Having a Roth IRA account in place for retirement is a accountable plan for the long run. In any case, you wouldn’t wish to fear about your monetary safety if you’ve lastly reached an age to benefit from the fruits of your labor.

For those who’re contributing to the sort of retirement account, you is likely to be questioning what Roth IRA withdrawal guidelines are in place. Fortunately, tax specialists can be found to assist reply any questions alongside the best way, particularly with a subject so complicated.

You’re all the time eligible for tax- and penalty-free withdrawals on contributions, however you should meet sure Roth IRA guidelines for withdrawal to withdraw earnings. There are guidelines for withdrawal each on the time of retirement and sooner should you had been to want extra cash instantly. Use this information to study extra in regards to the withdrawal guidelines for Roth IRAs.

Some key takeaways for a Roth IRA withdrawal embrace:

- Roth IRA distributions on contributions will be taken at any time, each tax- and penalty-free.

- Roth IRA distributions on earnings will be taken each tax- and penalty-free when:

- You’ve reached the age of 59.5, and

- Your Roth IRA account has been open for 5 years

- The taxes and penalties is likely to be prevented throughout sure conditions, together with buying your first dwelling, beginning or adoption, or protecting school training bills.

Hold studying to study extra in regards to the Roth IRA retirement account, together with detailed data on withdrawals and sure limits on contributions.

Are you allowed to withdraw Roth IRA contributions?

It’s necessary to make this distinction when speaking about guidelines for withdrawing from a Roth IRA: You possibly can withdraw contributions which were made to your Roth IRA at any time, each tax- and penalty-free. Nonetheless, relying on if you withdraw your Roth IRA earnings, you might need to pay taxes and penalties.

For those who’re withdrawing Roth IRA earnings, to keep away from triggering a ten% early withdrawal penalty, you should be at the very least 59 ½ years outdated, and your account should be open for no less than 5 years. When you’ve reached this level, you may make tax- and penalty-free withdrawals in your Roth IRA earnings.

Roth IRA Contributions and Earnings

It’s necessary to make this distinction when speaking about Roth IRA withdrawal guidelines: You possibly can withdraw contributions which were made to your Roth IRA at any time, each tax- and penalty-free. Nonetheless, relying on if you withdraw your Roth IRA earnings, you might need to pay taxes and penalties.

What are certified vs. nonqualified distributions?

Certified and nonqualified distributions decide whether or not there are taxes and penalties if you withdraw earnings out of your Roth IRA. For certified Roth IRA distributions, you should be at the very least 59 ½ years outdated, and your Roth IRA should be at the very least 5 years outdated.

For those who resolve to make a withdrawal on Roth IRA earnings earlier than your account has been open for 5 years, you will have to pay revenue taxes and a ten% penalty.

Needless to say sure circumstances can defend you from Roth IRA penalties and taxes. For instance, you possibly can withdraw as much as $10,000 should you’re buying your first dwelling.

What are the Roth IRA withdrawal guidelines?

Earlier than withdrawing from a Roth account, it’s vital to know the principles and limitations related to distributions. Contributions to a Roth IRA will not be tax-deductible, although earnings can develop tax-free. Certified distributions are each tax and penalty-free, whereas non-qualified distributions will incur penalties relying on various factors.

Hold the next Roth IRA withdrawal guidelines in thoughts to keep away from a ten% early withdrawal penalty:

- Withdrawals should be taken after you’ve turned 59.5 years outdated.

- Withdrawals should be taken after your five-year ready interval.

There are specific exceptions to the early withdrawal penalty — these embrace distributions to fund sure bills, like:

