{kind=link}

After consolidating for many of the week, the markets prolonged their upmove and ended at yet one more file lifetime excessive. Up to now 4 out of 5 classes, the markets had been seen consolidating and staying beneath restricted corrective retracement. Nonetheless, they did discover themselves taking help on the short-term 20-Day MA and rebounded from there. On a weekly foundation, whereas the markets consolidated within the earlier week, this time, they inched greater. The buying and selling vary additionally widened; the index oscillated in a 479.60 factors vary over the previous 5 days. Lastly, the benchmark index closed with a internet acquire of 183.75 factors (+0.85%).

From a technical standpoint, the markets are as soon as once more at an important juncture. The Choices information counsel that the markets might have opened up some extra room for themselves on the upside. Nonetheless, the general construction of the charts additionally means that the Index is very overextended and continues to stay susceptible and weak to profit-taking bouts from present ranges. With the continuing pattern staying robust, the one methodology to strategy such markets is to maintain buying and selling/following the pattern whereas successfully trailing the stop-losses greater. Volatility additionally inched greater; India Vix rose by 3.72% to 13.10.

The approaching week is more likely to see a secure begin because the markets enter uncharted territory as soon as once more. Count on the degrees of 21950 and 22185 to behave as potential resistance. The helps exist at 21745 and 21580 ranges.

The weekly RSI stands at 77.15; it stays mildly overbought. The RSI has additionally fashioned a brand new 14-period excessive however stays impartial with out exhibiting any divergence in opposition to the value. The weekly MACD is bullish and stays above its sign line.

A candle with a protracted decrease shadow has emerged. The prior candle to this was a spinning prime or a Doji. Such candles after a sustained upmove proceed to carry the potential of stalling the pattern at any cut-off date. Nonetheless, in the identical breadth, candles are by no means traded in isolation and one should all the time look out for affirmation.

The sample evaluation on the weekly charts reveals that the Nifty continues to increase its breakout. The index had damaged out from a rising channel when it crossed above 20800 ranges. This breakout continues to take the markets greater; nevertheless, on the identical time, the Nifty stays closely overextended on charts. The closest sample help stands at 21000, the 20-week MA is 1679 factors beneath the present ranges at 20215. The 50-week MA is at 19112; a superb 2792 factors from the present ranges. With the closest sample helps standing at nearly 900 factors from the present ranges, any imply reverting strikes shall be important to their extent.

All in all, the strategy to strategy the markets any longer is just about easy. There isn’t a query of shorting the markets or going in opposition to the pattern. Nonetheless, given the over-extended nature of the markets, it’s of paramount significance that one retains trailing their stoplosses successfully within the method that the key portion of the earnings stand protected. New purchases should be stored defensive; it’s anticipated that sectors like FMCG, Pharma, and so forth., might do nicely going forward from right here. Whereas retaining leveraged exposures beneath management, a extremely selective strategy is suggested for the day.

