{kind=link}

Within the ever-evolving world of tax laws, staying on prime of adjustments which may have an effect on your monetary state of affairs is essential. For the primary half of this 12 months, the enterprise mileage price stood at 58.5 cents, which many people are accustomed to. Nevertheless, within the 12 months’s second half, it bumped barely to 62.5 cents. Medical and shifting bills elevated from 18 to 22 cents for the latter half. In the meantime, safety bills remained regular at 14 cents. Whereas the precise origins of those charges could seem shrouded in thriller, one fixed is the unchanging debt element.

Nevertheless, what has but to shift is the depreciation element of enterprise mileage, which generally constitutes about half of the usual mileage price. Surprisingly, regardless of the speed adjustment, this element remained untouched. Why? Properly, the wrongdoer behind the speed fluctuation is the worth of gasoline. Fortunately, which means that the depreciation side stays constant all year long.

So, when your purchasers come knocking with their questions and confusion, some would possibly come armed with meticulous calculations for each halves of the 12 months, whereas others would possibly have a look at you a bit misplaced. The way you deal with this discrepancy is the place your private contact comes into play. Whether or not you advise a easy cut-in-half strategy or information them by the intricacies, your experience, and magnificence make all of the distinction in navigating these tax adjustments. Keep knowledgeable, keep adaptable, and hold serving to your purchasers make sense of the ever-changing tax panorama.

|

Customary Mileage Charges |

Jan 1 – June 30 |

July 1 – Dec 31 |

|

Enterprise mileage |

58.5 cents |

62.5 cents |

|

Medical and shifting |

18 cents |

22 cents |

|

Charity |

14 cents |

14 cents |

Subheading 3.13: Medicare Half B & 2022 Premiums

Navigating Medicare generally is a monetary rollercoaster, and here is the twist: your Half B premium can skyrocket primarily based in your revenue. In 2022, the usual Half B premium is $170.10, however for people with an revenue under $91,000 or $182,000 for {couples}. Now, brace your self. The premium takes off like a rocket in case your revenue exceeds these thresholds. For these incomes between $91,000 and $114,000 for people, or $182,000 to $228,000 for {couples}, that $170.10 turns into $238.10 per 30 days – that is a $68 soar. However wait, there’s extra! In the event you’re within the subsequent revenue bracket, $114,000 to $142,000 for people or $228,000 to $284,000 for {couples}, your premium skyrockets to a staggering $340.20 per 30 days, double the usual quantity. So, for those who all of the sudden discover your revenue hovering on account of a property sale or a crypto windfall, do not be shocked when your Medicare Half B premium follows go well with two years later. It is important to tell purchasers about this potential monetary shock and advise them on submitting the required SSA kinds to handle uncommon revenue adjustments. In spite of everything, no one needs to be blindsided by a doubled Medicare invoice.

COVID Repayments

In 2020, amidst the chaos of the COVID-19 pandemic, the IRS launched a singular provision – the Coronavirus Catastrophe Retirement Plan Distributions. This program allowed people to withdraw as much as $100,000 from their IRAs or retirement plans with out going through the standard 10% penalty. What made it outstanding was the self-certification side; it wasn’t about proving how severely the pandemic had impacted one’s life, however somewhat a versatile measure to assist individuals navigate the monetary challenges posed by the pandemic. The thought was easy: empower people to entry their retirement funds as a lifeline throughout these unsure instances. Whereas it might need raised eyebrows for some, it demonstrated a dedication to supporting these going through monetary turmoil as a result of pandemic.

Subheading 4.1 The 8915 Sequence

Type 8915-F is a revamped model of the previous Type 8915. Beginning in 2021, there will not be extra alphabetically labeled variations of this way (like Type 8915-G or Type 8915-H). As an alternative, Type 8915-F will likely be used for reporting distributions associated to certified 2020 disasters and any certified disasters which will happen in 2021 and past, if relevant. The checkboxes in objects A and B on the shape assist establish the particular 12 months and nature of the reported disaster-related distributions. Beforehand, there have been separate kinds for annually’s disasters.

So, who ought to file Type 8915-F? Anybody who acquired a certified catastrophe distribution from an eligible retirement plan acquired a certified distribution, included a certified catastrophe distribution from a previous 12 months of their revenue over three years (with that interval nonetheless ongoing), or made a reimbursement of a certified catastrophe distribution. It is essential to notice that this way remains to be mandatory if not one of the distribution was reported as taxable revenue in 2020. Additionally, do not forget that the reimbursement deadline relies on the distribution date, not the tax return due date.

