{kind=link}

States’ company earnings taxA company earnings tax (CIT) is levied by federal and state governments on enterprise earnings. Many corporations should not topic to the CIT as a result of they’re taxed as pass-through companies, with earnings reportable beneath the person earnings tax. bases expanded dramatically with the enactment of the TaxA tax is a compulsory cost or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of common authorities companies, items, and actions. Cuts and Jobs Act (TCJA) in 2017, and that continues to be the case after the implementation of the brand new and restored enterprise expensing provisions beneath the One Large Stunning Invoice Act (OBBBA). As lawmakers in some states take into account decoupling from the pro-growth enterprise expensing provisions of the reconciliation act because of issues about company earnings tax baseThe tax base is the full quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slender tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges. erosion, it’s helpful to acknowledge simply how a lot bigger that company tax base has change into over the previous decade, and what quantity of the prices of conformity are frontloaded, with far decrease prices in subsequent years.

On the federal stage, the TCJA was a major tax reduce for people and companies alike, however the laws paired price reductions with substantial base broadening. States obtained the good thing about the broader tax base with out bringing within the (greater than) offsetting price reductions. Moreover, the TCJA stemmed the tide of company inversions and introduced extra funding again to the US. For the federal authorities, the insurance policies encouraging these actions got here at a income price, however few of those prices flowed by means of to the states, which benefited from the windfall.

