{kind=link}

Notice to the reader: That is the seventh in a sequence of articles I am publishing right here taken from my e-book, “Investing with the Development.” Hopefully, you can see this content material helpful. Market myths are usually perpetuated by repetition, deceptive symbolic connections, and the whole ignorance of info. The world of finance is filled with such tendencies, and right here, you may see some examples. Please needless to say not all of those examples are completely deceptive — they’re typically legitimate — however have too many holes in them to be worthwhile as funding ideas. And never all are straight associated to investing and finance. Take pleasure in! – Greg

“Those that have information do not predict. Those that predict haven’t got information.” — Lao Tzu

In order that there could be no confusion, I need to state my sincere heartfelt opinion on forecasting: I adamantly consider there isn’t a one who is aware of what the market will do tomorrow, subsequent week, subsequent month, subsequent yr, or at any time sooner or later—interval.

Hindsight is a superb device to make use of with a view to know why one thing might need occurred up to now, however not often is the trigger recognized in the course of the occasion itself. The prediction enterprise is gigantic. William Sherden, in The Fortune Sellers, claimed that in 1998 the prediction enterprise accounted for $200 billion value of principally faulty predictions. Are you able to think about with the expansion of the Web and globalization, what that business is immediately? Scary! As Oaktree Capital Administration’s Howard Marks says, “You can not predict, however you’ll be able to put together.”

Dean Williams, then-senior vice chairman of Batterymarch Monetary Administration, gave a keynote speech on the Monetary Analysts Federation Seminar in August 1981, the place he made some nearly prophetic feedback about investing which can be as true immediately as they had been then. He spoke concerning the relationship between physics and investing, however I’ve beforehand mentioned that topic. One other remark was, “Probably the most consuming makes use of of our time, in actual fact, has been accumulating data to assist us make forecasts of all these issues we expect we’ve got to foretell. The place’s the proof that it really works? I have been searching for it. Actually! Listed here are my conclusions: Confidence in a forecast rises with the quantity of data that goes into it. However the accuracy of the forecast stays the identical.” Afterward, he added, “It is you can be a profitable investor with out being a perpetual forecaster. Not solely that, I can inform you from private expertise that one of the crucial liberating experiences you’ll be able to have is to be requested to go over your agency’s financial outlook and say, ‘We do not have one.'” He goes on to speak about utilizing easy approaches versus advanced ones, delving into the truth that in addition they should be constant approaches. This can be a must-read; you’ll find it from an Web search on Dean Williams Batterymarch.

Sherden states that the title “second oldest occupation” often goes to legal professionals and consultants, however prognosticators are the rightful homeowners. Early information from 5,000 years in the past present that forecasting was practiced within the historical world within the type of divination, the artwork of telling the long run by seeing patterns and clues in every thing from animal entrails to celestial patterns. As Isaac Asimov wrote in Future Days, such was the eagerness of individuals to consider these augers that they’d nice energy and will often rely on being properly supported by a grateful, or fearful, public. I am not so positive most of this is not relevant to immediately. Sherden did a lot analysis into the numbers of individuals straight concerned in forecasting—and this information was from 1998. They’re staggering and rising. And let’s not neglect that one of many largest-selling newspapers within the nation is the Nationwide Enquirer. Under are a number of the findings on forecasting from Sherden’s e-book.

- No higher than guessing.

- No long-term accuracy.

- Can not predict turning factors.

- No main forecasters.

- No forecaster was higher with particular statistics.

- Nobody ideology was higher.

- Consensus forecasts don’t enhance accuracy.

- Psychological bias distorts forecasters.

- Elevated sophistication doesn’t enhance accuracy.

- No enchancment through the years.

A climate forecaster may have an distinctive report if he says merely that tomorrow might be identical to immediately. If I had been a climate forecaster, I might are inclined to err on the aspect of unhealthy climate as an alternative of fine climate. Then, in case you are flawed, most is not going to discover. It’s once you forecast good climate, and it’s not, that they’ll discover. Most market prognosticators are inclined to have a bullish or a bearish bias of their forecasts. Bullish forecasts are usually well-accepted, particularly by the Wall Avenue neighborhood, and bearish forecasting is a big enterprise as a result of it infringes on traders’ fears.

