{kind=link}

Notice: Every year we evaluate and enhance the methodology of the Index. For that purpose, prior editions will not be akin to the outcomes on this 2025 version. All information and methodological notes are accessible in our GitHub repository. Beneath is an abbreviated model of the 2025 Index. To entry the complete report, click on the obtain button above.

Introduction

The construction of a rustic’s tax code is a figuring out issue of its financial efficiency. A well-structured tax code is simple for taxpayers to adjust to and may promote financial improvement whereas elevating adequate income for a authorities’s priorities. In distinction, poorly structured tax programs may be pricey, distort financial decision-making, and hurt home economies.

Many nations have acknowledged this and have reformed their tax codes. Over the previous few many years, marginal tax charges on company and particular person revenue have declined considerably throughout the Organisation for Financial Co-operation and Improvement (OECD). Now, most OECD nations increase a big quantity of income from broad-based taxes corresponding to payroll taxes and value-added taxes (VAT).[1]

Not all latest modifications in tax coverage amongst OECD nations have improved the construction of tax programs; some have made a unfavorable affect. Although some nations, like Austria, have decreased their company revenue taxA company revenue tax (CIT) is levied by federal and state governments on enterprise earnings. Many firms will not be topic to the CIT as a result of they’re taxed as pass-through companies, with revenue reportable below the person revenue tax. charges by a number of proportion factors, others, like France, the Slovak Republic, and Slovenia, have elevated them. Company tax base enhancements have occurred in Germany, the UK, and the US, whereas the company tax base has been made much less aggressive within the Czech Republic and Slovenia. Canada and Finland are phasing out short-term enhancements to their company tax bases that the UK and the US have made everlasting and expanded.[2]

Lately, tax coverage has more and more drifted away from its conventional roles of elevating authorities income and inspiring funding into the toolbox of worldwide tax and commerce disputes, with import tariffs, digital service levies, and extraterritorial taxes deployed to exert financial stress. On this setting, policymakers ought to refocus on impartial, internationally aggressive tax insurance policies that increase income with minimal hurt to funding and financial progress. The number of approaches to taxation amongst OECD nations creates a necessity to judge these programs relative to one another. For that goal, we now have developed the Worldwide Tax Competitiveness Index—a relative comparability of OECD nations’ tax programs with respect to competitiveness and neutrality.

The Worldwide Tax Competitiveness Index

The Worldwide Tax Competitiveness Index (ITCI) seeks to measure the extent to which a rustic’s tax system adheres to 2 vital points of tax coverage: competitiveness and neutrality.

A aggressive tax code is one which retains marginal tax charges low. In at the moment’s globalized world, capital is very cell. Companies can select to put money into any variety of nations all through the world to search out the very best price of return. Which means that companies will search for nations with decrease tax charges on funding to maximise their after-tax price of return. If a rustic’s tax price is simply too excessive, it is going to drive funding elsewhere, resulting in slower financial progress. As well as, excessive marginal tax charges can impede home funding and result in tax avoidance.

In keeping with analysis from the OECD, company taxes are most dangerous for financial progress, with private revenue taxes and consumption taxes being much less dangerous. Taxes on immovable property have the smallest affect on progress.[3]

Individually, a impartial tax code is just one which seeks to boost essentially the most income with the fewest financial distortions. Which means that it doesn’t favor consumption over saving, as occurs with funding taxes and wealth taxes. It additionally means few or no focused tax breaks for particular actions carried out by companies or people.

As tax legal guidelines develop into extra complicated, in addition they develop into much less impartial. If, in idea, the identical taxes apply to all companies and people, however the guidelines are such that giant companies or rich people can change their conduct to realize a tax benefit, this undermines the neutrality of a tax system.

A tax code that’s aggressive and impartial promotes sustainable financial progress and funding whereas elevating adequate income for presidency priorities.

There are numerous elements unrelated to taxes which have an effect on a rustic’s financial efficiency. Nonetheless, taxes play an vital position within the well being of a rustic’s economic system.

To measure whether or not a rustic’s tax system is impartial and aggressive, the ITCI seems at greater than 40 tax coverage variables. These variables measure not solely the extent of tax charges, but additionally how taxes are structured. The Index seems at a rustic’s company taxes, particular person revenue taxes, consumption taxes, property taxes, and the therapy of earnings earned abroad. The ITCI provides a complete overview of how developed nations’ tax codes evaluate, explains why sure tax codes stand out nearly as good or dangerous fashions for reform, and offers vital perception into how to consider tax coverage.

On account of some information limitations, latest tax modifications in some nations is probably not mirrored on this yr’s model of the Worldwide Tax Competitiveness Index.

