{kind=link}

October 28, 2025

Practically 40% of small companies are on the monetary brink, missing a month of money runway. Discover out why.

Survey: 39% of small companies have lower than a month of money available

Unstable gross sales, rising bills, unpredictable funds: In the present day’s small enterprise math hardly ever balances itself. For a lot of, that provides as much as a day by day money movement puzzle.

Bluevine surveyed 774 U.S. homeowners with $50,000-$5 million in annual income to see how they navigate money movement and put together for crunches, protecting money available, emergency triggers, entry to funding, and the instruments they’re adopting.

Here’s what stood out—and the way small companies can tighten money movement, construct resilience, and keep prepared for what’s subsequent.

Key takeaways

- Practically 4 in 10 SMBs (39%) have lower than one month’s value of working bills in money available.

- 51.3% would faucet emergency reserves inside 48 hours to make payroll—earlier than utilizing them for upcoming taxes or deposits on sudden massive orders.

- 42.8% say entry to money issues greater than returns—solely 18.6% disagree.

- Over two-thirds are curious about AI for money movement administration; “very ” spikes to 54.26% in retail/e-commerce vs. simply 17.6% in transportation/logistics.

- Solely 38% of companies with underneath $250,000 in annual income have a line of credit score vs. 63.4% above $250,000.

- Amongst these looking for funds, 25.6% say funding was tough to acquire, and 39.4% cite excessive rates of interest as the highest mortgage barrier.