“Given the difficulties forecasting the long run, it is vitally helpful to easily know the current.” — Unknown

Barry Ritholtz (The Huge Image weblog) just lately identified how ridiculous the forecasting enterprise has grow to be. Specifically, the end-of-the-year forecasts for the subsequent yr or the most effective shares to personal. Right here is an instance from the August 14, 2000, difficulty of Fortune journal by David Rynecki on “10 Shares to Final the Decade.”

August 14, 2000

- Nokia (NOK: $54)

- Nortel Networks (NT: $77)

- Enron (ENE: $73)

- Oracle (ORCL: $74)

- Broadcom (BRCM: $237)

- Viacom (VIA: $69)

- Univision (UVN: $113)

- Charles Schwab (SCH: $36)

- Morgan Stanley Dean Witter (MWD: $89)

- Genentech (DNA: $150)

Closing Costs December 19, 2012

- Nokia (NOK: $4.22)

- Nortel Networks ($0)

- Enron ($0)

- Oracle (ORCL: $34.22)

- Broadcom (BRCM: $33.28)

- Viacom (VIA: $54.17)

- Univision ($?)

- Charles Schwab (SCH: $14.61)

- Morgan Stanley Dean Witter (MWD: $14.20)

- Genentech (Takeover at $95 share)

Ritholtz goes on to say, “The portfolio managed to lose 74.31 p.c, with three bankruptcies, one bailout, and never a single winner within the bunch. Even the Roche Holdings takeover of Genentech was for 37 p.c beneath the instructed buy worth. Had you merely purchased the S&P 500 Index ETF (SPY), you’ll have seen a achieve of over 23 p.c.”

On March 11, 2008, CNBC’s Mad Cash host, Jim Cramer, emphatically stated it was silly to maneuver cash out of Bear Stearns. He claimed that Bear Stearns was simply effective. He was completely flawed. Every week later, JPMorgan agrees on March 16 to purchase Bear for $236 million, or $2 a share, representing simply over 1 p.c of the agency’s worth at its report excessive shut simply 14 months earlier. The deal basically marked the tip of Bear’s 85-year run as an impartial securities agency. On Monday, March 17, Bear shares closed at $4.81 on optimism one other purchaser might emerge. The typical goal worth: $2. Do not confuse recommendation from somebody within the leisure enterprise with recommendation from somebody who manages cash. Actually, do not take note of anybody’s predictions. Nobody is aware of the long run!

The Reign of Error

In 1987, a e-book was written entitled The Nice Despair of 1990, by Dr. Ravi Batra, an SMU professor of economics. Sadly, I purchased and skim that e-book. Batra was claimed as one of many nice theorists on the planet and ranked third in a gaggle of 46 superstars chosen from all economists in American and Canadian universities by the realized journal Financial Inquiry (October 1978). The foreword was written by world-renowned economist Lester Thurow, who stated The Nice Despair of 1990 is essential studying for everybody who hopes to outlive and prosper within the coming financial upheaval. The title for one chapter was “The Nice Despair of 1990–96.” Not solely did he pronounce the start of it, he additionally proclaimed to know the tip.

The Nineteen Nineties noticed the most important bull market in historical past, with the Dow Industrials rising from 2,700 to over 11,000 in the course of the decade of the Nineteen Nineties. By the tip of the last decade, we had been flooded with books concerning the unending bull market, reminiscent of Dow 40,000 by Elias, Dow 36,000 by Glassman and Hassett, and Dow 100,000 by Kadlec. From 2000 till early 2003, we witnessed a bear market that eliminated many of the positive factors of the earlier 10 years, with the Dow Industrials again all the way down to about 7,350.

