Proposal: Particulars & Evaluation")

{kind=link}

After France’s Constitutional Council upheld the legality of the nation’s digital companies taxA tax is a compulsory cost or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of common authorities companies, items, and actions. (DST), the Nationwide Meeting proposed an modification to lift the DST fee from 3 % to as excessive as 15 % as a part of ongoing price range negotiations. This week, a separate modification, which might legally substitute the earlier one, proposed to double the present DST fee to 6 %. This is able to be a significant coverage shift with probably dangerous penalties for all stakeholders.

DSTs Tax Revenues Reasonably Than Earnings

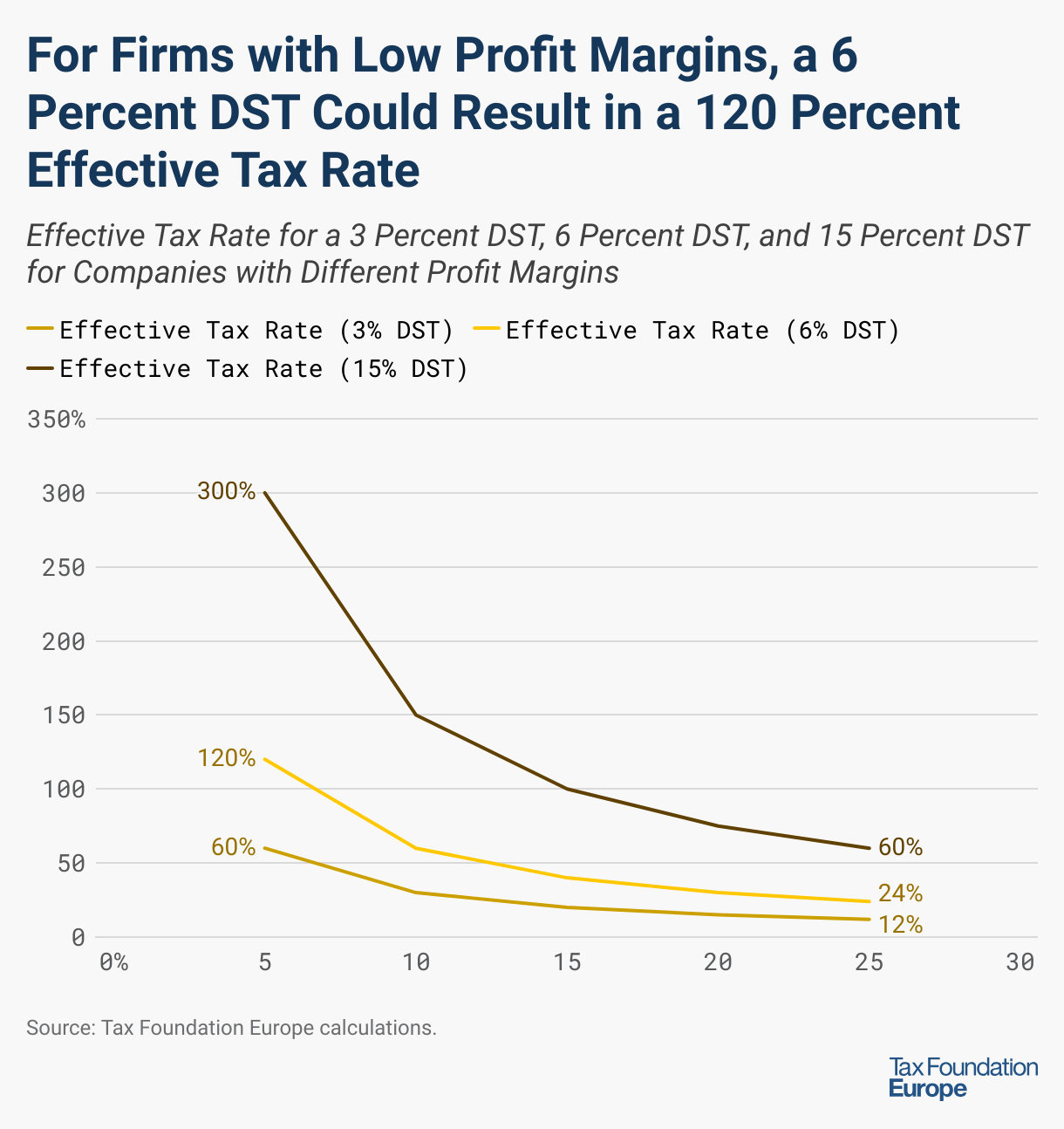

In contrast to company earnings taxes, DSTs are levied on revenues quite than income. Traditionally, European nations have turned away from a majority of these taxes as a result of even low tax charges can translate into excessive efficient tax burdens. For instance, if an organization has €100 in income and €90 in prices, it is going to earn €10 in revenue. Beneath the present regulation, if a 3 % DST is utilized to that income, the corporate would owe €3 in tax (3 % of €100 in income). For this firm, a 3 % tax on income equals a 30 % tax on income (a €3 tax on a €10 revenue).