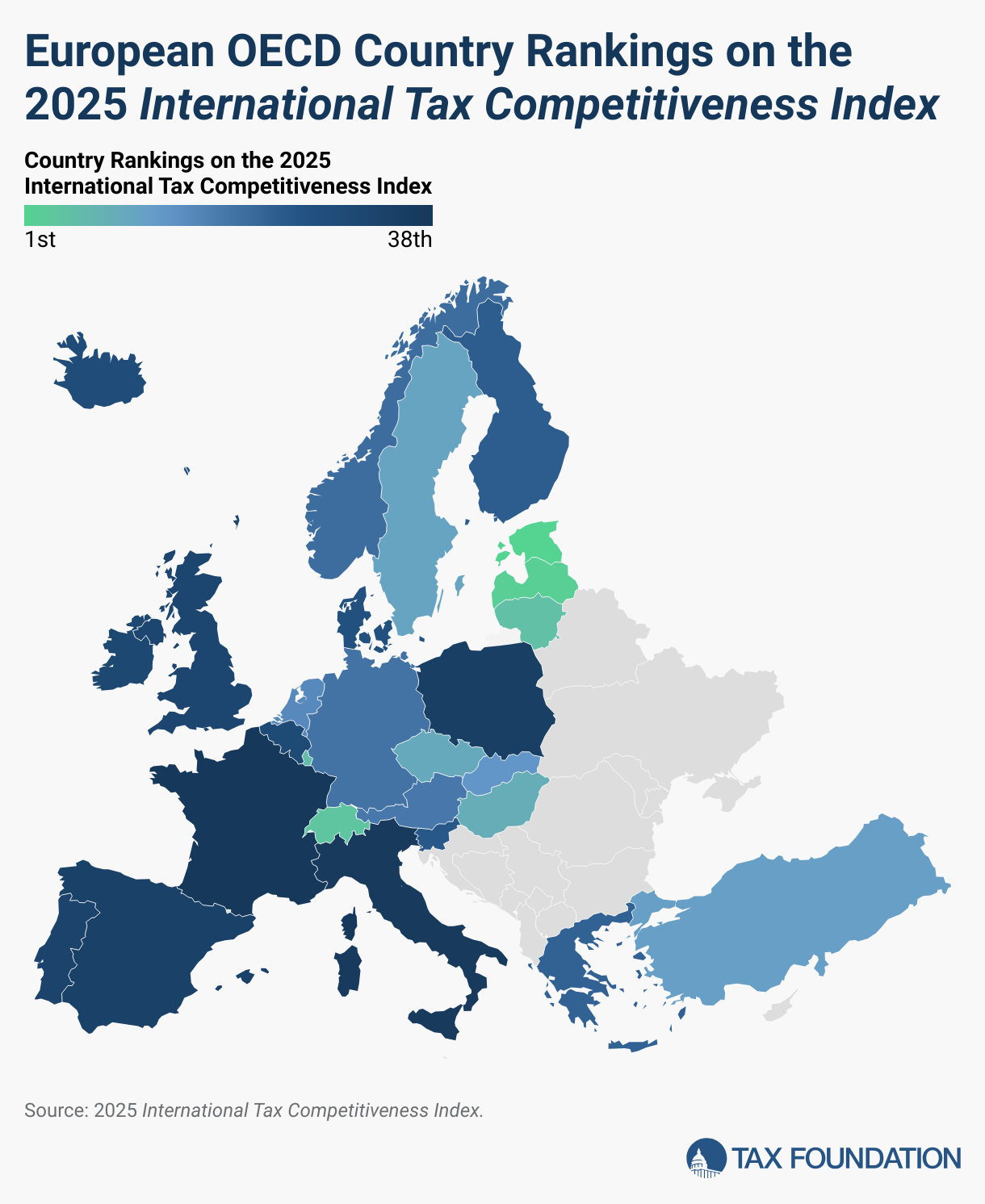

2025 Rankings

For the 12th yr in a row, Estonia has the most effective tax code within the OECD. Its prime rating is pushed by 4 optimistic options of its tax system. First, it has a 20 p.c tax price on company revenue that’s solely utilized to distributed earnings. Second, it has a flat 20 p.c tax on particular person revenue that doesn’t apply to non-public dividend revenue. Third, its property taxA property tax is primarily levied on immovable property like land and buildings, in addition to on tangible private property that’s movable, like autos and gear. Property taxes are the one largest supply of state and native income within the U.S. and assist fund faculties, roads, police, and different companies. applies solely to the worth of land, fairly than to the worth of actual property or capital. Lastly, it has a territorial tax systemTerritorial taxation is a system that excludes overseas earnings from a rustic’s home tax base. That is widespread all through the world and is the other of worldwide taxation, the place overseas earnings are included within the home tax base. that exempts one hundred pc of overseas earnings earned by home firms from home taxation, with few restrictions.

2025 Worldwide Tax Competitiveness Index Rankings

Whereas Estonia’s tax system is essentially the most aggressive within the OECD, the opposite prime nations’ tax programs obtain excessive scores because of excellence in a number of of the foremost tax classes. Latvia, which not too long ago adopted the Estonian system for company taxation, additionally has a comparatively environment friendly system for taxing labor revenue. New Zealand has a comparatively flat, low-rate particular person revenue taxA person revenue tax (or private revenue tax) is levied on the wages, salaries, investments, or different types of revenue a person or family earns. The U.S. imposes a progressive revenue tax the place charges improve with revenue. The Federal Revenue Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years outdated, particular person revenue taxes are the biggest supply that additionally largely exempts capital positive aspects (with a mixed prime price of 39 p.c), a broad-based VAT, and levies no taxes on inheritance, property transfers, property, or monetary transactions. Switzerland has a comparatively low company tax price (19.7 p.c), a low, broad-based consumption taxA consumption tax is often levied on the acquisition of products or companies and is paid straight or not directly by the patron within the type of retail gross sales taxes, excise taxes, tariffs, value-added taxes (VAT), or revenue taxes the place all financial savings are tax-deductible., and a person revenue tax that partially exempts capital positive aspects from taxation. Luxembourg levies its broad-based VAT on 82 p.c of ultimate consumption, exempts long-term capital positive aspects with out substantial possession from taxation, and has a aggressive cross-border regime with out withholdingWithholding is the revenue an employer takes out of an worker’s paycheck and remits to the federal, state, and/or native authorities. It’s calculated primarily based on the quantity of revenue earned, the taxpayer’s submitting standing, the variety of allowances claimed, and any further quantity the worker requests. taxes on curiosity or royalties. Lithuania has a low company tax price of 17 p.c, permits companies to deduct a excessive share of their capital funding prices, and levies a comparatively flat and low-rate particular person revenue tax.

France has the least aggressive tax system within the OECD. It has the very best prime company tax price within the OECD, at 36.13 p.c, together with a number of surtaxes and distortive manufacturing taxes. It additionally applies a number of distortionary property taxes with separate levies on estates, financial institution property, and monetary transactions, along with a wealth taxA wealth tax is imposed on a person’s web wealth, or the market worth of their whole owned property minus liabilities. A wealth tax may be narrowly or extensively outlined, and relying on the definition of wealth, the bottom for a wealth tax can range. on actual property. Its VAT covers about 50 p.c of ultimate consumption, and it has one of many highest VAT registration thresholds.

Italy has the second-least aggressive tax system within the OECD. It has a number of distortionary property taxes with separate levies on actual property transfers, estates, and monetary transactions, in addition to a wealth tax on chosen property. Italy’s comparatively excessive VAT price of twenty-two p.c applies to the sixth-narrowest consumption tax base within the OECD.