Subheading 4.2: Kiddie Tax

The “Kiddie Tax” is a provision that impacts kids’s taxation, and it applies if a baby meets sure standards. Firstly, a baby should be below 18 on the finish of the tax 12 months or be between 19 and 24 and a full-time pupil with out incomes greater than half of their help. Moreover, they need to have unearned revenue exceeding $2,300, together with varied varieties of revenue like curiosity, dividends, and extra. If a baby’s mother or father is alive on the finish of the tax 12 months, and the kid should file a tax return however would not file a joint return, the kiddie tax applies. These guidelines additionally prolong to legally adopted and stepchildren, no matter their dependent standing. The kiddie tax means a baby’s revenue could also be taxed at their mother and father’ larger marginal tax charges. This tax is reported utilizing both Type 8615 for the kid or Type 8814 on the mother or father’s return. Understanding these guidelines is essential for households to navigate their tax tasks successfully.

2022 Revisions for the Type 1040 S

Subheading 5.1: Adjustments to Schedules 1 by 6

- Schedule 1: Internet working loss and playing revenue are nonetheless there, however different objects like cancellation of debt, overseas earned revenue exclusion, and taxable well being financial savings account distributions have made their means into the highlight. There’s additionally a point out of actions not engaged in for revenue, together with pastime revenue and inventory choices. Surprisingly, there’s even a line merchandise for Olympic medal winners!

- Schedule 2: Line 8 now features a checkbox that claims, “If not required, verify right here.” Oddly sufficient, they nonetheless want to clarify this transformation. Additionally, “The Superior Baby Tax Credit score” funds aren’t any extra; for a lot of, that is not a trigger for sorrow.

- Schedule 3: We observe a brand new function on line E, which is split into two elements: the choice motorized vehicle credit score (Type 8910) and the certified plug-in motorized vehicle credit score (Type 8936).

- Schedules 4, 5, and 6: The Finish of Pandemic Adjustments Schedule 4 has bid farewell to extra pandemic-related objects. Likewise, Schedule 5 and Schedule 6 have seen the tip of pandemic adjustments. This offers us a glimpse of Schedule 8812 for 2022, although it is essential to notice that this data relies on a draft model.

Subheading 5.2: Charitable Deductions & Limits

The principles surrounding charitable contribution deductions might be complicated, however they’re important to understanding for anybody seeking to maximize their tax advantages whereas supporting charitable causes. Usually, people can deduct as much as 60% of their Adjusted Gross Earnings (AGI) in relation to money donations. Noncash contributions, alternatively, have a decrease restrict at 50% of AGI. Nevertheless, contributions to particular organizations like veterans’ teams and nonprofit cemeteries have an additional lowered restrict of 30% of AGI. This 30% restrict additionally applies to items of long-term capital achieve property until the donor chooses to scale back the property’s Truthful Market Worth (FMV) by the potential long-term capital achieve quantity, through which case the 60% restrict applies.

Here is an essential replace: In 2021, the Taxpayer Certainty and Catastrophe Aid Act suspended the 60% limitation on money charitable contributions, permitting taxpayers who itemized and donated money to deduct as much as 100% of their AGI. This was a short lived provision for that 12 months solely, and it is essential to notice that the 100% deduction restrict expired after 2021 and has but to be prolonged to 2022. Due to this fact, whereas the tax panorama can change, staying knowledgeable in regards to the newest laws and consulting a tax skilled to benefit from your charitable giving whereas staying inside the established limits is at all times advisable.

Subheading 5.3: Charitable Deduction Carryover

Relating to charitable contributions and taxes, it is important to know how revenue limitations can affect your deductions. In the event you can not totally deduct your charitable contributions in a given 12 months on account of revenue restrictions, there is a silver lining. The tax code permits you to carry over the surplus quantity for as much as 5 years, providing some aid. Nevertheless, it is essential to bear in mind that any remaining charitable contribution carryover past that interval will likely be forfeited. Moreover, it is essential to notice that the identical revenue limitations that utilized within the 12 months the preliminary contribution was made will proceed to use to the carryover years. So, whereas this provision gives flexibility for these going through revenue restrictions, planning your charitable giving technique thoughtfully is important to maximise your deductions successfully.

