{kind=link}

October 24, 2025

One of many many upsides to residing within the twenty first century is that common life expectations are greater than ever earlier than. Individuals who make it to retirement age can anticipate to get pleasure from many extra years of well being and happiness than their mother and father and grandparents.

One of many many upsides to residing within the twenty first century is that common life expectations and lifespans are greater than ever earlier than, and so individuals who make it to retirement age can anticipate to get pleasure from many extra years of well being and happiness than their mother and father and grandparents.

This creates considerations at a state and nationwide stage, because the getting old inhabitants places stress on varied programs that have been designed and applied lengthy earlier than present lifespan tendencies got here to move. It additionally poses potential issues for people, because the query of monetary safety in retirement turns into extra acute when individuals can fairly anticipate to stay longer whereas counting on the pension provisions they’ve put in place.

So, is there a real disaster brewing, or can we anticipate rising life expectations to be manageable with the appropriate planning? The group at Abacus International Administration, Inc. got down to reply this query by letting the info do the speaking.

The Progress of Golden Years Dwelling

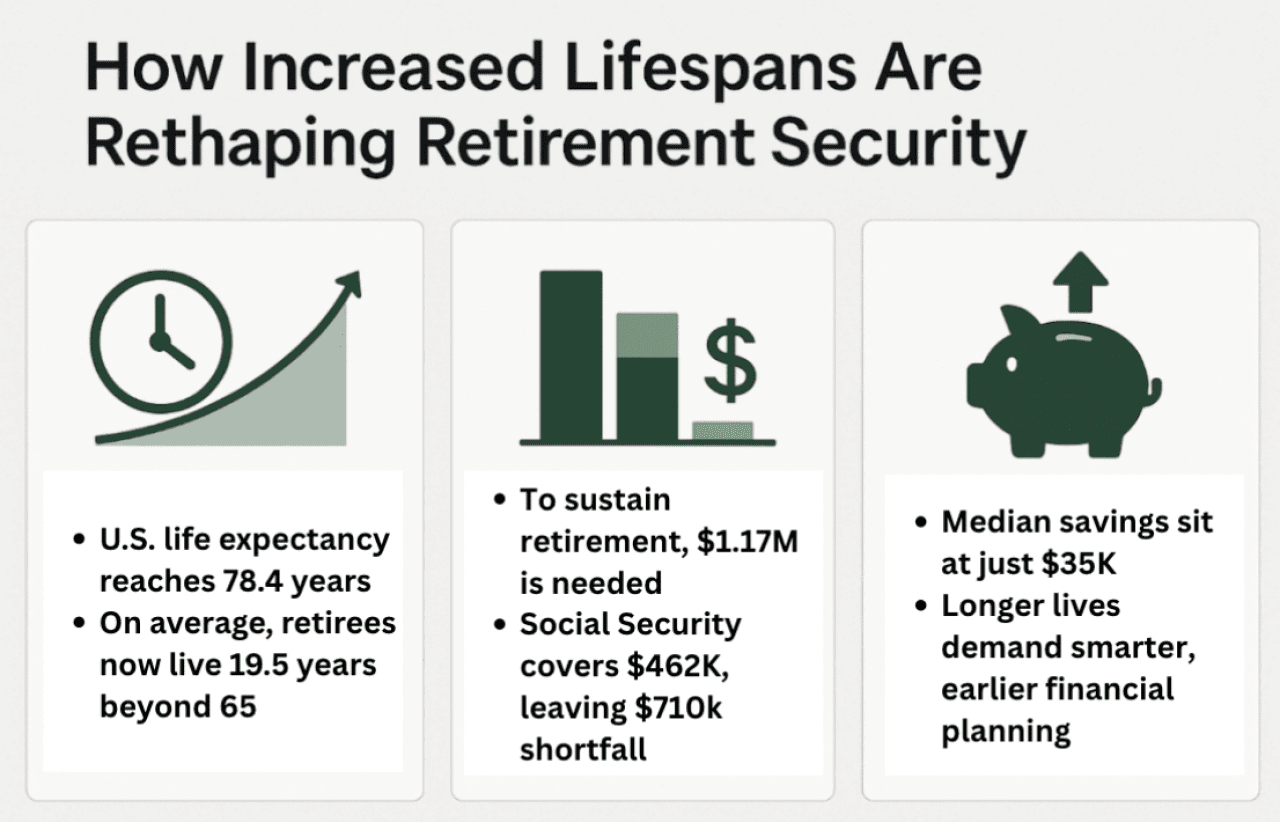

The newest statistics from the CDC, printed for 2023, point out a median life expectancy of 78.4 years. This represents a virtually one-year improve in comparison with 2022’s knowledge, indicating simply how quickly lifespans are rising year-on-year.