“We’re making forecasts with unhealthy numbers, however unhealthy numbers are all we’ve got.” — Michael Penjer

These forecasts had been useless flawed; nevertheless, I ‘m positive the authors offered numerous books. The unhealthy information within the inventory market didn’t finish after the bear market from 2000 to 2003; by March 2009, the Dow Industrials was beneath the extent of the earlier bear by one other 8 p.c. Companies whose responsibility is to make forecasts had been nearly universally flawed in the course of the 2006 to 2007 interval, with forecasts of the economic system, the markets, and the world outlook all optimistic; even those that weren’t fairly as rosy had been solely modestly so. The enterprise magazines had been the identical. What number of forecasts do you end up studying and listening to? Did you ever analysis to see if any of them ever turned out to be right? And even shut?

Finance shouldn’t be the identical as physics, in that no mathematical mannequin can totally seize the massive variety of at all times altering financial elements that trigger huge market strikes—the monetary meltdown of 2008 is an instance. Emanuel Derman says, “In physics, you are enjoying towards God; in finance, you are enjoying towards folks.” The parallelism between physics and finance has gained assist from writer Nassim Taleb, who says, “It would not meet the quite simple rule of demarcation between science and hogwash.” Whether or not invoking the physicist Richard Feyman or the late Fischer Black, using mathematical fashions to worth securities is an train in estimation. Derman additional states, “You must take into consideration how you can account for the mismatch between fashions and the true world.”

“Science is a good many issues, however in the long run all of them return to this: Science is the acceptance of what works and the rejection of what would not. That wants extra braveness that we would suppose.” — Jacob Bronoski

Lengthy Time period Capital Administration (LTCM) was began by John Meriwether, who had an amazing following together with Myron Scholes and Robert Merton, two well-known economists. Collectively, they grew LTCM into property of greater than $130 billion, utilizing a mannequin they claimed would obtain distinctive returns with out the same old threat. That alone ought to have been all of the warning anybody wanted. In 1997, their mannequin didn’t do properly, and by mid-1998 they’d misplaced all of it; they’d borrowed greater than a trillion {dollars} to make investments. The story led to September 1998, when the New York Federal Reserve Financial institution led a gaggle of organizations to step in and bail them out; shortly thereafter, there was no extra LTCM. Teachers with refined fashions are a harmful lot. And here is the most effective half—simply earlier than the demise, Scholes and Merton received the Nobel Prize for economics for his or her efforts in monetary threat management.

LTCM was not alone; tales of a whole bunch of funds have gone out of enterprise after brief intervals of remarkable success. Rogue trades had been rampant. Keep in mind Nick Lesson of Barings Financial institution? How about Jerome Kerviel of Societe Generale, or a number of enormous banks in the course of the interval? The checklist is lengthy and rising. Enron, WorldCom, and International Crossing had been only a few massive firms that went bankrupt, taking their staff’ pensions and investments with them. I do not recall anybody ever anticipating any of those failures; forecasters by no means do.

After the inflationary decade of the Nineteen Seventies, the value of gold was hovering. Within the early Eighties, forecasts of gold reaching unbelievable heights had been all over the place. They had been supported with the info that gold’s mounted worth was launched in 1971 and it was free to commerce, and commerce it did. The Hunt Brothers had purchased a big portion of the silver market. No forecaster noticed something however greater costs. I recall shopping for three 100-ounce bars and wishing I had extra money to purchase extra. You will note in Chapter 11 on drawdowns that gold plummeted in 1981, and it took greater than 25 years to get again to its peak. And by 2013, the forecasts of gold going to the moon had been all over the place.

At what level will we begin to consider that forecasting is a hoax? This e-book is concerning the inventory market, the place the forecasting enterprise is big. I can inform you this: inventory market forecasters are not any totally different than financial forecasters. Those who get fortunate with a forecast are those who’ve but to be flawed. I feel the worst of them are those I name outliers (to not be confused with outlaws); these are those who, via some stroke of luck, make a forecast about one thing huge and it seems to truly occur. Nonetheless, it’s not often within the precise method of the forecast, however that’s quickly forgotten as she or he is paraded via the monetary media because the guru of the yr. They begin newsletters, maintain conferences, and embark on intervals of increasingly more forecasts as a result of they’re now specialists. But, most not often make one other right forecast. John Kenneth Galbraith stated: “Relating to the inventory market, there are two sorts of traders: those that have no idea the place it’s going, and those that have no idea that they have no idea the place it’s going.”