Tax Extenders

Subheading 6.1: Mortgage Insurance coverage Premiums

Premiums paid or accrued for certified mortgage insurance coverage, generally known as non-public mortgage insurance coverage (PMI), in reference to acquisition indebtedness pertaining to a certified residence of the taxpayer are handled as certified residence curiosity. As such, they’re deductible on Schedule A, Itemized Deductions. Nevertheless, it is essential to notice that as of the present data accessible, the deduction for PMI premiums has not been prolonged to the tax 12 months 2022. Taxpayers ought to keep knowledgeable about any updates or adjustments to tax laws which may have an effect on their eligibility for this deduction.

Subheading 6.2: Principal Residence Indebtedness Exclusion

The Taxpayer Certainty and Catastrophe Tax Aid Act has introduced vital monetary aid for owners. This Act retroactively prolonged the exclusion from revenue for discharges of certified mortgage debt on a taxpayer’s principal residence, permitting for as much as $750,000 ($375,000 for married people submitting individually) for discharges occurring after 2020. This exclusion comes into play when taxpayers face varied homeownership challenges, reminiscent of restructuring their acquisition debt, foreclosures on their principal residence, or participating in a brief sale. Furthermore, the Consolidated Appropriations Act of 2021 additional extends this precious provision, guaranteeing that the certified principal residence indebtedness exclusion stays in impact for tax years earlier than January 1, 2026. This extension gives owners with much-needed monetary flexibility and safety throughout these unsure instances.

Subheading 6.3: Baby Tax Credit score

The Baby Tax Credit score (CTC) is a big monetary profit for households with qualifying kids below the age of 17. It affords a tax credit score of as much as $2,000 per baby, and as much as $1,500 of that quantity is refundable, that means that even when your tax legal responsibility is decrease than the credit score, you may nonetheless obtain a portion as a refund. Nevertheless, it is important to notice that the kid should have a Social Safety quantity (SSN) to qualify for this credit score. One other noteworthy side of the CTC is that it is accessible for married people submitting separate (MFS) returns, providing flexibility in claiming the credit score. Moreover, when figuring out who will get to assert the credit score, the mother or father claims the kid on their tax return, no matter custodianship. Lastly, bear in mind that phaseouts for the CTC, which aren’t listed for inflation, kick in when your Adjusted Gross Earnings (AGI) exceeds $200,000 for single filers and $400,000 for these submitting collectively, regularly decreasing the credit score quantity as revenue rises.

Subheading 6.4: Baby Tax Credit score Expired Provisions

In 2021, vital adjustments had been made to the Baby Tax Credit score (CTC) in response to the COVID-19 pandemic. The age restrict for a qualifying baby was prolonged to these below 18, and the credit score quantity noticed a considerable enhance, with $3,000 allotted per baby and a formidable $3,600 for these below the age of 6. Moreover, new phaseout thresholds had been launched to find out eligibility, with limits set at $150,000 for married submitting collectively or qualifying widow(er) statuses, $112,500 for heads of family, and $75,000 for single filers or married people submitting individually. An essential growth was that the credit score turned 100% refundable for many taxpayers in 2021, offering a big monetary profit. Moreover, advance baby tax credit score funds had been launched to assist households obtain this very important help all year long. Nevertheless, it is important to notice that these enhanced provisions solely utilized to the 2021 tax 12 months, and as of now, they’ve but to be prolonged into 2022, signaling a shift within the panorama of this essential tax profit.

Subheading 6.5: Dependent Care Tax Credit score Expired Provisions

The Baby and Dependent Care Credit score underwent vital adjustments in 2021, providing precious advantages that sadly expired on the finish of that 12 months. These provisions included a most eligible expense restrict of $8,000 for one qualifying individual or a formidable $16,000 for households with two or extra qualifying people. Moreover, the credit score price elevated to 50% for these with an revenue of $125,000 or much less, offering substantial aid however phased out totally for these incomes greater than $438,000. A key function was that the credit score turned refundable in 2021, benefiting taxpayers (or their spouses if submitting collectively) who resided in america for over half the 12 months. Moreover, the enlargement included the next exclusion quantity of $10,500 (or $5,250 for these submitting individually) for employer-provided dependent care help.