- Buying your first dwelling

- Delivery

- Adoption

- School tuition

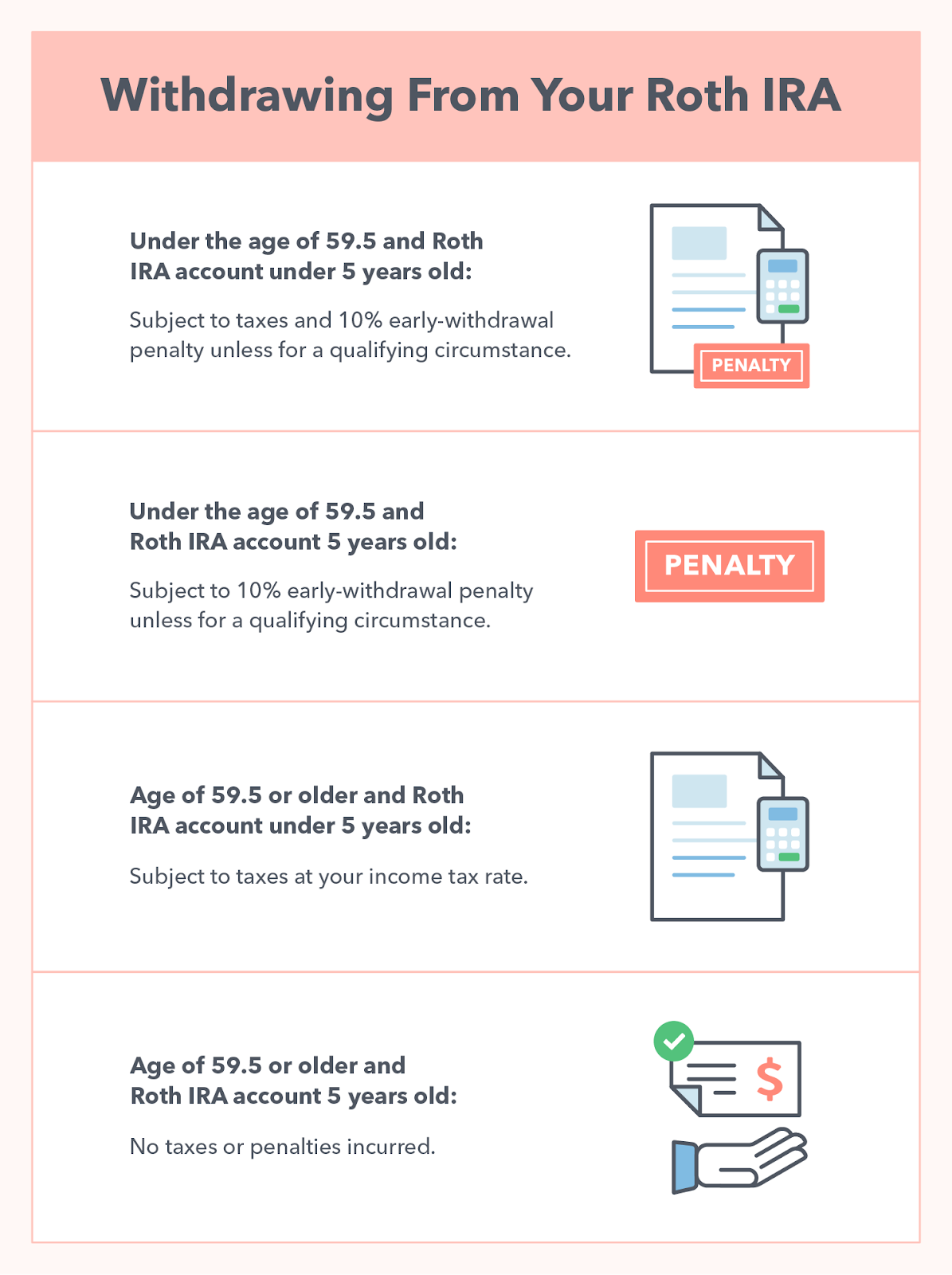

Roth IRA withdrawal guidelines for these underneath the age of 59.5

For those who’re underneath the age of 59.5, you may must pay taxes and penalties in your earnings that you simply’d wish to withdraw out of your Roth account. Keep in mind that you would be able to withdraw your contributions at any time with out taxes or penalty; these solely apply to the earnings in your account.

- For those who’ve had your Roth IRA for lower than 5 years: You can be topic to each your commonplace revenue tax price and a ten% penalty in your earnings distribution. You may be capable to avoid the ten% penalty should you use the funds for one of many following conditions:

- Everlasting incapacity

- First dwelling buy

- Certified training bills

- The beginning or adoption of a kid

- Considerably equal periodic funds

- Unreimbursed medical bills or medical insurance should you lose your job

- For those who’ve had your Roth IRA for greater than 5 years: You received’t be topic to taxes, however you’ll incur a ten% early-withdrawal penalty. You may be capable to keep away from the ten% penalty should you meet one of many following circumstances:

- Everlasting incapacity

- First dwelling buy

- Certified training bills

- The beginning or adoption of a kid

- Considerably equal periodic funds

- Unreimbursed medical bills or medical insurance should you lose your job

Roth IRA withdrawal guidelines for these over the age of 59.5

For those who’ve reached the age of 59.5, you’ve met half of the necessities to withdraw your Roth IRA earnings each tax- and penalty-free. The second half of the requirement is the Roth IRA 5-Yr Rule.