An Funding Skilled’s Dilemma

When talking to funding advisors, I usually remind them that they need to take care of two realities:

- Your shoppers count on you to have solutions.

- The market is unpredictable.

After you have your shoppers believing #2, then the questions for #1 might be simpler to reply. Most advisors, and particularly their shoppers, get caught up within the second and are simply swayed into believing that some skilled really is aware of the long run. Or that they deal with the current previous and extrapolate that advert infinitum.

“Thoughts you, it is best to take financial forecasts—even my very own—with an enormous grain of salt.” John Kenneth Galbraith might have been extra proper than econometricians wish to suppose when he stated that “The one perform of financial forecasting is to make astrology look respectable.”

Nobel Prize-winning economist Kenneth Arrow has his personal perspective on forecasting. Throughout World Conflict II, he served as a climate officer within the U.S. Military Air Corps, working with people who had been charged with the notably tough job of manufacturing month-ahead climate forecasts. As Arrow and his staff reviewed these predictions, they confirmed statistically what you and I would simply as simply have guessed: The Corps’ climate forecasts had been no extra correct than random rolls of a die. Understandably, the forecasters requested to be relieved of this seemingly futile responsibility. Arrow’s recollection of his superiors’ response was priceless: “The commanding basic is properly conscious that the forecasts are not any good. Nonetheless, he wants them for planning functions.” (Peter Bernstein, Towards the Gods)

“You do not want a weatherman to know which manner the wind blows.” — Bob Dylan

The e-book Dance with Likelihood by Spyros Makridakis (an writer who wrote an exquisite business-forecasting e-book a few a long time in the past) provides a brief story about Karl Popper. Popper was a thinker of science born in Austria. Within the Nineteen Thirties, he leveled a cost towards Sigmund Freud, whose psychoanalytical theories had gained widespread acceptance. Popper identified that actual scientists begin with conjectures, which they then attempt to refute—in addition to in search of proof to assist them. Solely by failing to disprove their hypotheses, can they show they had been right. In the meantime pseudoscientists, as Popper known as them, solely search for occasions that show their theories right. Theories like this are little greater than untested assertions. That is to not say the assertions cannot finally change into proper, however we are able to solely attain this conclusion as soon as somebody has examined them.

“Forecasting the long run is rather more tough than forecasting the previous.” — Unknown

Forecasting the way forward for financial, financial, monetary, or political potentialities has a severe flaw in that no matter in case your forecast is near being right, and even whether it is spot on, the belief about how the market will react is the place the large drawback lies. There’s a flawed perception that optimistic occasions from political, financial, and financial information will replicate positively on the markets. Conversely, destructive information occasions will replicate negatively on the markets. This merely shouldn’t be true. You may see that there’s hardly any usable correlation to those occasions and the markets; earnings bulletins are an ideal instance. What number of instances have they been optimistic and the inventory market didn’t react accordingly? The hole between an excellent financial or financial forecast and the fact of what the market does is big.

“There’s at all times a purpose for a inventory appearing the best way it does. But additionally do not forget that chances are high you’ll not grow to be acquainted with that purpose till someday sooner or later, when it’s too late to behave on it profitably.” — Jesse Livermore

The next (barely modified) comes from Gary Anderson, who wrote the must-read e-book entitled The Janus Issue. The hyperlink between fundamentals and worth is elastic, and barely nonetheless. At instances, good earnings studies trigger the value of a inventory to rise, whereas at different instances merchants use optimistic earnings information to promote the identical inventory. Will a worldwide disaster enhance the worth of the greenback or ship it decrease? The linkage between change on the planet and alter available in the market is commonly ambiguous and typically simply plain mysterious. Usually, human beings are intelligent sufficient to create believable tales to account for the market’s response to occasions, however too usually solely with assistance from hindsight. There’s a fixed shift within the elementary reasoning used to assist selections to purchase and promote. The monetary media is consistently justifying every transfer available in the market with no matter current occasion they’ll discover that helps that transfer. Elementary conventions supporting purchase/promote selections can range from interval to interval and haven’t any place in rational investing.