International locations that rank poorly on the ITCI usually levy comparatively excessive marginal tax charges on company revenue or have a number of layers of tax guidelines that contribute to complexity. The 5 nations on the backside of the rankings all have higher-than-average mixed company tax charges. Eire ranks poorly on the ITCI regardless of its low company tax price. This is because of excessive private revenue and dividend taxes and a comparatively slender VAT base. The 5 lowest-ranking nations have unusually slender VAT bases, overlaying solely between 38 and 50 p.c of ultimate consumption. Additionally they are inclined to levy unusually many distortive taxes on slender bases, with all backside 5 nations making use of digital companies taxes, monetary transaction taxes, and inheritance taxes. 4 out of 5 of the lowest-ranking nations additionally levy both some kind of wealth tax or capital duties (or each).

Notable Adjustments from Final Yr

Canada

In 2024, Canada began to part out full expensingFull expensing permits companies to right away deduct the complete value of sure investments in new or improved expertise, gear, or buildings. It alleviates a bias within the tax code and incentivizes firms to speculate extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs. for equipment and the accelerated funding incentive for buildings. Canada additionally abolished its digital companies tax in 2025 and canceled the deliberate improve within the capital positive aspects inclusion price. Canada’s rank rose from 14th to 13th.

Czech Republic

The Czech Republic elevated its company tax price and began taxing long-term capital positive aspects at a prime price of 23 p.c for high-income people. The Czech Republic’s rank fell from 9th to 10th.

France

France added a brief surtax on company revenue for firms with excessive revenues, lifting its prime marginal company price from 25.8 to 36.1 p.c, the very best price within the OECD. France’s rank fell from 36th to 38th.

Germany

Germany reinstated its accelerated depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, corresponding to equipment or a manufacturing unit, to find out the multiyear interval over which the price of that asset may be deducted from taxable revenue. As a substitute of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, decreasing their worth and disco schedule for equipment and gear at the next price in summer season 2025 and plans to cut back its company tax price by 5 proportion factors over the subsequent 5 years. Germany’s rank improved from 21st to twentyth.

Eire

Eire turned one of many final OECD nations to introduce a participation exemption for dividends obtained from overseas, transferring to a extra territorial system. Eire’s rank improved from 33rd to 31st.

Portugal

Portugal lowered its tax price on long-term capital positive aspects from 28 to 19.6 p.c and decreased its prime company tax price from 31.5 to 30.5 p.c. In 2025, Portugal additionally made its notional curiosity deduction extra beneficiant. Portugal’s rank rose from 35th to 33rd.

Slovak Republic

In 2025, the Slovak Republic elevated its company price from 21 to 24 p.c, elevated its VAT registration threshold, and launched a monetary transaction tax. The Slovak Republic’s rank fell from 10th to 14th.

United States

The US reinstated full expensing for crops and gear and prolonged the coverage to chose industrial buildings and buildings. Whereas the relative attractiveness of US cross-border guidelines elevated as many different nations began to implement revenue inclusion guidelines and home top-up taxes inside the international minimal tax course of, the US can be set to tighten its cross-border guidelines in 2026. The US rank improved from 16th to fifteenth.

Desk 2. Adjustments from Final Yr

Methodological Adjustments

Every year, we evaluate the Index’s information and methodology to enhance the way it measures each competitiveness and neutrality. This yr, we now have modified the best way the Index treats company taxes and particular person taxes.

We’ve utilized every change to prior years to permit constant comparability throughout years. Knowledge for all years utilizing the present methodology is accessible within the GitHub repository for the Index,[5] and an outline of how the Index is calculated is offered within the Appendix of this report. Prior editions of the Index, nonetheless, will not be akin to the outcomes on this 2024 version because of these methodological modifications.

Company Tax

The online current worth of capital allowances for equipment, industrial buildings, and intangibles now displays inflation-indexing for capital allowances as practiced in Israel and Mexico.

Consumption Taxes

Some nations have revised the calculation of nationwide accounts information, altering the estimated share of ultimate consumption captured by their VAT.

Property Taxes

The true property tax burden as a share of a capital inventory now consists of property tax income collected from taxpayers aside from households.

Company Revenue Tax

The company revenue tax is a direct taxA direct tax is levied on people and organizations and isn’t anticipated to be handed on to a different payer (in contrast to oblique taxes corresponding to gross sales and excise taxes), although financial incidence can nonetheless fall upon others. Typically with a direct tax, corresponding to the person revenue tax, tax charges improve because the taxpayer’s potential to pay, or monetary sources, will increase, leading to what is named a p on the earnings of a company. All OECD nations levy a tax on company earnings, however the tax charges and bases range considerably throughout nations. Company revenue taxes scale back the after-tax price of return on company funding. This will increase the price of capital, which ends up in decrease ranges of funding and financial output. Moreover, the company tax can result in decrease wages for staff, decrease returns for traders, and better costs for shoppers.

Though the company revenue tax has a comparatively important affect on a rustic’s economic system, it raises a comparatively low quantity of tax income for many governments—the OECD common was 11.9 p.c of whole revenues in 2023.[6]

The ITCI breaks the company revenue tax class into three subcategories. Desk 3 shows every nation’s Company Revenue Tax class rank and rating together with the ranks and scores of the subcategories, particularly, the company price, value restorationPrice restoration refers to how the tax system permits companies to recuperate the price of investments by means of depreciation or amortization. Depreciation and amortization deductions have an effect on taxable revenue, efficient tax charges, and funding selections., and incentives and complexity.

Mixed Prime Marginal Company Revenue Tax Fee

The highest marginal company revenue tax price measures the speed at which every further greenback of taxable revenue is taxed. Excessive marginal company tax charges are inclined to discourage capital formation and thus sluggish financial progress.[7] International locations with greater prime marginal company revenue tax charges than the OECD common obtain decrease scores than these with decrease, extra aggressive charges.