What’s extra pertinent to our dialogue is the life expectancy for somebody who reaches 65. That is 19.5 years on common, that means that an individual who chooses to finish their profession at this level can have practically twenty years forward of them.

There’s a gender hole right here, with girls who attain 65 residing for 20.7 years, whereas males can anticipate to stay for 18.2 years in the event that they survive so far.

The Retirement Financial savings Conundrum

Deciphering the info on retirement safety is relatively difficult, since there’s a major hole between these with important sums squirreled away and people with extra modest pots. This makes averages much less helpful with out additional scrutiny.

Vanguard’s newest report on saving habits exemplifies this. The median account stability reported for 2023 was $35,286. This represents the precise midpoint in each account throughout this explicit supplier’s buyer base.

Nevertheless, the typical holding for that 12 months was $134,128, with this determine pushed nicely past the median by a smaller quantity of people that had put aside considerably more money than is typical. The truth is, simply 15% of consumers had greater than $250,000 saved, whereas 53% had underneath $40,000.

Constancy’s figures supply just a little extra readability. Right here, knowledge on 401(ok) and IRA balances are divided generationally. Child boomers lead the pack with $249,300, with Gen X coming shut behind with $192,300. Millennials have $67,300 on common, whereas Gen Z brings $13,500 to the desk, which is comprehensible, on condition that many members of this group are solely simply getting into the world of labor or are nonetheless in full-time schooling.

It’s additionally price bearing on knowledge drawn from the Survey of Client Funds, which paints its personal image of the present state of retirement financial savings. The latest survey, performed in 2022, reveals that household retirement accounts common $87,000. That’s up from $75,350 in 2019.

The Rising Hole

So, persons are residing longer and getting older, and common retirement pots are rising, albeit modestly. What actually issues is the affordability of retirement. Inflation stays a problem, and people with mounted post-retirement incomes should take into account this when in search of to take care of their high quality of life.

Information from the Federal Reserve Financial institution of St. Louis exhibits that the typical annual expenditure for over-65s is $60,087. The mathematics is easy: You’ll want $5,000 a month to maintain up with the price of trendy residing, or $1,171,696 over 19.5 years.

The Social Safety retirement profit could account for a portion of this, though it’s a good distance in need of the $5,000 mark. As an example, recipients have been paid out $1,976 for January of 2025, that means that they’d want over $3,000 from their private retirement belongings to shut the hole.

The Retirement Shortfall

Whereas $1.17 million is a frightening determine, retirees don’t need to fund all of it from their private financial savings. Social Safety gives a vital revenue stream. With the typical month-to-month profit at $1,976 ($23,712 per 12 months), the everyday retiree can anticipate to obtain about $462,000 from Social Safety over their 19.5 years of retirement.

This leaves a spot of roughly $710,000 that should be lined by private financial savings, pensions, and investments.

When this required financial savings quantity is in comparison with actuality, the true scale of the issue emerges. In response to Vanguard’s 2023 “How America Saves” report, the median retirement account stability was simply $35,286. Even the typical stability, skewed by high-net-worth people, was solely $134,128. This reveals a staggering shortfall of practically $700,000 for the everyday American retiree.

The Backside Line

There are variations in lifespan based mostly on age, gender, socioeconomic standing, race, and plenty of different components. These similar variables affect common incomes, financial savings, and different belongings. So drawing conclusions about your individual circumstances from top-level knowledge shouldn’t be doable.

What is clear is that should you’re nonetheless working now, you’ll stay longer than you’d should you’d been born into any earlier era. As such, getting ready for all times after work requires extra thought and a firmer dedication sooner slightly than later.

The retirement hole is actual, and the price of residing is barely going to extend as time passes. Saving early and investing properly will stand you in good stead for a future wherein the one certainty is that you simply’ll want a agency monetary footing to get pleasure from retirement, slightly than simply subsisting on state payouts.

This story was produced by Abacus International Administration and reviewed and distributed by Stacker.

RELATED CONTENT: Ndamukong Suh Retires From NFL And Tackles Wealth Constructing With New Finance Podcast