We will draw a helpful distinction between causes and causes. Earnings don’t trigger costs to maneuver, nor do analysis studies, information bulletins, speaking heads, dividends, inventory splits, the economic system, peace, or warfare. These elements could also be causes motivating merchants to purchase and promote, however the direct reason behind a inventory’s worth motion is the shopping for and promoting exercise of merchants and traders. We deal with causes, not causes—on what merchants do, not why. That is completed by measuring worth and worth derivatives (breadth, relative energy) of worth motion.

Gurus/Consultants

What would we do with out all of the specialists, gurus, pontificators, purveyors of gloom and doom, and, in fact, the perma-bulls and perma-bears?

To begin with, a large business could be gone, an business that generates billions of {dollars} within the USA alone. I am not going to spend an excessive amount of time on this, as a result of the web site of CXO Advisory Group LLC, CXOadvisory.com , does all of the heavy lifting. They’ve a complete part dedicated to GURUS. Listed here are the 2 questions they ask in the beginning of that part: “Can specialists, whether or not self-proclaimed or endorsed by others (publications), present dependable inventory market timing steering? Do some specialists clearly present higher instinct about total market route than others?” They handle these questions with a logical and clear course of. After following greater than 60 specialists and hundreds of observations, close to the tip of the Guru part, they conclude: “The general accuracy of the group, primarily based on each uncooked forecast rely and on the common of forecaster accuracies (weighting every particular person equally) is 47 p.c. In abstract, inventory market specialists as a gaggle don’t reliably outguess the market. Some specialists, although, could also be higher than others.” Hmmm! It looks as if a coin toss, on common, would do higher.

Moreover, CXOadvisory.com evaluations quite a few educational papers, after which does its personal backup evaluation to find out if the paper’s writer and so they agree. A superb piece, when reviewing Charles Manski’s July 2010 paper entitled “Coverage Evaluation with Unbelievable Certitude,” categorizes unimaginable analytical practices and underlying certitude. These 4 are:

- Typical certitudes (standard knowledge)—Predictions (indicators) that specialists usually settle for as correct, however should not essentially correct.

- Dueling certitudes—Two contradictory predictions that competing specialists current as precise, with no expression of uncertainty (resulting in conflicting robust funding technique suggestions).

- Conflating science and advocacy—Growing arguments (assumptions) that assist an funding technique somewhat than an funding technique that helps evidence-based arguments, whereas portraying the deliberative course of as scientific.

- Wishful extrapolation—Drawing a conclusion about some future state of affairs primarily based on historic tendencies and untenable assumptions (ignoring variations between the historic and future conditions, and emphasizing in-sample over out-of-sample testing).

If in case you have ever watched tv, learn a e-newsletter, or attended a seminar, I am positive the above sounds acquainted. Individuals who seem as specialists usually are no higher than the lots; nevertheless, when they’re flawed, they’re not often held accountable, and by no means admit it (usually). They may reply that their timing was simply off or some catastrophic occasion caught them off guard, or worse—flawed for the appropriate causes.

There’s a e-book by Philip Tetlock, Knowledgeable Political Judgement: How Good Is It? How Can We Know?, that offers with the enterprise of prediction. Tetlock claims that the better-known and extra often quoted they’re, the much less dependable their guesses concerning the future are more likely to be. The accuracy of their predictions really has an inverse relationship to his or her self-confidence, renown, and depth of information. Take heed to specialists at your individual threat.

