{kind=link}

November 16, 2025

The thought behind an extended mortgage is to avoid wasting debtors money by lowering their month-to-month cost. However Does it work?

President Donald Trump steered the thought of 50-year mortgages to make dwelling shopping for extra inexpensive for Individuals. It’s not the primary time this concept has been tossed round, and it’s even been tried earlier than.

The thought behind an extended mortgage is to avoid wasting debtors some money by lowering their month-to-month cost. And it could do this, however the way in which mortgages work, it doesn’t truly prevent cash. Finder.com explains how this sort of mortgage would perform and what it could imply for patrons.

How a 50-year mortgage would work

Most mortgages use an amortization mannequin, also referred to as being front-loaded.

Entrance-loaded means that almost all of your month-to-month mortgage funds go to paying down curiosity within the first few years of the mortgage. Over time, increasingly of your month-to-month funds will probably be allotted towards your precise mortgage stability.

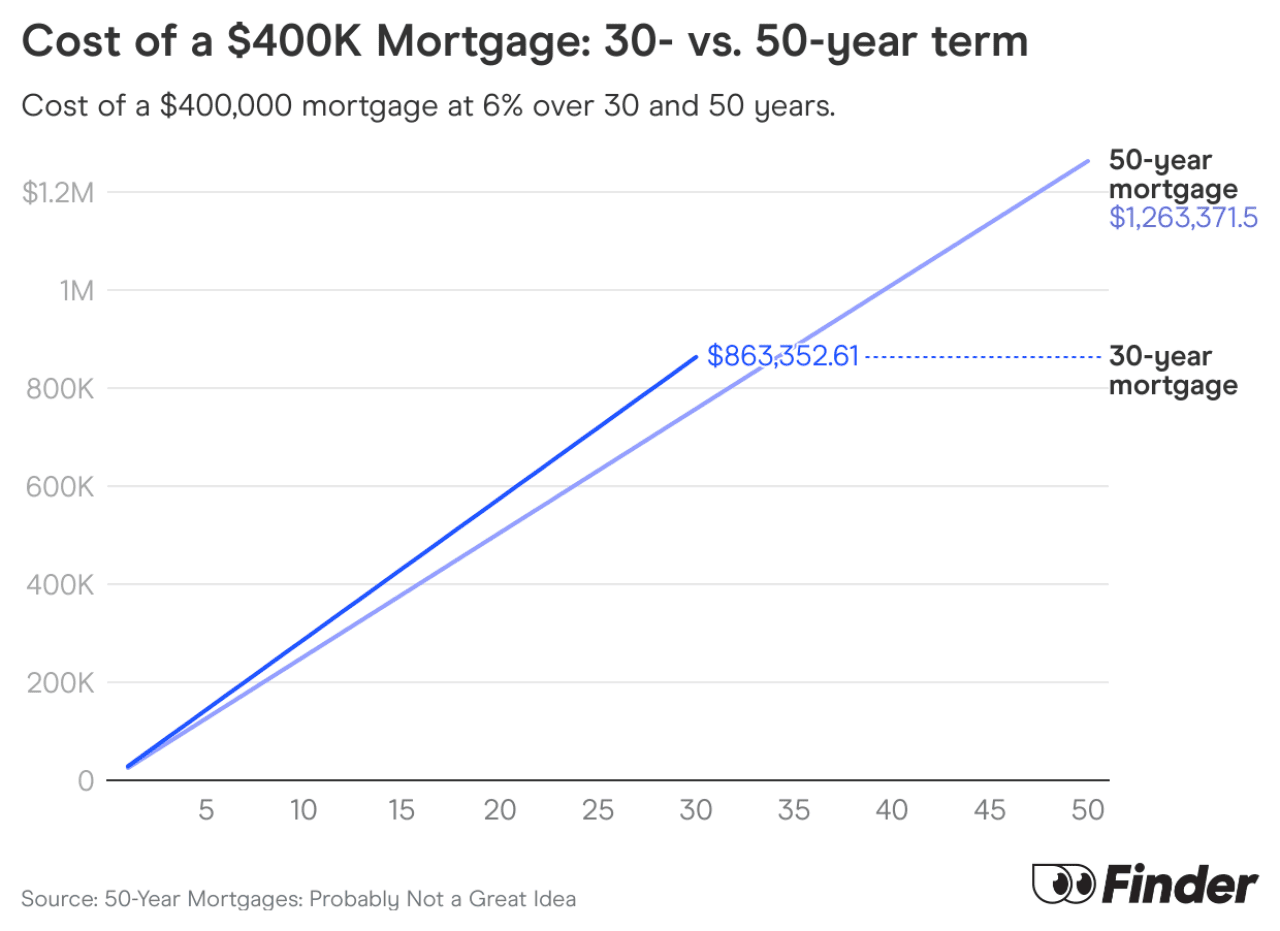

For instance, let’s say you purchase a $400,000 home, and your 50-year mortgage has a 6% rate of interest. Your month-to-month mortgage cost could be $2,105.62.

With mortgages being front-loaded, this implies $2,000 of your first cost goes towards curiosity, and $105.62 goes towards your principal. With a 50-year mortgage, it’ll take practically 20 years earlier than half of your month-to-month cost goes towards your principal.

And in comparison with a 30-year mortgage, stretching a mortgage to 50 years on a $400,000 dwelling solely reduces your month-to-month cost by $292.58.

50-year mortgages can imply double the curiosity

Utilizing the identical instance of a $400,000 dwelling with a 6% rate of interest, right here’s how a lot you’ll pay in curiosity primarily based on the mortgage time period:

- 30-year mortgage: $463,352.76 complete curiosity

- 50-year mortgage: $863,371.51 complete curiosity

Paying practically double the curiosity and being locked in a mortgage for 50 years doesn’t appear value it to cut back a mortgage cost by lower than $300 every month.

50-year mortgages are additionally a nightmare for fairness

House fairness is the distinction between a house’s market worth and the way a lot you owe on the home.