France levies the very best prime mixed company revenue tax price, at 36.1 p.c, adopted by Colombia (35 p.c) and Portugal (30.5 p.c). The bottom prime marginal company revenue tax price within the OECD is present in Hungary, at 9 p.c, adopted by Eire (12.5 p.c) and Lithuania (15 p.c). The OECD common mixed company revenue tax price is 24.2 p.c for 2025.[8]

Desk 3. Company Taxes

Price Restoration

Enterprise earnings are typically decided as income (what a enterprise makes in gross sales) minus prices (the price of doing enterprise). The company revenue tax is meant to be a tax on these earnings. Thus, it can be crucial {that a} tax code correctly defines what constitutes taxable revenue. If a tax code doesn’t permit companies to account for all the prices of doing enterprise, it is going to inflate a enterprise’s taxable revenue and thus its tax invoice. This will increase the price of capital, resulting in slower funding and financial progress.

Loss Offset Guidelines: Carryforwards and Carrybacks

Loss carryover provisions permit companies to both deduct present yr losses towards future earnings (carryforwards) or deduct present yr losses towards previous earnings (carrybacks). Many firms have funding initiatives with totally different threat profiles and function in industries that fluctuate significantly with the enterprise cycle. Carryover provisions assist companies “easy” their threat and revenue, making the tax code extra impartial throughout investments and over time.[9]

Ideally, a tax code permits companies to hold ahead their losses for a vast variety of years, guaranteeing {that a} enterprise is taxed on its common profitability over time. Whereas some nations do permit for indefinite loss carryovers, others have time—and deductibility—limits.

In 22 of the 38 OECD nations, firms can carry ahead losses indefinitely in 2025, although 13 of those restrict the quantity of taxable revenue that may be offset by losses from earlier years.[10] Of the 16 nations with deadlines, the typical loss carryforward interval is eight years. Hungary, Poland, and Slovakia have essentially the most restrictive loss carryover provisions within the OECD: carrybacks will not be allowed, and carryforwards will not be solely restricted to 5 years but additionally capped at 50 p.c of taxable revenue (coded as 2.5 years).[11] The ITCI ranks nations that permit losses to be carried ahead indefinitely with out limits higher than nations that impose time or deductibility restrictions on carryforwards.

International locations are usually considerably extra restrictive with loss carryback provisions than with carryforward provisions. In 2025, solely the Estonian and Latvian programs permit, by design, limitless carrybacks of losses.[12] Of the 9 nations that permit time-limited carrybacks, the typical interval is 1.3 years.[13] The ITCI penalizes the 27 nations that don’t permit any loss carrybacks.

Capital Price Restoration: Machines, Buildings, and Intangibles

Companies decide their earnings by subtracting prices—corresponding to wages and uncooked supplies—from income. Nevertheless, in most jurisdictions, capital investments—corresponding to in buildings, equipment, and intangibles—will not be handled like different common prices that may be subtracted from income within the yr the cash is spent. As a substitute, companies are required to put in writing off these prices over a number of years and even many years, relying on the kind of asset.

Depreciation schedules specify the quantities companies are legally allowed to put in writing off, in addition to the time interval over which property must be written off. For example, a authorities could require a enterprise to deduct an equal proportion of the price of a machine over a seven-year interval. By the top of the depreciation interval, the enterprise would have deducted the full preliminary greenback value of the asset. Nevertheless, because of the time worth of cash (a traditional actual return plus inflation), write-offs in later years will not be as beneficial in actual phrases as write-offs in earlier years. In consequence, companies successfully lose the power to deduct the complete current worth of their funding value. This tax therapy of capital bills understates true enterprise prices and overstates taxable revenue in current worth phrases.[14]

The ITCI measures a rustic’s capital allowances for 3 asset varieties, particularly, equipment, industrial buildings, and intangibles.[15] Capital allowances are expressed as a p.c of the current worth value that firms can write off over the lifetime of an asset. A one hundred pc capital allowanceA capital allowance is the quantity of capital funding prices, or cash directed in direction of an organization’s long-term progress, a enterprise can deduct every year from its income by way of depreciation. These are additionally generally known as depreciation allowances. represents a enterprise’ potential to deduct the complete value of an funding over its life in actual phrases. International locations that present quicker write-offs for capital investments obtain higher scores within the ITCI.

On common, throughout the OECD, in actual phrases, companies can write off 85.7 p.c of funding prices in equipment, 49.9 p.c of the price of industrial buildings, and 76.7 p.c of the price of intangibles.

In 2023, the UK made full expensing for equipment and gear a everlasting function of its tax code. In 2025, the US reinstated full expensing for equipment and gear, additionally on a everlasting foundation. Moreover, the US quickly offers one hundred pc expensing for qualifying buildings (overlaying near one hundred pc of all industrial buildings), with the start of building occurring after Jan. 19, 2025, and earlier than Jan. 1, 2029, and positioned in service earlier than Jan. 1, 2031. This represents roughly 10-15 p.c of all buildings and buildings within the US.

Germany partially reinstated accelerated depreciation in 2024 and once more in 2025, at the next depreciation price. The renewal was paired with an elevated depreciation price for dwellings till 2029. Moreover, the federal government has not too long ago elevated and prolonged the accelerated depreciation schedules for equipment into 2027.

In distinction, Canada is frequently phasing out its insurance policies of full expensing whereas Finland’s accelerated depreciation coverage is about to run out after 2025. Moreover, the Czech Republic ended its coverage of extraordinary depreciation for equipment. New Zealand abolished its capital allowances for long-life business buildings completely in 2024 earlier than introducing a 20 p.c speedy allowance for any new bodily property, together with industrial buildings.

Estonia and Latvia are coded as permitting one hundred pc of the current worth of a capital funding to be written off, as their company tax solely applies to distributed earnings and is thus decided by money move.[16]

Inventories

Much like capital investments, the prices of inventories will not be written off within the yr of buy. As a substitute, the prices of inventories are deducted at sale. In consequence, governments have to outline the full value of inventories offered. There are typically three strategies used to calculate inventories: Final In, First Out (LIFO); Common Price; and First In, First Out (FIFO).