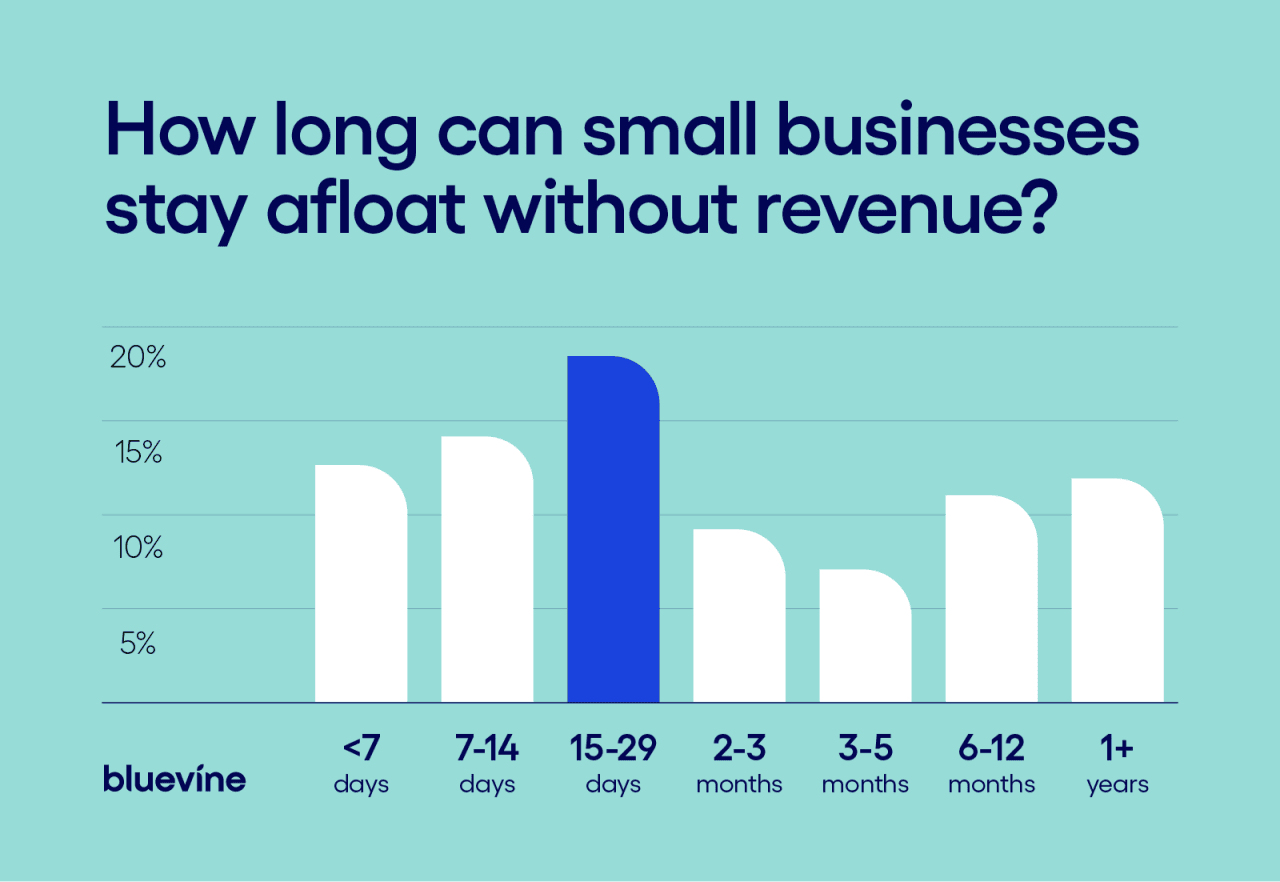

Practically 4 in 10 companies can not cowl greater than a month of bills

Most homeowners don’t preserve the sort of money cushion they need to—and that hole exhibits up quick when payroll, taxes, or a rush order hits. Our survey uncovered that just about 4 in 10 small companies (39%) can not cowl greater than a month of bills within the face of sudden monetary disruptions.

Small enterprise accountant, bookkeeper, and fractional CFO Eric Trettel recommends maintaining a minimum of two to a few months’ value of working bills in reserve. For context, JPMorgan Chase analysis has lengthy flagged that the majority SMBs solely have weeks of buffer (about 18 days).

“For many companies, I’d counsel maintaining eight to 13 weeks’ value of working bills. Companies that gather receivables shortly can most likely preserve much less if gross sales are forecasted to a minimum of keep the identical. Nevertheless, any seasonal enterprise or companies with lengthy buyer fee phrases, ought to intention to maintain further funds to assist cowl bills by durations with much less income. The final word objective is to cowl payroll, hire, and important payments with out counting on short-term borrowing. If the enterprise continues to be rising or has unpredictable gross sales, construct that reserve steadily by setting apart a proportion of month-to-month income till a snug cushion is reached.” – Eric Trettel, Founding father of Sota Bookkeeping

Youthful companies are usually extra uncovered. In our examine, solely 19.6% of companies 5 years outdated or youthful carry three to 12 months of money, in contrast with 39.2% of companies 6 years or older.

And the very youngest battle most with day-to-day protection: 20.7% of companies underneath two years report lower than seven days of money of their checking account (versus 10.5% for these 11+ years). Solo operators face comparable strain as a result of entry to versatile financing is restricted.

That fragility flows into funding. Simply 21.4% of companies lower than a 12 months outdated really feel “very assured” about getting capital, in comparison with 43.7% of 11+ 12 months companies.

To bridge gaps, newer homeowners usually tend to attain for private financial savings: 54% of 1- to 2-year companies have used private funds a minimum of as soon as, in comparison with 37.9% of companies which are 11 years or older.

Find out how to begin constructing enterprise credit score

If your enterprise is new (as much as two years outdated), prioritize constructing credit score and banking relationships now by doing the next:

- Set up enterprise credit score: Get an Employer Identification Quantity (EIN), separate private/enterprise funds, pay distributors on time, and monitor your enterprise credit score scores.

- Open devoted accounts: Use a enterprise checking account for all income and bills to create a clear monetary historical past.

- Safe a modest line of credit score early: Apply whereas money movement is secure, so funds can be found earlier than you want them.

- Formalize banking relationships: Join with a consultant out of your banking platform, talk about merchandise (LOC, overdraft, treasury instruments), and preserve docs up-to-date for quicker approvals.

- Cut back reliance on private funds: Set a goal reserve of three to 6 months of working bills and automate transfers to construct it.

Half of enterprise homeowners would faucet into reserves if payroll have been in danger

Emergency triggers present what retains homeowners up at night time. Payroll comes first—as a result of lacking a payday dangers authorized motion, back-pay claims, and worker belief.

In our survey, 51.3% of homeowners stated they might transfer cash from emergency funds inside 48 hours to make payroll.

Past group morale, federal guidelines require well timed, full fee for hours labored. Failure to take action can result in again wages plus liquidated damages underneath the Honest Labor Requirements Act (FLSA), and state legal guidelines usually add further penalties.

Taxes are subsequent: 40.4% stated an upcoming tax deadline would immediate motion, which tracks with IRS failure to deposit penalties for late employment tax deposits. And 36.4% would act if a big, sudden order required a deposit, selecting to guard income momentum even when it means tapping reserves.