Subheading 6.6: Earned Earnings Tax Credit score

At the start, the minimal age to assert the EIC for childless people was lowered from 25 to 19, though full-time college students wanted to be at the least 24 years previous. Moreover, the utmost age restrict of 65 for claiming the childless EIC was fully eradicated, permitting extra people to qualify. This transformation additionally considerably elevated the utmost EIC quantity, which reached a excessive of $1,502.

Nevertheless, it is essential to notice that these adjustments had been solely particular to the 2021 tax 12 months. In 2022, the foundations reverted to a narrower age vary for these claiming the EIC with out kids, aged 25 to 64, and the utmost EIC quantity decreased to $560. Taxpayers should keep knowledgeable about such adjustments and adapt their tax planning accordingly to benefit from accessible credit and deductions.

Subheading 6.7: Premium Tax Credit score

In Part 36B of the tax code, a noteworthy provision comes into play for people who acquired unemployment compensation throughout 2021. If you end up on this state of affairs, here is what it’s essential to know: Firstly, you will be thought of an “relevant taxpayer” for this part. Secondly, the calculation of your eligibility for the refundable credit score for protection below a certified well being plan is totally different. Usually, family revenue performs a vital function in figuring out this credit score. Nonetheless, in your case, solely the portion of your revenue exceeding 133 % of the poverty line for a household of your dimension will likely be taken into consideration. This provision goals to offer some monetary aid to those that confronted unemployment through the difficult 12 months of 2021, making healthcare protection extra accessible for many who want it most.

Different new stuff

Heading 7.1 : Frequent Tax Issues

Navigating the labyrinthine world of taxes might be daunting, and several other widespread tax issues can journey up even essentially the most conscientious taxpayers. One challenge typically arises from the revenue misattribution reported on a 1099-Okay type. This could happen when taxpayers obtain a 1099-Okay below their Social Safety Quantity (SSN), however the revenue belongs to a partnership or company they’re concerned with. Sharing a cost terminal with one other individual or enterprise can additional complicate issues, because the 1099-Okay could report revenue for each events, creating potential discrepancies.

One other tax pitfall arises when a taxpayer must replace their Taxpayer Identification Quantity (TIN) and enterprise title related to a bank card terminal after buying or promoting a enterprise through the 12 months. This oversight can result in misreported revenue and IRS inquiries.

Money-back choices throughout purchases are tempting, however they arrive with tax implications. When a enterprise permits cash-back, the money acquired is often thought of a part of the revenue and should be reported accordingly.

Moreover, companies counting on a single cost terminal for a number of revenue sources can face issues. Every supply of revenue ought to be tracked and reported individually, however once they all movement by the identical terminal, it turns into a problem to make sure correct reporting. These widespread tax issues underscore the significance of meticulous record-keeping and staying up-to-date with tax laws. Consciousness of those points and searching for skilled steering may also help taxpayers navigate the complicated tax panorama and keep away from potential pitfalls.

Sub-Heading 7.2: Type 1099-Okay

In a big change that took impact in 2022, a brand new regulation has led to a pointy discount within the reporting threshold for third-party cost settlement entities. This alteration, introduced into motion by the American Rescue Plan Act (ARPA), has far-reaching implications for companies and people concerned in cost transactions. To know this shift totally, let’s delve into the background. For over a decade, cost settlement entities had been mandated to file Type 1099-Okay yearly with the IRS, reporting the gross quantity of reportable cost transactions for payees. This requirement utilized to transactions that occurred between 2010 and 2021.

Throughout this era, third-party settlement organizations loved a de minimis exception, exempting them from submitting Type 1099-Okay for payees with 200 or fewer transactions through the calendar 12 months so long as the mixture gross quantity remained at $20,000 or much less. Nevertheless, ARPA ushered in a considerable change by amending this de minimis threshold. Ranging from calendar years starting after December 31, 2021, the brand new threshold is ready at $600, with no minimal variety of transactions required.

This shift has far-reaching implications, as many payees will probably obtain Type 1099-Okay, which should be despatched out by January 31 following the tip of the reporting 12 months. Understanding and complying with these new laws is important for companies and people engaged in varied cost transactions to keep away from potential penalties and guarantee compliance with the regulation. The panorama of monetary reporting has advanced, ushering in adjustments that demand our consideration and understanding within the years forward.