The tactic by which a rustic permits companies to account for inventories can considerably affect a enterprise’s taxable revenue. When costs are rising, as is normally the case, LIFO is the popular technique as a result of it permits stock prices to be nearer to true prices on the time of sale. This ends in the bottom taxable revenue for companies. In distinction, FIFO is the least most well-liked technique as a result of it ends in the very best taxable revenue. The Common Price technique is between FIFO and LIFO.[17]

International locations that permit companies to decide on the LIFO technique obtain the most effective scores, those who permit the Common Price technique obtain a mean rating, and nations that solely permit the FIFO technique obtain the worst scores. Fourteen OECD nations permit firms to make use of the LIFO technique of accounting, 19 nations use the Common Price technique of accounting, and 5 nations restrict firms to the FIFO technique of accounting.[18]

Allowance for Company Fairness

Companies can finance their operations by means of debt or fairness. Nevertheless, the return on these two sorts of finance is taxed otherwise. Customary company revenue tax programs permit tax deductions of curiosity funds however not of fairness prices, successfully offering a tax benefit to debt over fairness finance—the so-called “debt bias.” This debt bias may be thought-about an actual threat to financial stability.[19]

There are two broad methods to handle this debt bias, particularly, limiting the tax deductibility of curiosity and offering a deduction for fairness prices. Limiting the tax deductibility of curiosity bills creates new distortions, as curiosity revenue normally continues to be absolutely taxed. An allowance for company fairness—generally known as a notional curiosity deduction—retains the deduction for curiosity bills however provides an identical deduction for the traditional return on fairness, neutralizing the debt bias whereas eliminating tax distortions to funding.

Three OECD nations—Poland, Portugal, and Turkey—have an allowance for company fairness.[20] Belgium and Italy phased out their allowances for company fairness in 2024. The allowance price is often primarily based on the company or authorities bond price and, in some circumstances, is adjusted by a threat premium.[21]

International locations which have carried out an allowance for company fairness obtain a greater rating within the Index.

Tax Incentives and Complexity

Good tax coverage treats financial selections neutrally, neither encouraging nor discouraging one exercise over one other. A tax incentive is a tax credit score, deduction, or preferential tax price that completely applies to a selected kind of financial exercise and may thus distort financial selections.

For example, when an trade receives a tax credit score for producing a selected product, it could select to overinvest in that exercise, though it would in any other case not be worthwhile. Moreover, the price of particular provisions is commonly offset by shifting the burden onto different taxpayers within the type of greater taxes.

As well as, the opportunity of receiving incentives invitations efforts to safe these tax preferences,[22] corresponding to lobbying, which creates further deadweight financial loss as corporations focus sources on influencing the tax code in lieu of manufacturing merchandise. For example, the deadweight losses in the US attributed to tax compliance and lobbying have been estimated to be between $215 billion and $987 billion in 2012. These expenditures for lobbying, together with compliance, have been proven to cut back financial progress by crowding out potential financial exercise.[23]

The ITCI considers whether or not nations present incentives corresponding to patent fieldA patent field—additionally known as mental property (IP) regime—taxes enterprise revenue earned from IP at a price beneath the statutory company revenue tax price, aiming to encourage native analysis and improvement. Many patent packing containers all over the world have undergone substantial reforms because of revenue shifting considerations. provisions and analysis and improvement (R&D) tax subsidies. International locations that present such incentives are scored worse than these that don’t.

Patent Containers

On account of an more and more globalized and cell economic system, nations have searched for methods to forestall firms from reincorporating or shifting operations or earnings elsewhere. One response to the rise in capital mobility has been the creation of patent packing containers.

Patent packing containers—additionally known as mental property, or IP, regimes—present tax charges on revenue derived from IP which can be beneath statutory company tax charges. Eligible sorts of IP are mostly patents and software program copyrights. Patent packing containers are an income-based fairly than an expenditure-based tax incentive, limiting its advantages to profitable R&D initiatives which have produced IP rights fairly than lowering the ex ante dangers of R&D by means of value reductions.

Mental property is extraordinarily cell. Therefore, a rustic can use the decrease tax price of a patent field to entice firms to carry their mental property inside its borders. Analysis means that patent packing containers are more likely to entice new revenue derived from patents, implying that companies scale back their company tax legal responsibility by shifting IP-related revenue. Tax revenues, nonetheless, are more likely to decline, because the unfavorable income results of the decrease statutory price on patent revenue may be solely partially offset by revenues from newly attracted patent revenue.[24]

Lately, patent field guidelines have develop into extra stringent in some nations because the OECD necessities for countering dangerous tax practices have been adopted. International locations that comply with the OECD requirements now require firms to have substantial R&D exercise inside their borders to profit from tax preferences related to their mental property.[25]

As a substitute of offering patent packing containers for mental property, nations ought to acknowledge that every one capital is cell to a point and decrease their company tax charges throughout the board. This might encourage funding of every kind, fairly than merely incentivizing firms to find their patents in a selected nation.

Seventeen OECD nations—Australia, Belgium, France, Hungary, Eire, Israel, Korea, Lithuania, Luxembourg, the Netherlands, Poland, Portugal, Slovakia, Spain, Switzerland, Turkey, and the UK—have patent field laws, with charges and exemptions various amongst nations.[26] The USA has a decreased tax price for earnings from exports associated to mental property held within the US, which is handled as a patent field within the Index. International locations with patent field regimes obtain a decrease rating.

Analysis and Improvement

Within the absence of full expensing, expenditure-based R&D tax incentives (partially) offset the tax prices of enterprise funding. Sadly, R&D tax incentives are hardly ever impartial—they normally outline very particular actions that qualify—and are sometimes complicated of their implementation.

As with different incentives, R&D incentives distort funding selections and may result in an inefficient allocation of sources.[27] Moreover, the need to safe R&D incentives encourages the relabeling of bills as R&D and lobbying actions that devour sources and detract from funding and manufacturing. In Italy, as an illustration, corporations can have interaction in a negotiation course of for incentives, corresponding to simple time period loans and tax credit.[28]

International locations might higher use the income spent on particular tax incentives to offer a decrease enterprise tax price throughout the board, enhance the tax therapy of capital funding, or lengthen loss-carryover provisions.[29]

The implied tax subsidy price on R&D expenditures, developed by the OECD, measures the extent of expenditure-based R&D tax reduction throughout nations. Implied tax subsidy charges are measured because the distinction between one unit of funding in R&D and the pretax revenue required to interrupt even on that funding unit, assuming a consultant agency. In different phrases, it measures the extent of the preferential therapy of R&D in a given tax system. The extra beneficiant the tax provisions for R&D, the upper the implied tax subsidy charges for R&D. An implied subsidy price of zero means R&D doesn’t obtain preferential tax therapy.