Business patterns matter right here, too. Retail/ecommerce respondents have been practically twice as prone to dip into reserves for provider reductions (25.5%) as these working in skilled/enterprise companies (13.8%).

Early fee phrases, akin to 2/10 web 30, successfully provide double-digit annualized returns for paying suppliers sooner—beneficial if the money to take action is obtainable.

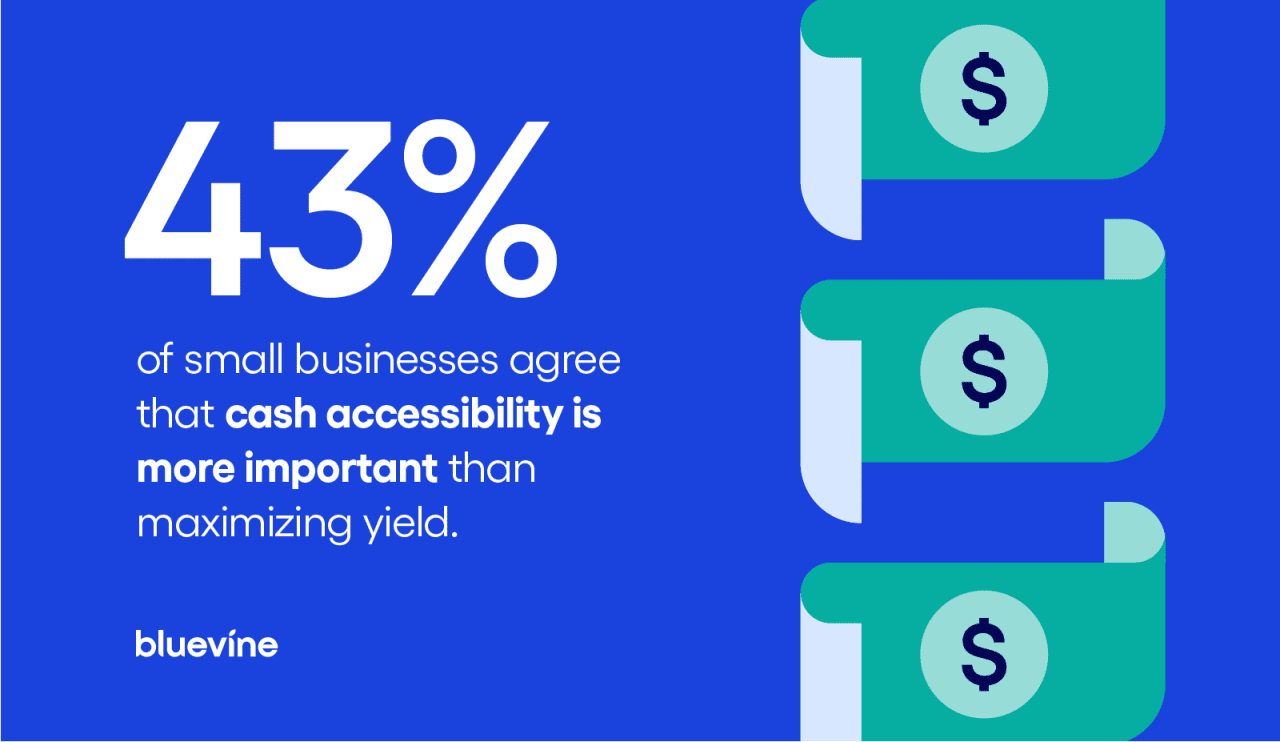

42.8% of small companies preserve cash liquid, even when it means decrease returns

House owners are nonetheless favoring reach-for-it-now money over higher-yield choices. In our survey, 42.8% agreed that entry to money issues greater than maximizing returns, whereas 18.6% disagreed.

That tilt towards liquidity suits the second. Pandemic-era shocks confirmed how shortly money wants can change and the way skinny buffers may be, a lesson echoed by current findings on small companies in misery.

Our analysis on would-be enterprise founders exhibits folks favor quick fee processing/funds availability and quick access to credit score/loans over high-interest accounts—alerts that liquidity and dealing capital outrank rate-chasing when cash wants to maneuver shortly.

Warning can be exhibiting up in sentiment knowledge. The Nationwide Small Enterprise Affiliation’s newest report highlights financial uncertainty as the highest problem for homeowners. Practically 60% say it’s their largest hurdle, the best in 13 years—which makes maintaining money versatile really feel safer than chasing yield.