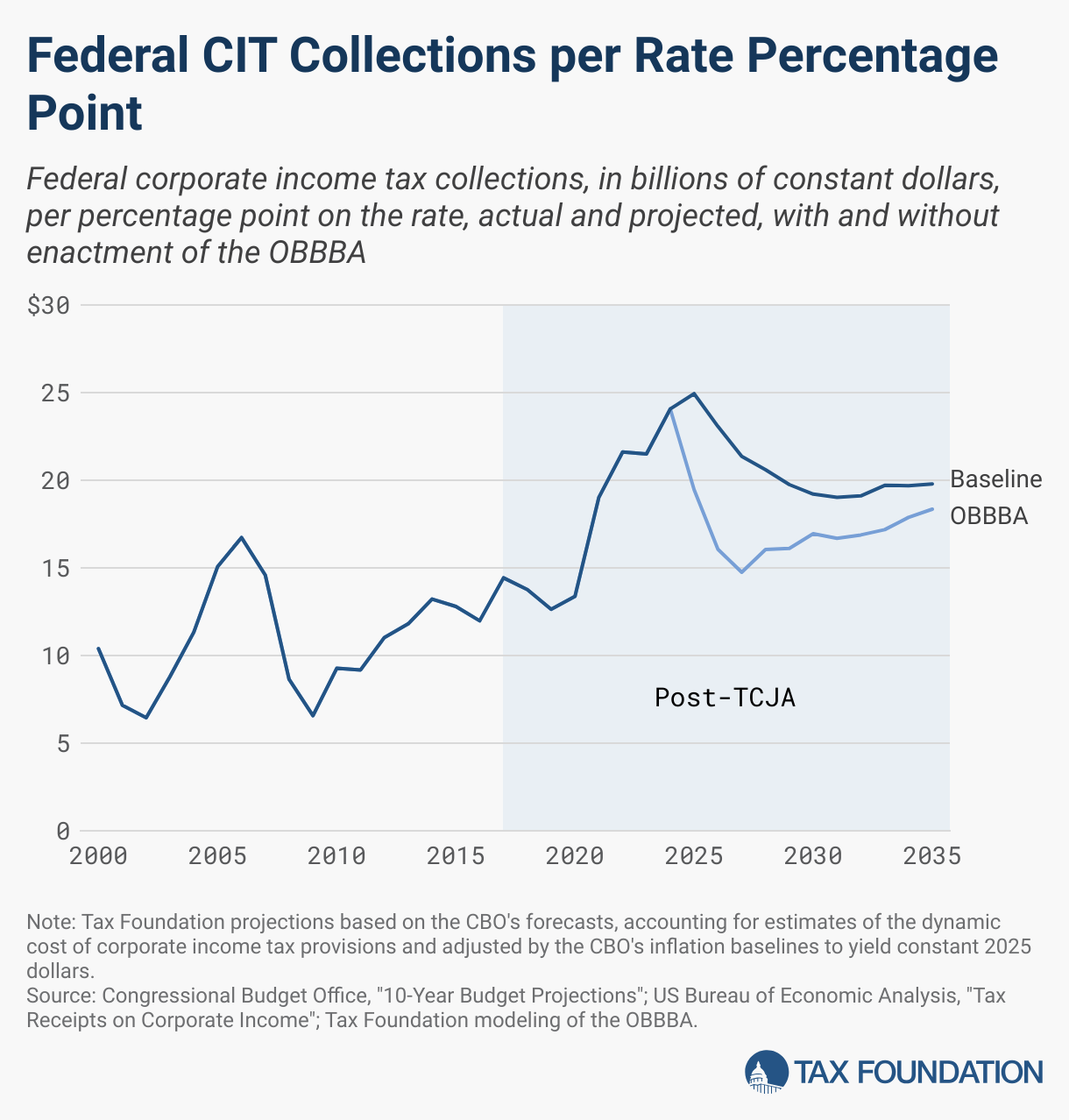

One method to visualize the expansion of the company earnings tax base is to chart the federal income generated per proportion level of the speed. Previous to the TCJA, the highest price was 35 p.c. (This was very practically equal to a flat price of 35 p.c because the overwhelming majority of company earnings was taxed on the prime price, and the schedule had a sequence of “bubble charges” to recapture the decrease charges.) Underneath the TCJA, company earnings is taxed at a flat price of 21 p.c.

From 2000 by means of 2016, the company earnings tax raised a median of $10.88 billion per level on the speed in actual (inflationInflation is when the final worth of products and companies will increase throughout the financial system, lowering the buying energy of a foreign money and the worth of sure property. The identical paycheck covers much less items, companies, and payments. It is typically known as a “hidden tax,” because it leaves taxpayers much less well-off because of increased prices and “bracket creep,” whereas growing the federal government’s spendin-adjusted) phrases. Because the TCJA went into impact in 2017, common annual collections per level on the speed soared to $19.30 billion. With or with out the OBBBA, collections have been projected to say no from an anticipated peak in 2026, however even with the brand new or restored expensing provisions from the OBBBA, the tax is projected to boost $16.94 billion per p.c on the speed—far increased than the pre-TCJA trajectory. Much more considerably, a lot of the discount is frontloaded, with the hole between the pre-OBBBA baseline and revenues beneath the OBBBA shrinking considerably by the tip of the finances window.

The OBBBA accommodates 4 enterprise expensing provisions:

- The restoration of first-year expensing for enterprise equipment and gear (M&E) beneath § 168(ok), to which 17 states conform

- The restoration of first-year expensing for analysis and experimentation (R&E) expenditures beneath § 174, which had been in place from 1954 to 2022 and to which all states traditionally conformed

- A brand new momentary expensing provision for factories beneath § 168(n)

- Increased limits for small enterprise expensing beneath § 179

The primary two provisions (the restoration of first-year expensing for M&E and R&E) are accountable for most of the price of enterprise expensing conformity and have drawn probably the most consideration. § 168(ok) expensing is sweet coverage, and states that provide the supply did so affirmatively and thus have good motive to keep up their conformity. More and more, nevertheless, some lawmakers are speaking about decoupling from § 174.

Requiring five-year amortization of analysis and improvement prices beneath § 174 was by no means actually supposed to enter impact. That gimmick (a “price financial savings” within the TCJA that was not meant to be realized) is honest recreation for criticism, however the analysis and experimentation expensing provision has all the time been so well-liked, so bipartisan, and such clearly applicable coverage, that many observers have been stunned the capitalization and amortization provision was permitted to take impact in 2022.

Companies have been allowed to deduct R&E expenditures within the 12 months wherein the expense is incurred since 1954, and each state with a company earnings tax has adopted go well with. When the federal authorities shifted to five-year amortization starting in 2022, 10 states continued to supply instant expensing of R&E, both by means of categorical coverage or by conforming to a pre-TCJA model of the Inner Income Code. All different states with company earnings taxes adopted the federal authorities’s lead in setting apart the R&E coverage that had prevailed for 68 years. By conforming to its restoration, states shall be accepting a “price” in comparison with the coverage of the previous three and a half years, however one which was absolutely baked into their tax code for the higher a part of seven many years.

This price is front-loaded, since first-year expensing signifies that deductions for any R&E bills should not obtainable in years 2-5. Functionally, states obtained a windfall from 2022 by means of earlier this 12 months, with deductions unfold out, however with comparatively decrease income in subsequent years since they needed to proceed providing these amortized deductions. Restoring conventional therapy has the other impact: a large preliminary price, however a reversal in subsequent years.

First-year expensing does have a price for states for a similar motive that it’s useful for companies: beneath amortization, companies’ deductions are eroded by inflation, and their current worth is lowered because of the time worth of cash. However in the long term, the state income prices are modest—they usually’re what each state with a company earnings tax accepted as solely unexceptional from 1954 (or at any time when they adopted the tax) to 2022. Absent first-year expensing for R&E, the company tax code is biased in opposition to funding in analysis and improvement. It’s ironic that the majority states considerably carve up their tax code with R&D credit, however some at the moment are contemplating introducing a penalty in opposition to those self same expenditures. Nonetheless worse, R&E is on the market to all company taxpayers with internet earnings, whereas R&D incentives are sometimes solely obtainable to massive incumbent corporations.

Decoupling from § 174 is opposite to most policymakers’ said objectives, and it’s on no account made crucial by the trajectory of company tax collections, which stay effectively above the wildest goals of state lawmakers pre-TCJA.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

Share this text