OECD nations grant implied tax subsidies of R&D expenditures at a mean price of 15.4 p.c. Iceland has the very best implied tax subsidy price, at 36 p.c. Portugal and France present the second and third most beneficiant reduction, with implied tax subsidy charges of 35 and 34 p.c, respectively.

Of the nations that grant notable reduction, Denmark (1 p.c), the US (3 p.c), Mexico (6 p.c), and Turkey (6 p.c) are the least beneficiant. The implied tax subsidy charges of Costa Rica, Estonia, Israel, Latvia, Luxembourg, and Switzerland don’t present any important expenditure-based R&D tax reduction.[30]

International locations that present extra beneficiant expenditure-based R&D tax incentives obtain a decrease rating on the ITCI.

Digital Companies Taxes

Over the previous few years, a number of OECD nations have carried out so-called digital companies taxes (DSTs). DSTs are taxes on chosen gross income streams of huge digital companies. Their tax base usually consists of revenues both derived from a selected set of digital items or companies (for instance, focused internet marketing) or primarily based on the variety of digital customers inside a rustic. Comparatively excessive home and international income thresholds restrict the tax to giant multinationals.

DSTs successfully ring-fence the digital economic system by limiting the tax to sure income streams of huge digital companies, creating distortions primarily based on agency measurement and enterprise mannequin. As well as, as a result of DSTs are levied on revenues fairly than earnings, they don’t take note of profitability, and thus disproportionally have an effect on corporations with decrease revenue margins.

As of 2025, 12 OECD nations have carried out a DST: Austria, Colombia, Denmark, France, Hungary, Italy, Poland, Portugal, Spain, Switzerland, Turkey, and the UK.[31]

International locations which have carried out a DST obtain a decrease rating on the ITCI.

Complexity

The ITCI quantifies company tax code complexity by measuring the variety of separate taxes (and charges) that apply to enterprise revenue, the existence of surtax charges on enterprise revenue, and the quantity of income nations accumulate from enterprise earnings taxes aside from the company revenue tax. These burdens are measured by tallying up the separate charges that apply to enterprise revenue, figuring out relevant surtaxes, and counting on OECD income information to measure the share of income from taxes on enterprise revenue aside from the company revenue tax. In 2024, many OECD nations have adopted QDMTTs inside the international minimal tax course of.[32]

International locations which have a number of charges that apply to company revenue, surtaxes, and accumulate income on revenue and earnings exterior of regular revenue taxes obtain worse scores on the ITCI.

The nation with the very best variety of separate tax charges is Portugal with six brackets. Costa Rica and Korea comply with with 5 and 4, respectively. There are six OECD nations that shouldn’t have a number of tax charges or bases for his or her company revenue tax.[33]

Company surtaxes are comparatively unusual in OECD nations, with simply 4 making use of a surtax to enterprise revenue. France, Germany, Japan, and Luxembourg all apply a surtax to all or a part of their company revenue tax base.[34]

The OECD information on tax revenues has a class for revenues which can be unallocable to regular private or enterprise revenue taxes.[35] The information present that Italy (1.76 p.c), Iceland (1.58 p.c), New Zealand (1.44 p.c), Costa Rica (1.21 p.c), Switzerland (1.08 p.c), and Israel (1.06 p.c) accumulate non-negligible shares of income from revenue (together with private revenue) from taxes aside from company or private revenue taxes. Seventeen OECD nations accumulate no income in that class.

Particular person Taxes

Particular person taxes are some of the prevalent technique of elevating income to fund authorities spending. Particular person revenue taxes are levied on a person’s or family’s revenue (wages and, usually, capital positive aspects and dividends) to fund common authorities operations. These taxes are usually progressive, that means that the speed at which a person’s revenue is taxed will increase as the person earns extra revenue.

As well as, nations have payroll taxes—additionally known as social safety contributions or social insurance coverage taxes. These usually flat-rate taxes are levied on wage revenue along with a rustic’s common particular person revenue tax. Nevertheless, income from these taxes is often allotted particularly towards social insurance coverage applications corresponding to unemployment insurance coverage, authorities pension applications, and medical insurance.

Particular person taxes can get pleasure from being among the extra clear taxes. Taxpayers are made conscious of their whole quantity of taxes paid in some unspecified time in the future within the course of—in contrast to, for instance, consumption taxes, that are collected and remitted by a enterprise, and a person is probably not conscious of their whole consumption tax burden.

Most nations tax people on their revenue utilizing two approaches. First, nations tax earnings from work with odd revenue taxes and payroll taxes. The construction of those taxes can affect people’ selections to work, take a further part-time job, or whether or not a second earner within the family will work. Second, people are taxed on their financial savings by means of taxes on capital positive aspects and dividends. Generally, these taxes are a second layer of tax on company earnings and may affect selections on how a lot to save lots of and make investments. Excessive taxes on capital positive aspects and dividends can scale back the mixture financial savings and funding in a rustic.

A rustic’s rating for its particular person revenue tax is decided by three subcategories: the speed and progressivity of wage taxation, revenue tax complexity, and the extent to which the revenue tax double taxes company revenue. Desk 4 reveals the ranks and scores for your complete Particular person Taxes class in addition to the rank and rating for every subcategory.

Taxes on Odd Revenue

Particular person revenue taxes are levied on the revenue of people or households. Many nations, corresponding to the US, depend on particular person revenue taxes as a big supply of tax income.[36] They’re used to boost income for each common authorities operations and for particular applications, corresponding to social insurance coverage and government-provided medical insurance.

A rustic’s taxes on odd revenue are measured in line with three variables: the highest price at which odd revenue is taxed, the highest revenue tax threshold, and the financial effectivity of labor taxation.