When demand is uneven or insurance policies are in flux, liquidity buys time to make payroll, cowl taxes, and seize pressing orders with out scrambling for financing.

Over two-thirds of companies are curious about AI finance instruments

House owners are leaning into AI for day-to-day finance work like money movement forecasting, bill dealing with, and quicker collections. In our survey, 67.9% of companies stated they’re curious about AI instruments for money movement administration, and solely 13% are opposed. Curiosity is broad throughout firm ages, suggesting AI is shifting from “good to have” to plain tooling.

There’s a significantly sharp divide amongst industries:

- In retail/ecommerce, 54.26% of respondents reported being very curious about AI finance instruments.

- In know-how/SaaS, 44.8% of respondents stated they’re very .

- In transportation/logistics, solely 17.6% of respondents chosen “very .”

Collectively, these outcomes counsel that AI finance curiosity runs greater in transaction-heavy sectors like retail/ecommerce and tech, and decrease in logistics, the place the payback is much less fast.

Many SMBs are already embracing AI. A current Intuit QuickBooks survey of two,200 U.S. small companies discovered that 68% now use AI often, up from 48% in 2024. In finance particularly, typical functions embrace AP/AR automation—OCR and machine studying that learn invoices, route approvals, and predict late funds.

Lower than 40% of companies making $250K or much less have credit score strains in case of emergencies

Increased-revenue companies are higher ready for shocks—they usually are likely to act quicker when charges transfer.

On this survey, 63.4% of companies incomes greater than $250,000 per 12 months preserve a line of credit score (LOC) for emergencies, in contrast with simply 38% of companies incomes lower than $250,000.

Smaller companies even have much less capability to soak up massive gaps: Solely 7.7% of companies with lower than $250,000 in income might cowl a $100,000 shortfall, in comparison with 61.3% of companies with greater than $1 million in income.

Refinancing conduct within the survey aligns with this entry hole. If charges drop, 45.5% of corporations making larger than $1 million say they might refinance debt, in comparison with 33% of companies incomes lower than $250,000.

The highest cause smaller companies wouldn’t refinance was easy: “I don’t have any enterprise debt” (44.8%). This was in step with decrease LOC utilization amongst sub-$250,000 companies (38%).

Briefly, extra income usually means extra credit score instruments and extra methods to reply shortly to altering circumstances.