Taxpayers have to be diligent when tax season rolls round, particularly in the event that they’ve acquired a 1099-Okay type. To make sure accuracy, begin by cross-referencing the quantity on the shape along with your cost card receipt data and service provider statements. Preserve going; meticulously overview your data to substantiate that your gross receipts align with what’s reported in your tax return. It is essential to account for all cost kinds you have acquired, whether or not money, checks, or bank cards, as these ought to all be included in your gross receipts. Lastly, preserve complete documentation that helps your reported revenue, as thorough record-keeping is your greatest ally throughout tax time. By following these steps, you may confidently navigate your tax obligations and decrease the probabilities of encountering any sudden surprises.

Proposed Laws

Sub-Heading 8.1: Safe 2.0 Act

One promising growth on the horizon is the Safe 2.0 Act. At the moment, each the Home and Senate have crafted variations of this formidable invoice, with many overlapping provisions but additionally key variations that have to be reconciled. The prospect of Safe 2.0 changing into regulation has garnered vital consideration from specialists, lots of whom anticipate its passage in 2022.

Ranging from tax years after December 31, 2023, vital adjustments are coming for taxpayers aged 62 to 64 concerning catch-up contributions. The catch-up quantities are set to see substantial boosts: the retirement catch-up contribution will surge from $6,500 to $10,000, whereas the SIMPLE catch-up contribution will enhance from $3,000 to $5,000. Moreover, the $1,000 catch-up for IRAs will likely be listed for inflation. One peculiar side is that these catch-up contributions will likely be handled as Roth accounts for tax functions, implying that they will not take pleasure in tax deferral advantages. This shift is poised to affect the monetary methods of people on this age group, and cautious planning will likely be important to maximise their retirement financial savings successfully.

A standout function of the Safe 2.0 Act is its proposed penalty discount for failing to take required minimal distributions (RMDs) from retirement accounts. Below the present system, people who miss these distributions face a hefty 50% penalty. Nevertheless, if this laws is enacted, that penalty could be lowered to 25% and 10% if the error is promptly corrected.

RBD’s would enhance as follows:

- 73 beginning in 2023

- 74 beginning in 2030

- 75 beginning in 2033

In a transfer designed to spice up retirement financial savings, the Act mandates that employers auto-enroll eligible individuals in §401(okay) or §403(b) plans, initiating contributions at 3% and regularly growing them by 1% annually till they attain 10%. It is essential to notice that current plans and small companies with 10 or fewer staff are exempt from this requirement, which applies solely to new plans established after the laws’s enactment date.

One other noteworthy function of the Safe 2.0 Act is its recognition of the significance of charitable giving. The invoice permits a one-time switch of as much as $50,000 to a charitable reward annuity or charitable the rest belief, encouraging philanthropy and monetary planning.

The Safe 2.0 Act additionally acknowledges the altering panorama of employment by decreasing the requirement for workers to take part in a §401(okay) retirement plan. Beforehand, people wanted 500 service hours in 3 consecutive years to qualify. With Safe 2.0, this threshold is lowered to simply two consecutive years, making retirement advantages extra accessible to a broader vary of employees.

In conclusion, The Safe 2.0 Act represents a big step towards enhancing retirement safety for People. With its revolutionary provisions aimed toward decreasing penalties, boosting financial savings, and inspiring charitable giving, this laws might usher in a brand new period of monetary stability and well-being for retirees and future generations. Because it continues its journey by the legislative course of, the Safe 2.0 Act guarantees a safer monetary future for all.