Desk 4. Particular person Taxes

Prime Statutory Private Revenue Tax Fee

Most nations’ revenue tax programs have a progressive taxA progressive tax is one the place the typical tax burden will increase with revenue. Excessive-income households pay a disproportionate share of the tax burden, whereas low- and middle-income taxpayers shoulder a comparatively small tax burden. construction. Which means that, as people earn extra revenue, they transfer into tax bracketsA tax bracket is the vary of incomes taxed at given charges, which usually differ relying on submitting standing. In a progressive particular person or company revenue tax system, charges rise as revenue will increase. There are seven federal particular person revenue tax brackets; the federal company revenue tax system is flat. with greater tax charges. The highest statutory private revenue tax price is the highest tax price on all revenue over a sure degree. For instance, the US has seven tax brackets, with the seventh (prime) bracket taxing every further greenback of revenue over $626,350 ($741,600 for married submitting collectively) at a price of 37 p.c in 2025.[37] As well as, US taxpayers additionally pay state and native revenue taxes in addition to Medicare contributions, which sum to a mixed prime private revenue tax price of 45.8 p.c.[38]

People contemplate the marginal tax price when deciding whether or not to work a further hour. In lots of circumstances, the choice can be about taking a second, part-time job or whether or not households with two adults may have one or two earners. If a person faces a marginal tax price of 30 p.c on their present earnings, taking further work or one other shift would imply that solely 70 p.c of these earnings may very well be introduced house.

Excessive prime private tax charges make further work costlier, which lowers the relative value of not working. This makes it extra possible that a person will select leisure over work, sustaining present hours fairly than transferring to full-time work or taking a further shift. Excessive tax charges improve the price of labor, which might lower hours labored, and, in flip, can scale back the quantity of manufacturing within the economic system.

International locations with excessive prime statutory private revenue tax charges obtain a worse rating on the ITCI than nations with decrease prime charges. Slovenia has the very best all-in prime statutory private revenue tax price (together with worker social contributions) at 67.5 p.c. Estonia has the bottom, at 21.6 p.c.[39]

Revenue Stage at Which Prime Statutory Private Revenue Tax Fee Applies

The extent at which the highest statutory private revenue tax price first applies can be vital. If a rustic has a prime price of 20 p.c, however nearly everybody pays that price as a result of it applies to any revenue over $10,000, that nation basically has a flat revenue tax. In distinction, a tax system that has a prime price that applies to all revenue over $1 million requires a a lot greater prime tax price to boost the identical quantity of income, as a result of it targets a small variety of those who earn a excessive degree of revenue.

International locations with prime statutory private revenue tax charges that apply at decrease ranges rating higher on the ITCI. The ITCI bases its measure on the revenue degree at which the highest price first applies as in comparison with the nation’s common revenue. In keeping with this measure, Colombia applies its prime tax price on the highest degree of revenue (the highest private revenue tax price applies at 58.9 occasions the typical Colombian revenue), whereas Hungary applies its prime price on the primary greenback, with a flat private revenue tax of 15 p.c.[40]

The Financial Price of Labor Taxation

All taxes create some financial losses; nonetheless, tax programs needs to be designed to reduce these losses whereas supporting income wants.

One technique to study the effectivity of labor taxation in a rustic is to manage for the extent of labor taxation utilizing the ratio of the marginal tax wedge to the typical tax wedge.[41] The marginal tax wedge influences the selection to earn one other greenback of revenue, whereas the typical tax wedge measures the tax burden on the present revenue degree.[42] The next ratio signifies that as one earns extra revenue, the affect of the tax system on these selections and the associated financial losses grows. A decrease ratio signifies that a person can resolve to work extra with out the tax system altering their selections.

For instance, one particular person faces a mean tax wedge on their earnings of 20 p.c and their marginal tax wedge can be 20 p.c. That particular person might work extra hours with out the relative tax burden rising. The ratio of that employee’s marginal tax wedge to their common tax wedge is 1. One other particular person who faces a mean tax wedge of 20 p.c on their earnings and a marginal tax wedge of 30 p.c, nonetheless, would have their determination of whether or not to work extra hours influenced by the tax system. The ratio of that employee’s marginal tax wedge to their common tax wedge is 1.5.

The ITCI provides nations with excessive ratios a worse rating because of the bigger affect that these programs have on staff’ selections.

Hungary has the bottom ratio of 1, that means the subsequent greenback earned faces the identical tax burden as present earnings.[43] It’s because Hungary has a flat revenue tax, so the marginal and common tax wedge are the identical. In distinction, Israel’s ratio is 1.7. The typical throughout OECD nations is 1.27.[44]

Complexity

Complexity is measured by the speed of any surtax on private revenue and the quantity of income raised by means of social safety contributions aside from these collected by means of employer or worker payroll taxes. These measures point out non-standard approaches to the taxation of labor revenue and, within the case of surtaxes, a much less clear private revenue tax system. The Index penalizes nations with surtaxes and important revenues from non-standard employer and worker payroll taxes.

4 OECD nations levy a surtax on private revenue: Germany, Japan, Korea, and Luxembourg. Germany levies a 5.5 p.c solidarity surcharge on all capital positive aspects and dividend revenue tax in addition to revenue tax paid in extra of EUR 18,130, equal to labor revenue above EUR 96,409 for single filers, rising its prime marginal revenue tax price from 45 p.c to 47.475 p.c. Japan applies a 2.1 p.c surtax on all nationwide (however not native) revenue tax legal responsibility.

4 OECD nations increase some significant share of income by means of non-standard social safety contributions. In Costa Rica, these revenues make up 31.1 p.c of whole tax revenues. Mexico (14.1 p.c), Iceland (8.6 p.c), and Colombia (8.3 p.c) make up the others on this group.

Capital Positive aspects and Dividends Taxes

Along with wage revenue, many nations’ particular person revenue tax programs tax funding revenue by levying taxes on capital positive aspects and dividends.

A capital acquire happens when a person purchases an asset (normally company inventory) in a single interval and sells it in one other for a revenue. A dividend is a cost made to a person from after-tax company earnings.