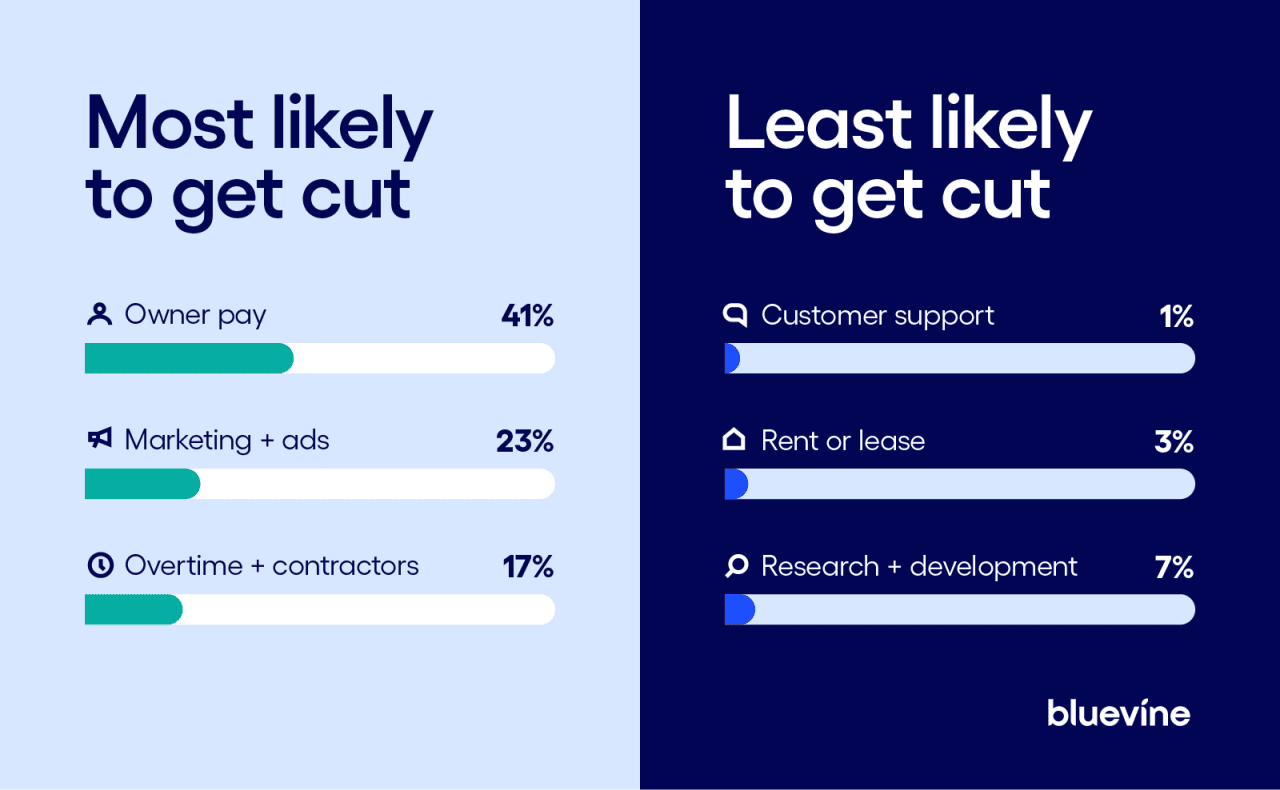

41% of enterprise homeowners would reduce their pay earlier than anything in a money crunch

In tough financial occasions, it’s normally the homeowners who take the primary hit.

This survey revealed that the primary transfer homeowners would make when cash will get tight is to chop their very own pay (41.1%).

The subsequent lever was advertising and marketing/advert spend (22.9%), exhibiting how shortly discretionary budgets get trimmed.

Solely a tiny share would begin with buyer assist/consumer companies (1.4%), underscoring how vital service is to retention and income.

The survey additionally revealed that group dimension performs a job in deciding what to chop:

- Bigger groups reduce proprietor pay first extra usually: 73% of companies with 250 or extra staff would cut back proprietor pay in a crunch, versus 52% of solopreneurs.

- Greater companies have extra levers to tug: Corporations with 10 or extra staff usually tend to reduce extra time or contractors first (23.4%) than solopreneurs (10.1%).

For these causes, many consultants suggest making use of for financing when your enterprise funds are wholesome, so funds can be found when money will get tight.

Eric Trettel, proprietor of Sota Bookkeeping, says, “One of the best time to safe financing is earlier than you really want it. Take into account making use of for a line of credit score proper after tax season or throughout a robust quarter, when your monetary statements greatest symbolize the enterprise’s stability.”