With a 50-year $400,000 mortgage, it could take over 38 years to construct 20% in dwelling fairness (assuming your property worth stays the identical and also you don’t make further funds).

These numbers matter as a result of to refinance your mortgage or keep away from paying mortgage insurance coverage, you want not less than 20% fairness normally.

So for practically 40 years, you’ll have important detrimental fairness on that dwelling mortgage, which isn’t a perfect place to be.

Tremendous lengthy mortgages aren’t a brand new thought, both

Within the late Eighties, Japan tried to make dwelling shopping for extra inexpensive by stretching mortgage phrases. They provided 100-year mortgage phrases, but it surely didn’t have the specified impact.

The thought behind a 100-year mortgage was that the house and debt may very well be handed down by the generations, sort of like generational wealth.

Nevertheless it didn’t actually make dwelling shopping for extra inexpensive for normal of us. As a substitute, prosperous owners had been extra prone to get these long-term mortgages as an estate-planning device to cut back inheritance taxes.

So what can first-time dwelling patrons do?

For those who’re a first-time dwelling purchaser, look into down cost help applications.

For instance, Michigan is providing a First-Technology Down Cost Help Program, which can present qualifying first-time patrons with as much as $25,000 to assist cowl a down cost, closing prices and pay as you go escrows. On the time of writing, this system’s obtainable funds have been dedicated, however applications like this exist.

Give attention to saving a down cost to cut back your month-to-month cost as a substitute of stretching out your mortgage. It’ll simply imply paying extra curiosity in the long term and taking years to personal a bit of your property.

Backside line

Longer mortgages gained’t repair the foundation difficulty of houses being unaffordable — there’s a restricted provide of houses to start with, and a 50-year mortgage can imply paying double the curiosity.

These owners could be locked right into a mortgage and unable to refinance for practically 40 years until they’ll put down a major down cost.

This story was produced by Finder.com and reviewed and distributed by Stacker.