Sector Evaluation for the approaching week

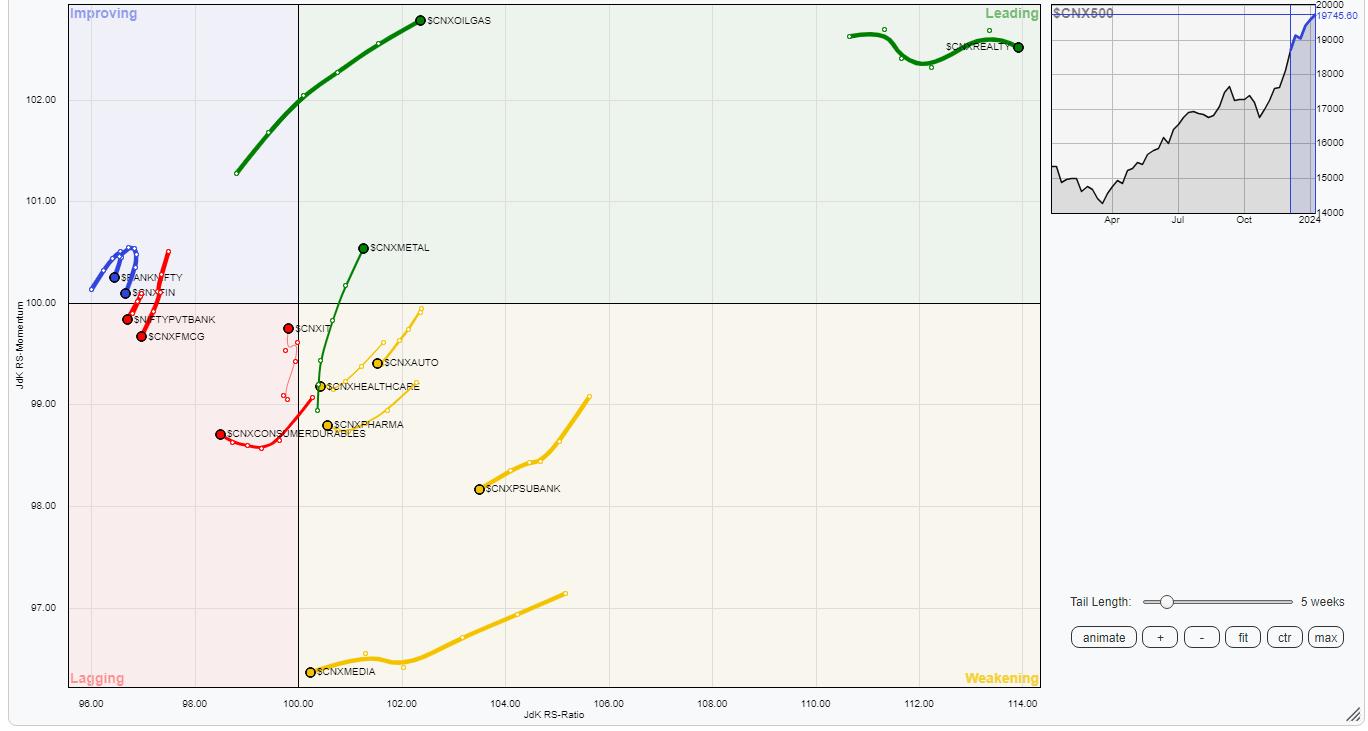

In our have a look at Relative Rotation Graphs®, we in contrast numerous sectors in opposition to CNX500 (NIFTY 500 Index), which represents over 95% of the free float market cap of all of the shares listed.

Relative Rotation Graphs (RRG) reveals Nifty Power, Commodities, Realty, PSE, and Steel Index firmly positioned contained in the main quadrant. The Infrastructure Index can also be contained in the main quadrant. These teams are more likely to proceed to comparatively outperform the broader markets.

The Nifty Media, PSU Financial institution, Pharma, and Auto Indices proceed to pull whereas staying contained in the weakening quadrant. Although particular person performances from these teams could also be seen, the relative efficiency might take the again seat. The MidCap 100 index reveals good enchancment in its relative momentum whereas staying contained in the weakening quadrant.

The IT Index reveals sharp enchancment in its relative momentum whereas staying contained in the lagging quadrant. Alternatively, Nifty Consumption and FMCG has rolled contained in the lagging quadrant given their relative underperformance in opposition to the broader markets.

The Nifty Financial institution and Companies Sector index are contained in the enhancing quadrant; nevertheless, they seem like giving up on their relative momentum.

Vital Notice: RRG™ charts present the relative power and momentum of a gaggle of shares. Within the above Chart, they present relative efficiency in opposition to NIFTY500 Index (Broader Markets) and shouldn’t be used instantly as purchase or promote alerts.

Milan Vaishnav, CMT, MSTA

Consulting Technical Analyst

www.EquityResearch.asia | www.ChartWizard.ae

Milan Vaishnav, CMT, MSTA is a capital market skilled with expertise spanning near 20 years. His space of experience consists of consulting in Portfolio/Funds Administration and Advisory Companies. Milan is the founding father of ChartWizard FZE (UAE) and Gemstone Fairness Analysis & Advisory Companies. As a Consulting Technical Analysis Analyst and along with his expertise within the Indian Capital Markets of over 15 years, he has been delivering premium India-focused Unbiased Technical Analysis to the Shoppers. He presently contributes every day to ET Markets and The Financial Occasions of India. He additionally authors one of many India’s most correct “Each day / Weekly Market Outlook” — A Each day / Weekly Publication, at present in its 18th yr of publication.