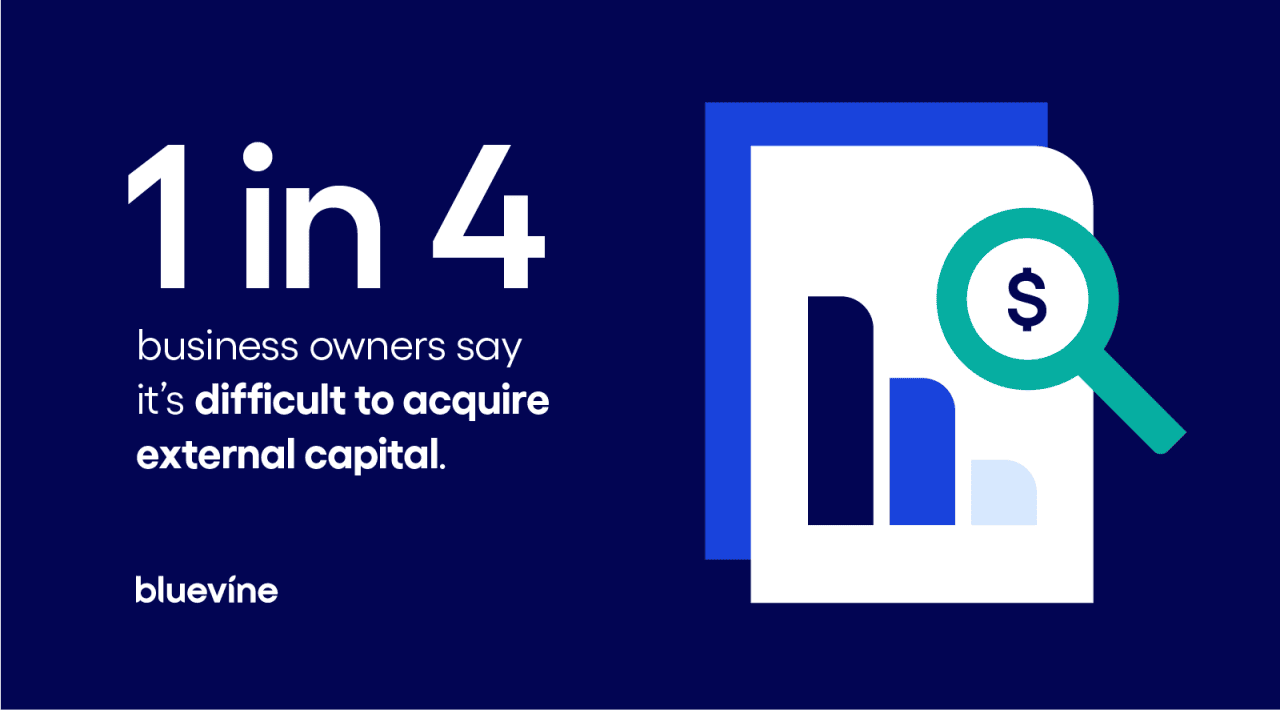

1 / 4 of enterprise homeowners say it’s tough to amass exterior capital

House owners are searching for funding, however based on this survey, that’s simpler stated than executed. Of the 68.2% of homeowners looking for exterior capital previously 12 months, one in 4 candidates (25.6%) stated it was tough to acquire.

The most important ache factors have been:

- Low credit score scores (8.1%)

- Restricted working historical past / skinny credit score recordsdata (6%)

- Unclear choices throughout underwriting (5.9%)

This tracks with business tendencies: The Federal Reserve stories that software charges held regular in 2024 whereas approval satisfaction fell.

Many homeowners keep away from new loans for 2 easy causes:

- They don’t need to add debt (31.4%): Debt aversion skews towards smaller corporations—84% of those that selected “don’t need extra debt” have fewer than 25 staff.

- Complete value is unclear (charges, APR, prepayment penalties) (15.6%): This pricing difficulty is concentrated at bigger companies (45% of 100+ worker corporations vs. 13% of corporations with underneath 25 staff).

Latest coverage strikes intention to enhance readability. The CFPB’s Part 1071 knowledge assortment rule (now shifting ahead after courtroom challenges) would require lenders to gather and report standardized knowledge on small enterprise credit score functions, which ought to make pricing and approval standards extra clear and comparable for homeowners.

Roughly 40% of small enterprise homeowners cite excessive rates of interest as the highest mortgage barrier

House owners are watching charges, and even after the Fed’s September quarter-point reduce, most plan to carry off on new hires or huge advertising and marketing pushes till circumstances really feel steadier.

In reality, 39.4% cited “charges are nonetheless too excessive” as their largest barrier to asking for a enterprise mortgage proper now.

In our knowledge, the top-cited strikes if charges fall are nonetheless constructing emergency reserves (21.3%) and paying down principal (21.1%), with far fewer planning to ramp advertising and marketing (13.8%), rent (3.4%), or speed up vacation spend (5%).

The Fed’s minutes additionally signaled assist for additional price cuts, however companies seem like ready for clearer circumstances earlier than shifting from balance-sheet restore to progress.

How homeowners would use financial savings if charges drop additionally varies by dimension:

- 21% of $1M+ companies say they might pay down principal quicker; within the $250,000-$999,000 band, that rises to 23.3%.

- For the smallest companies (

Put liquidity first with enterprise checking

The image is obvious: Many homeowners are working with skinny buffers, prioritizing entry to money over yield, and staying conservative about new borrowing. When circumstances shift, companies with the appropriate accounts, credit score instruments, and workflows already in place are those that transfer first.

Methodology

Centiment Viewers carried out this survey of 774 U.S. enterprise homeowners with $50K–$5M in annual income for Bluevine between September 25 and September 30, 2025. Information are unweighted, and the margin of error is roughly +/-3% for the general pattern on the 95% confidence degree.

This story was produced by Bluevine and reviewed and distributed by Stacker.

RELATED CONTENT: Let’s Get It! Jeezy’s Electrifying ‘TM:101’ Tour Finale In Detroit Ends With Upcoming Album & Las Vegas Residency Announcement