- For those who’ve had your Roth IRA for lower than 5 years: Your earnings shall be topic to taxes at your regular tax price, however you received’t be topic to the ten% penalty.

- For those who’ve had your Roth IRA for greater than 5 years: You possibly can withdraw your Roth IRA earnings with no taxes and no penalties.

Based mostly on the above eventualities, the perfect time to withdraw out of your Roth IRA account is if you’ve had your account for 5 years or extra and have reached the age of 59.5. It will make it easier to profit from your contributions and earnings.

The distributions that you simply take when you’ve reached each milestones (or a qualifying occasion) are often known as certified distributions. In any other case, the distributions are thought of non-qualifying distributions.

Exceptions to the Roth IRA withdrawal guidelines

Whereas there are a number of guidelines for Roth IRA withdrawals, there are additionally exceptions. Below sure circumstances, you might be able to make tax- and penalty-free withdrawals.

For those who’re buying your first dwelling with earnings out of your Roth IRA, you possibly can withdraw as much as $10,000 out of your Roth IRA with out going through penalties. Needless to say this penalty-free withdrawal solely applies if you’re shopping for your first dwelling.

You may as well use Roth IRA earnings to pay for bills associated to increased training, together with school tuition and different charges. So long as you’re protecting certified training bills, you don’t have to fret about a further 10% penalty however usually early withdrawals of earnings are topic to revenue taxes.

Roth IRA five-year rule

With a Roth IRA account, there are two necessities that should be met should you want to withdraw your earnings with out owing any taxes and penalties: You should be 59.5 years of age or older, and you should fulfill the five-year rule.

So, what precisely is the five-year rule? This rule states that there should be 5 years between the time you make your first contribution and the time that you simply withdraw your earnings. This rule applies no matter age, even should you had been to hit the age of 59.5 within the meantime.

For those who select to withdraw your Roth IRA earnings earlier than you’ve glad this five-year rule, count on to pay taxes on the withdrawal in addition to a ten% Roth IRA early-withdrawal penalty.

Roth IRA contribution limits

The annual quantity that you simply’re allowed to contribute to your Roth IRA is proscribed by the revenue that you simply earn. The annual Roth IRA contribution restrict is $6,500 for 2023; this modifications to $7,500 should you’re 50 or older. For 2024, the Roth IRA contribution restrict is $7,000 (or $8,000 in case you are 50 or older). In different phrases, your contributions to your Roth IRA account can’t exceed this restrict.

Roth IRA revenue limits

Equally to the contribution limits, sure limits on revenue exist with regard to a Roth IRA account.

- For those who’re a single filer or head of family: Your Modified Adjusted Gross Earnings (MAGI) should be lower than $153,000 in 2023 ($161,000 in 2024).

- For those who’re a joint filer: Your MAGI should be lower than $228,000 in 2023 ($230,000 in 2024).

So, what do these numbers imply? In case your revenue exceeds the higher restrict, you possibly can’t contribute to a Roth IRA account. Because the amount of cash you make will increase, your most contribution quantity decreases.

Under is further data on how the bounds for 2023 and 2024 are calculated:

- Single or head of family submitting standing:

- 2023 MAGI: lower than $138,000

- Most annual contribution: $6,500 (or $7,500 if age 50 or older)

- 2024 MAGI: lower than $146,000

- Most annual contribution: $7,000 (or $8,000 if age 50 or older)

- 2023 MAGI: $138,000 to $152,999

- Most annual contribution: Lowered

- 2024 MAGI: $146,000 to $160,999

- Most annual contribution: Lowered

- 2023 MAGI: $153,000 or extra

- No contribution allowed

- 2024 MAGI: $161,000 or extra

- No contribution allowed

- 2023 MAGI: lower than $138,000

- Married submitting collectively or qualifying widower submitting standing:

- 2023 MAGI: lower than $218,000

- Most annual contribution $6,500 ($7,500 if age 50 or older)

- 2024 MAGI: lower than $230,000

- Most annual contribution $7,000 ($8,000 if age 50 or older)

- 2023 MAGI: $218,000 to $227,999

- Most annual contribution: Lowered

- 2024 MAGI: $230,000 to $239,999

- Most annual contribution: Lowered

- 2023 MAGI: $228,000 or extra

- No contribution allowed

- 2024 MAGI: $240,000 or extra

- No contribution allowed

- 2023 MAGI: lower than $218,000

As you possibly can see, Roth IRA accounts usually favor these in a decrease revenue bracket, as they’ll contribute probably the most. As you climb the revenue bracket stage, the quantity that you would be able to contribute evens out to zero.

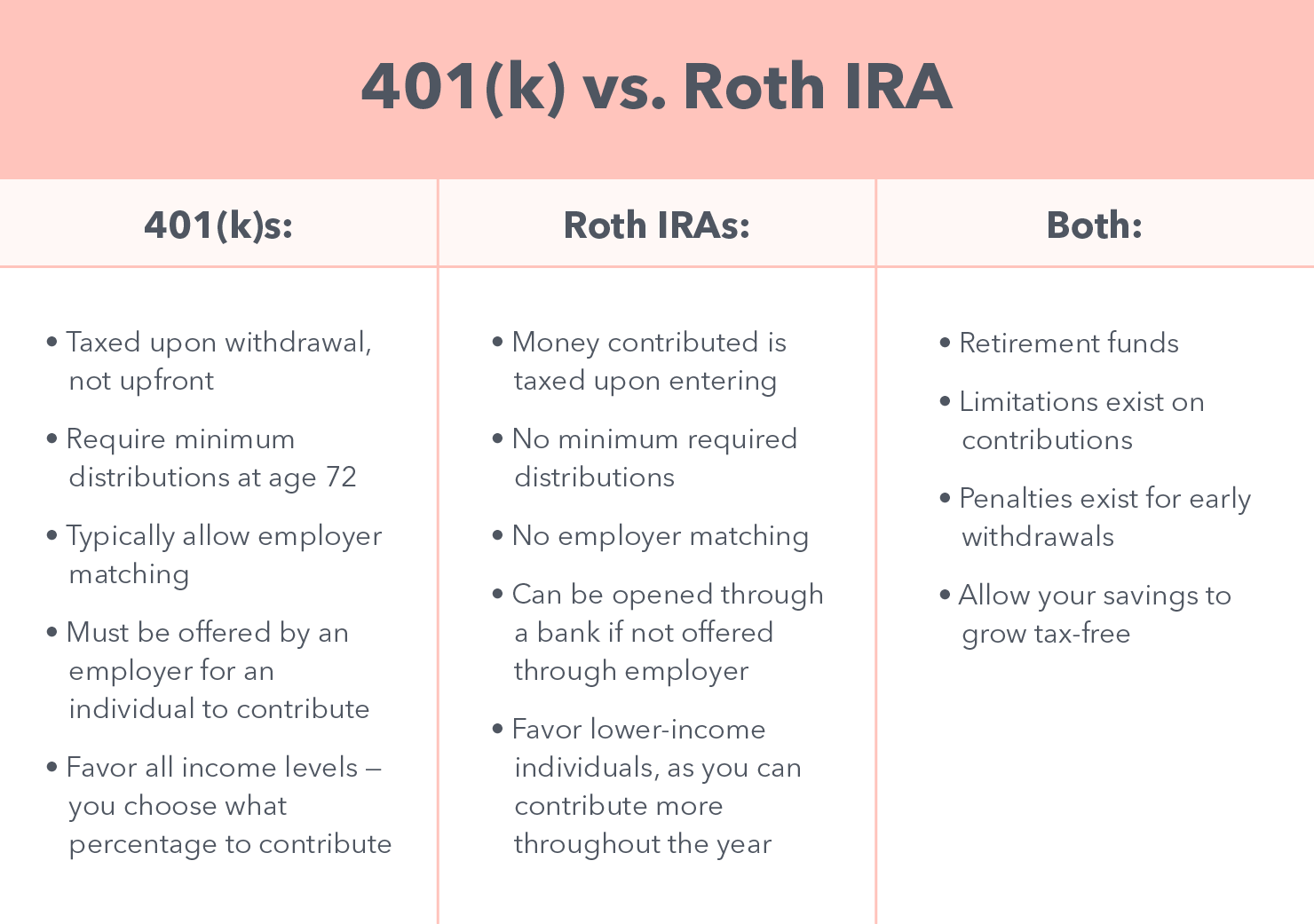

401(okay) vs. Roth IRA

When discussing retirement plans, you may hear about each Roth IRAs and conventional 401(okay)s. Whereas these are each nice choices that will help you save for retirement, there are many variations between these two plans that make them distinctive.

A standard 401(okay) plan is tax-deferred, that means that the cash that’s contributed shouldn’t be taxed upon getting into however is taxed when distributed. As well as:

- Employers can provide to match a proportion of your contribution and add it to your 401(okay) account.

- 401(okay)s require minimal distributions beginning at age 72.

- Employers should provide the 401(okay) program to ensure that a person to contribute.

Roth IRA plans are a little bit completely different, particularly in the best way that taxes work. Roth IRA contributions are taxed as they enter the plan, making them untaxed as they’re withdrawn. As well as:

- Roth IRAs will be opened even when an employer doesn’t provide them.

- There aren’t any required minimal distributions to a Roth IRA.

- Roth IRAs favor these making a decrease revenue, as they’ll contribute extra per yr.

Though there are a number of variations, there are a number of methods they’re the identical. For starters, limitations exist on contributions, although the restrict for 401(okay) is way increased. As well as, each plans impose a penalty for a nonqualified early withdrawal.

Execs and cons of taking a Roth IRA withdrawal

Whereas it is likely to be tempting to take a Roth IRA withdrawal, ideally, you need to wait to withdraw till retirement. At this level, you’ve seemingly glad each the five-year rule and the minimal age of 59.5. In any case, the longer you wait, the extra you possibly can maximize your general contributions and earnings. This supplies you with more cash for the long run with out paying any potential penalties.