Larry Williams was an lively and famend dealer earlier than I even started to point out curiosity within the markets. There’s one important level that Larry has made persistently that must be repeated right here. If you’re going to be mentored by somebody, if you’re going to learn somebody’s e-book on buying and selling/investing, if you’re going to join a course of instruction from somebody, please make certain they’re certified to show the topic. This doesn’t at all times translate into how they commerce or make investments. Like Larry says in his Buying and selling Lesson 16, Kareem Abdul-Jabbar tried teaching and was a catastrophe at it; Mark Spitz’s swimming coach couldn’t swim. Nonetheless, the underside line is that the most effective lecturers are in all probability those who really commerce and make investments, as they’ve firsthand expertise to the nuances of the talent. This argument shouldn’t be not like the one between the ivory tower lecturers and people concerned in the true world making use of their craft each day. Whereas they could have appreciable expertise to supply, your chances are high in all probability higher with an actual practitioner.

Masking an Mental Void

My formal training was in aerospace engineering. My training in “The World of Finance” got here and continues to come back from folks within the funding business I’ve grown to respect. I hate to checklist some as concern of leaving somebody out, however Ed Easterling, John Hussman, and James Montier are definitely on the high of the checklist. Are these professionals at all times right? After all not, however they often admit it and so they write in such a fashion that they know the uncertainty is at all times there and but current legitimate arguments on a variety of subjects and ideas. The remainder of the educational comes for studying actually a whole bunch and a whole bunch of white papers in finance and economics. This course of brought about my concern on the insane use of superior arithmetic, often within the type of partial differential equations, to supposedly help in making the purpose that the paper was addressing. I can not inform you what number of instances I assumed that many of the math was pointless and as a rule the paper would have stood alone with out the maths. In lots of cases I feel there’s an try by most to overly complicate their work with arithmetic with the idea that it brings credibility to their work. Another excuse, and one I definitely can not show, is that in addition they know that most individuals who learn their paper, apart from their friends, is not going to grasp the maths and simply assume it’s legitimate and vital.

The senior particular author, Carl Bialik, of The Wall Avenue Journal, who writes a piece known as “The Numbers Man”, is one among my favourite reads. As I used to be wrapping up analysis for this e-book and considering that I had included sufficient opinions about issues with out substantial proof, I used to be delighted to search out assist from Carl for this part on “Masking an Mental Void.” On January 4, 2013, he wrote two articles entitled, “Do not Let Math Pull the Wool Over Your Eyes,” and “Awed by Equations.” These articles referenced two papers that gave assist to my perception within the overuse of arithmetic, and the way readers of white papers usually had been impressed with what they really didn’t perceive. Analysis was performed utilizing solely the abstracts of two papers, one with out math, and one with math; the catch being that the one with math was bogus, completely unrelated to the paper. But the very best share of contributors who gave the very best score to the summary with added math, primarily based on the contributors’ instructional diploma, was as follows:

Math, Science, Expertise 46 p.c

Humanities, Social Science 62 p.c

Medication 64 p.c

Different 73 p.c

I feel this reveals that those that had a excessive likelihood of not understanding the maths gave the paper with the bogus math a better score, whereas those that presumably did perceive the maths didn’t.

That is simply my lame try at humor. The monetary lecturers have nearly universally used partial differential equations of their white papers; I feel, as a rule simply to cover an mental void. Many instances, the tough math shouldn’t be vital, however by together with it, they know most won’t ever be capable to query their work. Unhappy, certainly! By the way, the equation could be simplified to 1 + 1 = 2.