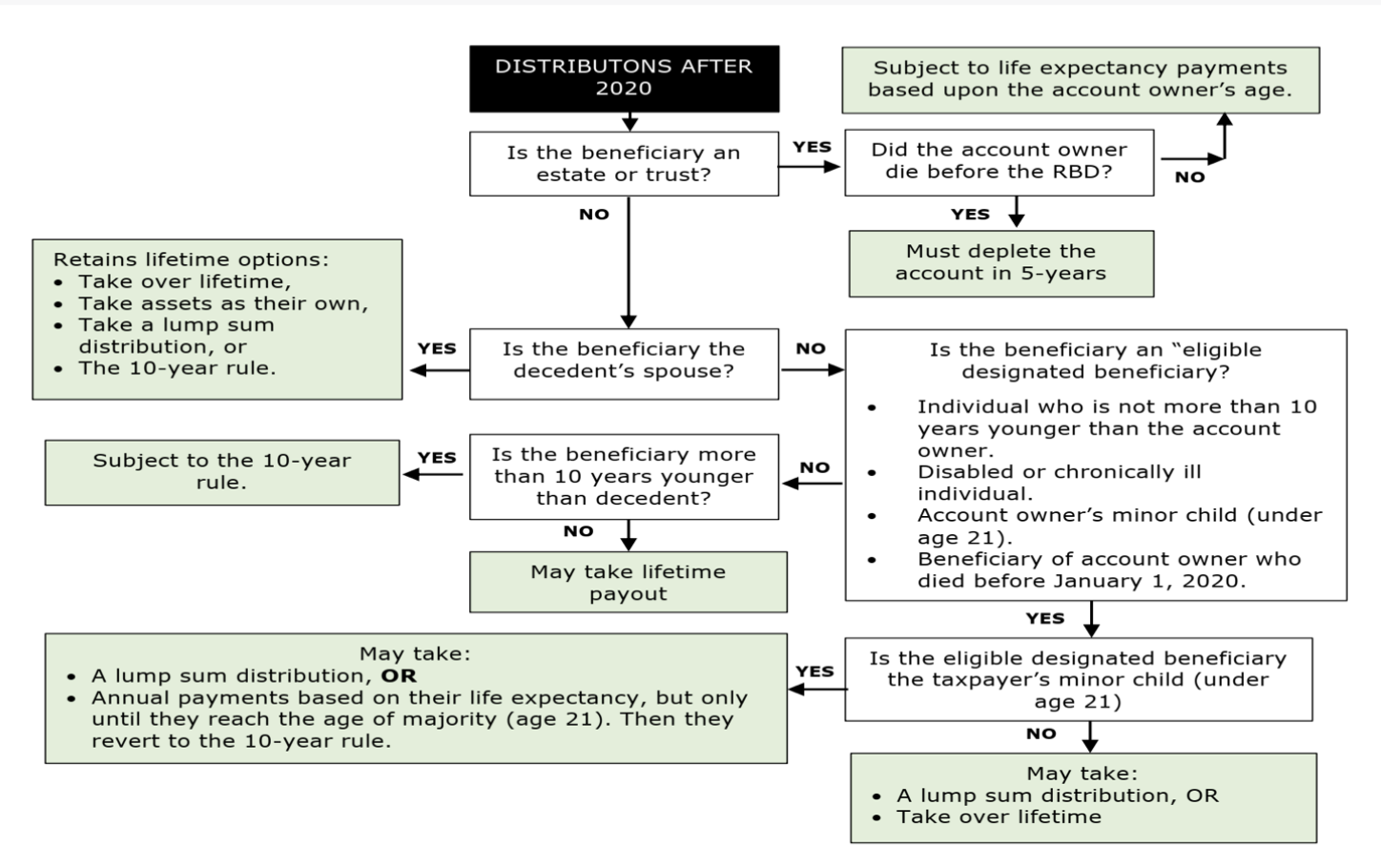

Safe 2.0 Circulate Chart

Subheading 8.2: Understanding the First-Time Homebuyer Credit score: A Nearer Take a look at the 2021 Adjustments

In the event you’ve been contemplating making the leap into homeownership, the First-Time Homebuyer Act of 2021 brings some thrilling adjustments to the desk. Launched in April 2021, this laws brings a recent perspective to the first-time homebuyer tax credit score, probably making the dream of proudly owning your individual house extra attainable than ever earlier than.

Below this new act, eligible first-time homebuyers can take pleasure in a credit score amounting to 10% of the acquisition worth of their principal residence, with a cap set at a most of $15,000. It is essential to notice that if two or extra single taxpayers determine to embark on this journey collectively and buy a house, the mixed credit allowed to all events concerned can not surpass the $15,000 most threshold.

Now, what precisely does it imply to be a first-time homebuyer? In response to the act, a person (and their partner if married) qualifies as a first-time homebuyer in the event that they meet two essential standards. Firstly, they have to not have held any possession curiosity in any residence through the three-year interval main as much as the date of their principal residence’s buy. Secondly, they have to not have claimed this credit score in any earlier taxable 12 months.