It’s necessary to notice earlier than you withdraw from a Roth IRA that cash can’t be repaid to the account. As soon as it’s gone, that cash and any earnings that may have include it are additionally gone.

If there’s a scenario the place you must withdraw out of your Roth IRA, it’s finest to think about the professionals and cons first. By withdrawing your Roth IRA, you possibly can keep away from paying curiosity on a mortgage. This protects you cash in the long term.

As well as, you possibly can all the time take out your contributions each tax and penalty-free and, in some circumstances, withdraw your earnings penalty-free as properly. This will likely offer you quick money reduction if you want it probably the most.

Earlier than withdrawing, nonetheless, it’s necessary to know there are a number of drawbacks as properly. First, the cash can’t be repaid to the account, that means that you simply’re lacking out on future tax-free development. As well as, should you had been to withdraw your earnings, you’ll incur taxes and penalties should you haven’t had the account for 5 years and also you’re underneath 59.5 years outdated.

Lastly, and perhaps most significantly, any cash you withdraw now received’t be accessible to you later in life if you retire. This may make this example financially troublesome for you.

Do I’ve to report my Roth IRA withdrawal on my tax return?

Roth IRA contributions are made with after-tax {dollars}, and people contributions aren’t tax-deductible. Certified distributions additionally aren’t thought of taxable revenue. So that you received’t report Roth IRA contributions or certified distributions in your tax return. Nonetheless, should you obtain a non-qualified distribution out of your Roth IRA you’ll have to report that distribution to the IRS. This is likely one of the causes Roth IRAs are such a well-liked retirement choice.

The quick reply is that you simply don’t should report contributions in your tax return.

Alleviate stress with tax assist

Understanding Roth IRA withdrawal guidelines doesn’t should be a troublesome course of. Meet with a TurboTax Full Service skilled who can put together, signal, and file your taxes. That method, you will be 100% assured your taxes are executed proper.

It doesn’t matter what strikes you made final yr, TurboTax will make them rely in your taxes. Whether or not you wish to do your taxes your self or have a TurboTax skilled file for you, we’ll be sure you get each greenback you deserve and your largest attainable refund – assured.

{kind=link}