Earnings Season

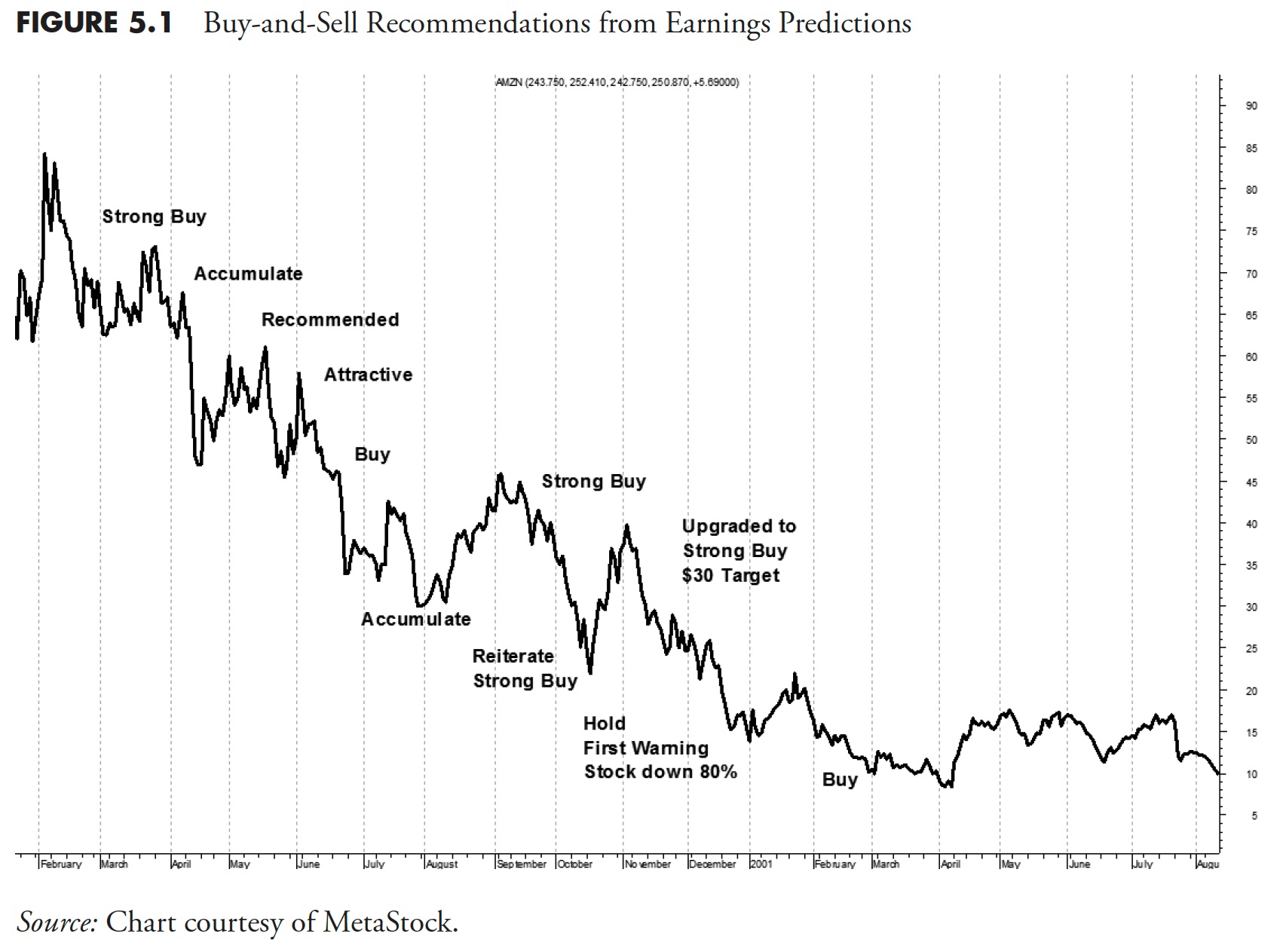

For many years, I’ve watched the parade of earnings bulletins and the way the media hangs on each as if it really had some worth apart from filling useless air. Determine 5.1 reveals the inventory worth of Amazon again within the 2000-2001 bear market. The annotations are from precise earnings forecasts from analysts. For those who yell “purchase” all the best way down, the chances are good that you’ll finally be right. Hopefully, you’ll nonetheless have some cash.