Nonetheless, below this new proposal, if a 6 % DST is utilized to that very same firm, the corporate would owe €6 in tax (6 % of €100 in income)—a 60 % tax on income.

The next determine reveals how totally different revenue margins for that very same firm incomes €100 in income relate to totally different efficient tax charges, below the present (3 %) and proposed (15 %) DST charges. With a 15 % DST, if that firm solely earned a 5 % revenue margin, the efficient tax fee can be 300 %. With a 25 % revenue margin, the efficient tax fee can be 60 %.

Even earlier than this proposal, the DST led to a disproportionate tax burden being positioned on firms with decrease revenue margins—the much less worthwhile an organization was, the upper its efficient tax fee turned. That is regressive. Nonetheless, a 15 % DST would disproportionately affect all firms, no matter profitability, and would turn into confiscatory for firms with revenue margins under 15 %.

A New Threshold

The modification additionally raises the worldwide income threshold for firms topic to the tax from €750 million to €2 billion. Nonetheless, this enhance will make the DST much more discriminatory by way of firm measurement. The income threshold ends in the tax solely being utilized to massive multinationals. Whereas this may keep away from burdening smaller firms, it additionally gives a relative benefit for companies under the edge and creates an incentive for companies working close to the edge to change their habits.

The French DST, which capabilities like a tariffTariffs are taxes imposed by one nation on items imported from one other nation. Tariffs are commerce boundaries that elevate costs, cut back accessible portions of products and companies for US companies and shoppers, and create an financial burden on overseas exporters. on sure companies, is designed to be discriminatory; it targets industries largely dominated by US firms, and the discrimination can be even higher if the income threshold is elevated. The US authorities has voiced opposition to DSTs during the last decade, with President Trump utilizing Part 301 investigations in his first time period, and, extra just lately, the US Congress threatening the Part 899 retaliatory tax. Ought to the proposed measure turn into regulation, the US is anticipated to reply with retaliatory commerce measures.

Financial Incidence

The modification abstract claims that the DST will “help digital sovereignty and public funds with out burdening households or home companies.” Nonetheless, this overlooks the financial actuality of tax incidenceTax incidence is a measure of who bears the authorized or financial burden of a tax. Authorized incidence identifies who’s chargeable for paying a tax whereas financial incidence identifies who bears the price of tax—within the type of greater costs for shoppers, decrease wages for staff, or decrease returns for shareholders.. A current analysis paper by economists Dominika Langenmayr and Rohit Reddy Muddasani reveals that the try to focus on large digital platforms misses the mark as the associated fee principally falls on shoppers.

A Increased DST Will Not Remedy France’s Deficit Downside

A part of the justification is to extend the income collected by the DST. Nonetheless, DST income in Austria, France, Italy, Spain, Turkey, and the UK ranged from €103 million (Austria) to €1.03 billion (the UK) in the newest 12 months income was reported. These numerous DSTs throughout Europe don’t work properly collectively. They work on totally different tax bases, and double taxationDouble taxation is when taxes are paid twice on the identical greenback of earnings, no matter whether or not that’s company or particular person earnings. on the identical companies is frequent.

Turkey’s DST, with a tax fee of 7.5 %, brings in probably the most at 0.14 % of complete revenues, whereas France’s present DST brings in lower than 0.06 % of complete revenues.

Even when France have been capable of quintuple its DST’s tax assortment (an unlikely end result), the quantity raised would nonetheless be lower than one % of the nation’s common income.

Current Income Raised from Chosen Digital Companies Taxes

| Nation | Most Current Yr for Official DST Income Reported | DST Income (Native Foreign money) in Hundreds of thousands | DST Income (in EUR) in Hundreds of thousands |

|---|---|---|---|

| Austria | 2023 | € 103 | |

| France | 2024 | € 756 | |

| Italy | 2024 | € 455 | |

| Spain | 2024 | € 375 | |

| Turkey | 2024 | ₺ 15,561 | € 322 |

| United Kingdom | 2025 | £900 | € 1,032 |

Be aware: These nations have been chosen as a result of they report digital companies tax income individually as a line merchandise.

Supply: Tax Basis evaluation of nationwide price range paperwork and bulletins.

If France is apprehensive about elevating extra money from digital companies, then it ought to proceed reforming its value-added tax (VAT) to successfully tax these companies on the level of consumption. Moreover, broadening the VAT tax baseThe tax base is the overall quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slim tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges. by eliminating lowered charges and exemptions would enhance France’s VAT income by 44.5 % whereas inflicting fewer distortions within the economic system. Lastly, the VAT is trade-neutral and doesn’t discriminate between companies.

Since a brand new DST would neither resolve France’s income shortfall nor keep away from shifting the burden to shoppers—and will set off renewed commerce tensions—it’s time for policymakers to rethink their strategy. Reasonably than increasing the DST, they need to eradicate it altogether. The core goal of tax coverage is to lift income effectively, and there are far more practical instruments than a DST to attain that objective.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

Share this text