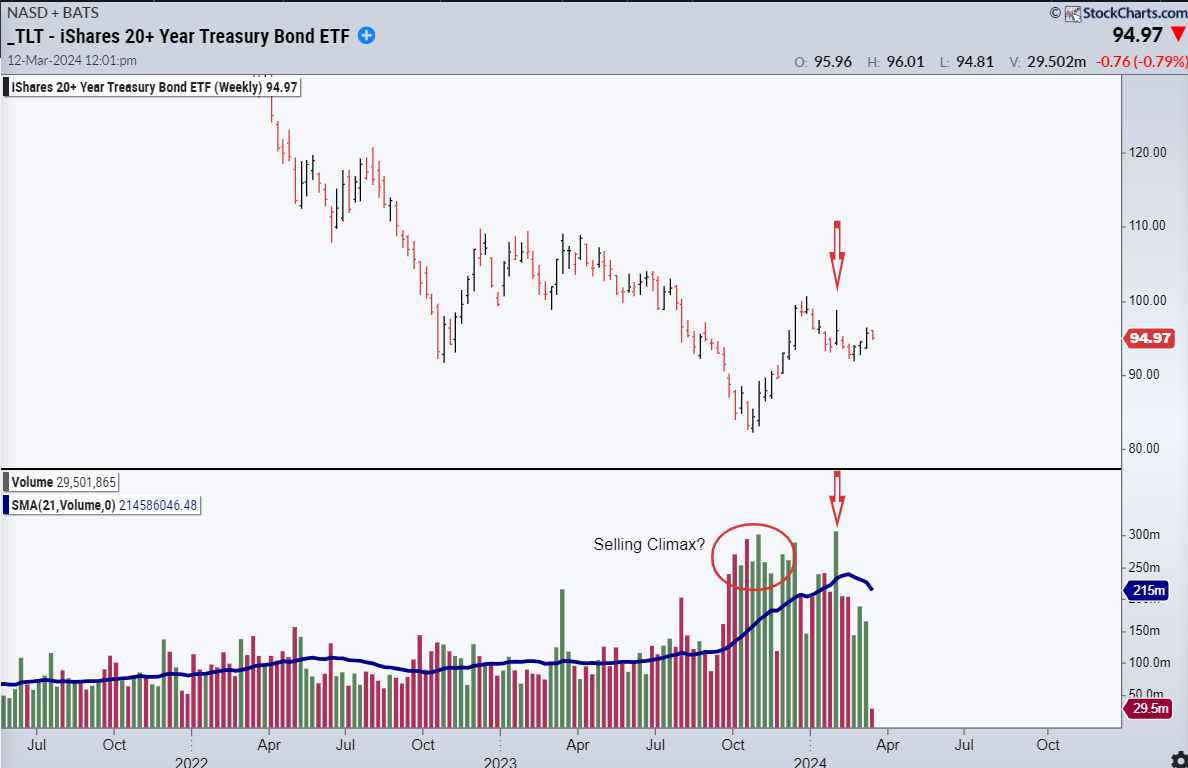

A Weekly Perspective of TLT (Bond ETF)

Some necessary factors re. quantity:

- Since we’re viewing the iShares 20+ 12 months Treasury Bond Fund (TLT), we’re worth (a downtrend is a bear market) relatively than working with yield. It’s because the yield indices we’re utilizing don’t have any reported quantity. The caveat right here is that, in my skilled capability, I desire to make use of futures quantity, as they higher symbolize institutional-rate buyers, whereas TLT has a distinctly retail focus.

- The proof between futures and ETF quantity is conflicting. TLT confirmed clear indicators of short-term capitulation final October, however didn’t show a traditional promoting climax.

- Futures are extra ambiguous, with no clear surge in quantity, however worth behaviors are extra in step with a promoting climax.

- For the reason that October low, the quantity typically has remained fairly excessive, and the upward progress is comparatively modest. The poor outcome for the hassle expended means that the market continues to run into high quality provide. The identical worth/quantity relationship can also be current in futures.