“In our view, safety analysts as an entire can not estimate the long run earnings sample of a number of progress shares with adequate accuracy to supply a agency foundation for valuation within the majority of circumstances.” — Benjamin Graham

Evidently the media is so centered on earnings studies that they neglect to report the precise earnings. As an alternative, their focus is on the place the earnings got here in relative to the analysts’ estimate. After beating up on specialists, it’s laborious to think about that somebody would really make an funding resolution primarily based on an analyst’s (skilled) guess as to what earnings ought to be. These analysts are consistently wined and dined by the businesses they analyze, so, typically, I feel they’re biased, and nearly at all times to the upside. Actually, I feel most are actually simply development followers, in that they’re at all times forecasting higher earnings as markets rise and, as soon as a market rolls over and begins to say no, they finally start to forecast decrease earnings.

Determine 5.1

Determine 5.1

When requested what traders’ biggest issues are, the late Peter Bernstein stated, “Extrapolation! They consider the current previous is how the long run might be.”

Are Monetary Advisors Value 1% of AUM (Property Beneath Administration)?

“Individuals who want recommendation are least more likely to take it.” — Unknown

Many asset managers maintain totally too many shares and have grow to be closet benchmark trackers. In the event that they beat their benchmark, they name it alpha, and when they don’t beat their benchmark, they name it monitoring error. In case your funding supervisor rebalances your portfolio periodically primarily based on just a few questions that he required you to reply when organising the account, listed here are some issues to consider. Often, the chance tolerance and goal questionnaire is rather more concerned, however listed here are two questions usually requested:

- What share of present revenue will you want once you retire?

- On a scale from 1 to 7, what’s your threat tolerance?

Do you actually consider an individual is aware of the solutions to these questions? No manner! They may attempt to reply primarily based on what the advisor has informed or instructed to them. The regulation requires the sort of motion for advisors, so decide an advisor you suppose will really meet your wants and, in case you are not sure, can level you in the appropriate route.

Economists Are Good at Predicting the Market

“The economic system relies upon about as a lot on economists because the climate does on climate forecasters.” — Jean Paul Kauffman

Simply to place this into perspective, the inventory market is a element of the index of main indicators. If the inventory market is an effective main indicator of the economic system, why ask an economist what the market goes to do? But they’re paraded day by day throughout the monetary media, making forecasts concerning the markets, political coverage, fiscal coverage, financial occasions, and, sure, often concerning the economic system. When they’re right, they will not allow you to neglect it; when they’re flawed, nobody remembers. Many economists are good when coping with the economic system, however not often are they good once they stray into different areas.

Information Is Noise

Here’s a humorous try and painting a number of the day by day noise also known as information. On Wall Avenue immediately, information of decrease rates of interest despatched the inventory market up, however then the expectation that these charges could be inflationary despatched the market down, till the belief that decrease charges may stimulate the sluggish economic system pushed the market up, earlier than it in the end went down on fears that an overheated economic system would result in as soon as once more an imposition of upper rates of interest.

Rolf Dobelli, writing for The Guardian, on April 12, 2013, in an article entitled “Information is unhealthy for you—and giving up studying it would make you happier,” listed these issues with information:

- Information misleads.

- Information is irrelevant.

- Information has no explanatory energy.

- Information is poisonous to your physique.

- Information will increase cognitive errors.

- Information inhibits considering.

- Information works like a drug.

- Information wastes time.

- Information makes us passive.

- Information kills creativity.

He claims he has gone with out information for 4 years and says it is not simple, nevertheless it’s value it. Since he wrote for a information group, I might think about he’s additionally searching for work.

“For those who can distinguish between good recommendation and unhealthy recommendation, then you do not want recommendation.” — VanRoy’s Second Legislation

When requested at seminars what’s the single most vital idea to grasp when investing, I reply merely that it’s to know thyself. The human thoughts is a horrible investor, and using heuristics doesn’t assist. The subsequent chapter offers with human conduct because it pertains to the market.

Thanks for studying this far. I intend to publish one article on this sequence each week. Cannot wait? The e-book is on the market right here.