Nevertheless, it is important to know that this credit score is not accessible to everybody. The act stipulates that no credit score will likely be granted to taxpayers whose Modified Adjusted Gross Earnings (MAGI) exceeds a sure threshold. Particularly, the brink is ready at 160% of the Space Median Earnings as decided by the Secretary of Housing and City Improvement. This determine takes into consideration components reminiscent of the realm through which the principal residence is positioned, the scale of the taxpayer’s family, and the calendar 12 months through which the principal residence is bought.

Aspiring owners ought to take a better have a look at these provisions to totally grasp the potential advantages and limitations of the First-Time Homebuyer Act of 2021. This laws is designed to offer much-needed help for these seeking to make their first foray into homeownership, nevertheless it’s important to navigate the intricacies to make sure you’re benefiting from this chance.

Subheading 8.3: Accountable Monetary Innovation Act

The Accountable Monetary Innovation Act emerges as a beacon of hope, aiming to streamline the combination of current banking and tax legal guidelines right into a complete regulatory framework for digital property. At its core, this groundbreaking laws seeks to offer readability and construction to the world of cryptocurrencies and blockchain know-how. The Act lays out a meticulous definition of digital property, encompassing a broad spectrum of natively digital property that bestow financial, proprietary, or entry rights by using cryptographically secured distributed ledger know-how. This all-encompassing definition spans digital currencies, ancillary property, cost stablecoins, and different securities and commodities that meet the required standards.

One of the noteworthy provisions of the Act is its therapy of digital property obtained by mining or staking actions. In response to the Act, these property wouldn’t set off tax implications till they’re offered, providing a welcome aid to these actively collaborating in blockchain networks. Furthermore, the Act redefines the regulatory panorama by categorizing most digital currencies as commodities below the jurisdiction of the Commodity Futures Buying and selling Fee (CFTC), somewhat than subjecting them to Securities and Trade Fee (SEC) oversight.

Digital asset exchanges, typically the lifeblood of the crypto ecosystem, are acknowledged as monetary establishments below this laws, additional cementing their function within the broader monetary sector. Cost stablecoins, particularly these issued by banks or credit score unions, are given a singular standing; they’re neither commodities nor securities, signifying a recent strategy to those revolutionary monetary devices.

Maybe one of the crucial vital steps ahead is the Act’s stringent necessities for stablecoins pegged to the US greenback. These issuers are mandated to take care of high-quality liquid property equal to 100% of all excellent stablecoins, guaranteeing their stability and safeguarding in opposition to potential crises. Moreover, issuers should possess the potential to redeem stablecoins at par, instilling belief and reliability within the stablecoin ecosystem.

In an period the place digital property are reshaping the monetary panorama, the Accountable Monetary Innovation Act emerges as a pioneering pressure, putting a fragile steadiness between innovation and regulation. By offering a transparent regulatory framework, the Act guarantees to foster a safer and accessible surroundings for digital property, ushering in a brand new period of accountable monetary innovation.

Subheading 8.4 : Digital Forex Tax Equity Act

In February 2022, a big legislative proposal took middle stage on the earth of cryptocurrencies: the Digital Forex Tax Equity Act. This act, if handed, guarantees to convey some much-needed readability and equity to the taxation of digital forex transactions. Below the provisions of this act, private transactions made with digital forex could be exempt from taxation if the positive factors quantity to $200 or much less. It is a welcomed growth for crypto fanatics and advocates who’ve lengthy argued that the tax therapy of digital forex ought to mirror its supposed objective – enabling peer-to-peer transactions with out the burden of extreme taxation. The act’s potential affect on the cryptocurrency panorama is important, because it paves the way in which for a extra seamless and user-friendly expertise in relation to utilizing digital property for on a regular basis transactions. It stays to be seen whether or not this act will turn into regulation, nevertheless it undoubtedly represents a step ahead within the ongoing effort to create a good and balanced regulatory framework for the burgeoning world of digital currencies.

Staying knowledgeable in regards to the particular person updates for the 2023 tax season is important for each taxpayer. These adjustments, whether or not they pertain to tax charges, deductions, or credit, can considerably affect how your taxes will go. By preserving up-to-date with the newest tax laws and profiting from accessible sources and instruments, you may navigate the tax season with confidence, guaranteeing you benefit from your monetary alternatives whereas staying compliant with the regulation. To study extra about this scorching subject, please go to www.getcanopy.com/programs and click on right here to take the “2023 Tax Season-Particular person Updates” course and get your CPE/CE credit score.