- Notice the speedy fall in quantity over the past three to 4 weeks because the market tilted greater. That is in step with a bear flag or pennant.

- Lastly, word the quantity spike (arrow) as sellers leaned into the market a couple of weeks in the past. There are nonetheless strong-handed sellers prepared to hit bids into power.

I believe the stability of proof means that the market made a promoting climax in October. That climax will probably maintain for many of this 12 months, however could also be retested.

10-12 months Treasury Yield Each day

{kind=link}

Chart 5: Each day Chart of 10-12 months Treasury Yield

Notice the next factors:

- Seasonal Tendency. Yields are likely to set vital intermediate highs early within the 12 months earlier than declining into mid-year. We’re close to the top of the bearish (yields up/costs down) annual interval. This might counsel a push decrease (yield down/worth up).

- Yields have struggled to maneuver away from the uptrend (A/B) however usually have constructed a bull (costs up/yields down) flag. Now, they’re being squeezed between the interior resistance (grey lateral trendline) and the A-B channel backside. From this attitude, bears (yields greater/costs decrease) have a bonus.

- If the market breaks greater from this zone, the place would resistance materialize? If yields breakout greater from this zone, there is not a lot resistance between 3.50% and final 12 months’s @ 4.89% excessive. Above 4.89%, 5.25–5.35% is an inexpensive goal.

- If the market breaks decrease from this zone, a strong assist confluence exists within the 3.23–3.30% zone. However it’s extra probably the 0.50–0.618 retracement zone within the 2.15–2.70% zone can be in play. This might probably come as the results of an financial recession.

The Backside Line

The subsequent few weeks ought to symbolize a major juncture within the each day and doubtlessly the weekly chart. The market has usually been consolidating over the past a number of months, and the sample breakout could possibly be significant. For shorter-term merchants, the path out of the consolidation will probably outline the path of journey into the autumn. In different phrases, it’s a go-with.

- If yields get away greater, I’ll probably start promoting the breakouts of bear (costs down/yields greater) flags and can view short-term declines in yields as promoting alternatives. If decrease, I’ll probably be a purchaser of bull flags and setups (yields down/costs greater) as they develop.

- If the market falls away from the trendline with velocity, the primary strong assist there may be discovered within the 3.79% zone.

- I proceed to see a not-trivial likelihood of 1 final push greater into the 5.25–5.50% zone, earlier than starting a serious weekly and month-to-month perspective correction (yield down/worth up) that ultimately makes the upper low. And whereas I see a bonus to being usually bullish over the subsequent few months (falling yields, rising costs), the evaluation is tentative, with solely a small near-term benefit to the commerce. In my buying and selling, I’d think about it non-actionable with out further worth/quantity improvement or affordable construction to commerce towards.

In deference to my macro work and enterprise cycle work, I can be a greater purchaser of bullish inflections within the weekly chart over the subsequent few months, as I totally anticipate a major financial slowdown to grow to be the top of the 12 months.

Disclaimer: Shared content material and posted charts are meant for use for informational and academic functions solely. The CMT Affiliation doesn’t provide, and this data shall not be understood or construed as, monetary recommendation or funding suggestions. The data offered is just not an alternative choice to recommendation from an funding skilled. The CMT Affiliation doesn’t settle for legal responsibility for any monetary loss or injury our viewers could incur.

Good Buying and selling.

Stewart Taylor, CMT

Chartered Market Technician

Stewart Taylor retired from Eaton Vance Administration in January 2020 after a 40-year profession in US fastened earnings with an emphasis on technical evaluation and relative worth investing. He joined Eaton Vance because the Senior Dealer for the Funding Grade Mounted Revenue workforce in 2005. Throughout his tenure, he was a portfolio supervisor for institutional separate accounts and mutual funds, managed the workforce’s inflation belongings, and was the workforce’s strategist for length, relative worth, and financial positioning. From 1992 to 2005, he offered non-public investing and buying and selling session to institutional purchase aspect, broker-dealers, and hedge funds.

Study Extra