Capital positive aspects taxes and private dividend taxes are a type of double taxationDouble taxation is when taxes are paid twice on the identical greenback of revenue, no matter whether or not that’s company or particular person revenue. of company earnings that contribute to the tax burden on capital. When a company makes a revenue, it pays company revenue tax. It may well then typically do one in all two issues. The company can retain the after-tax earnings, which increase the worth of the enterprise and thus its inventory worth. Stockholders then promote the inventory and understand a capital acquire, which requires them to pay tax on that revenue. Alternatively, the company can distribute the after-tax earnings to shareholders within the type of dividends. Stockholders who obtain dividends then pay dividends tax on that revenue.

An organization that makes a taxable revenue of $1 million and pays 20 p.c in company revenue taxes would have $800,000 left to both reinvest within the firm, which might increase the worth of the inventory, or pay a dividend. A shareholder would possibly face a further 20 p.c tax on the positive aspects from promoting the shares or on a dividend from the corporate. Successfully, the system taxes the enterprise earnings at 36 p.c. A person hoping that an funding offers a ten p.c actual price of return would possibly see solely a 6.4 p.c after-tax price of return.

Some tax programs account for this potential double taxation both by means of credit towards capital positive aspects taxes for company taxes paid or different deductions. Such a tax system offers built-in taxation of company earnings, or “company integration.”[45]

Other than double taxation, taxes on dividends and capital positive aspects can change the incentives for companies after they want to finance new initiatives. If a enterprise can both fund a brand new mission by promoting new shares of inventory or by reinvesting its earnings, the taxes on traders can affect which strategy ends in greater after-tax returns. Norway makes use of a price of return allowance on capital positive aspects taxes to neutralize the choice between reinvesting earnings or promoting new shares.[46]

Typically, greater dividends and capital positive aspects taxes create a bias towards saving and funding, scale back capital formation, and sluggish financial progress.[47]

Within the ITCI, a rustic receives a greater rating for decrease capital positive aspects and dividend taxes.

Capital Positive aspects TaxA capital positive aspects tax is levied on the revenue constructed from promoting an asset and is commonly along with company revenue taxes, often leading to double taxation. These taxes create a bias towards saving, resulting in a decrease degree of nationwide revenue by encouraging current consumption over funding. Charges

International locations typically tax capital positive aspects at a decrease price than odd revenue, offered that particular necessities are met. For instance, the US taxes capital positive aspects at a decreased price if the taxpayer holds the asset for at the least one yr earlier than promoting it (so-called long-term capital positive aspects).[48] The ITCI provides nations with greater capital positive aspects tax charges a worse rating than these with decrease charges.

Some nations use further provisions to assist mitigate the double taxation of revenue because of the capital positive aspects tax. For example, the UK offers an annual exemption of GBP 3,000 (USD 3,831),[49] and Canada excludes half of all capital positive aspects revenue from taxation.[50]

Denmark has the very best capital positive aspects tax price within the OECD, at 42 p.c. Belgium, Greece, Korea, Luxembourg, New Zealand, Slovakia, Slovenia, Switzerland, and Turkey don’t tax long-term capital positive aspects from the sale of shares.[51]

Dividend Tax Charges

Dividend taxes can adversely affect capital formation in a rustic. Excessive dividend tax charges improve the price of capital, which deters funding and slows financial progress.

International locations’ charges are expressed as the highest marginal private dividend tax price after any imputation or credit score system.

International locations with decrease total dividend tax charges rating higher on the ITCI because of the dividend tax price’s impact on the price of funding (i.e., the price of capital) and the extra impartial therapy between saving and consumption. Eire has the very best dividend tax price within the OECD, at 51 p.c. Estonia and Latvia have dividend tax charges of 0 p.c because of their cash-flow company tax system, and Greece’s prime dividend tax price is 5 p.c. The OECD common is 24.7 p.c.[52]

Consumption Taxes

Consumption taxes are levied on people’ purchases of products and companies. Within the OECD and a lot of the world, the value-added tax (VAT) is the commonest common consumption tax.[53] Most common consumption taxes both don’t tax intermediate enterprise inputs or permit a credit score for taxes already paid on them, making them some of the economically environment friendly technique of elevating tax income.

Nevertheless, many nations outline their tax base inefficiently. Most nations levy decreased tax charges and exempt sure items and companies from VAT, requiring them to levy greater normal tax charges to boost adequate income. Some nations fail to correctly exempt enterprise inputs. For instance, states in the US usually levy gross sales taxes on equipment and gear.[54]

A rustic’s consumption tax rating is damaged down into two subcategories: the tax price and the tax base. Desk 5 shows the ranks and scores for the Consumption Taxes class.

Consumption Tax Fee

If levied on the similar price and correctly structured, a VAT and a retail gross sales tax will every increase roughly the identical quantity of income. Ideally, both a VAT or a gross sales tax needs to be levied at the usual price on all remaining consumption (though they’re carried out in barely alternative ways). With a sufficiently broad consumption tax base, the tax price may be comparatively low. A VAT or retail gross sales tax with a low price and impartial construction limits financial distortions whereas elevating substantial income.

Nevertheless, many nations have consumption taxes that exempt sure items and companies from VAT or tax them at a decreased price, requiring greater normal charges to boost adequate income. If not neutrally structured, excessive tax charges create financial distortions by discouraging the acquisition of extremely taxed items and companies in favor of untaxed, lower-taxed, or self-provided items and companies.

International locations with decrease consumption tax charges rating higher than these with greater tax charges, as decrease charges do much less to discourage financial exercise and permit for extra future consumption and funding.

The typical common consumption tax price within the OECD is nineteen.4 p.c. Hungary has the very best tax price at 27 p.c, whereas the US has the bottom tax price at 7.5 p.c.[55]

Desk 5. Consumption Taxes

Consumption Tax Base

Ideally, both a VAT or a gross sales tax needs to be levied at an ordinary price on all remaining consumption. In different phrases, consumption tax collections needs to be equal to the quantity of ultimate consumption within the economic system occasions the speed of the gross sales tax or VAT. Nevertheless, many nations’ consumption tax bases are removed from this ultimate. Many nations exempt sure items and companies from the VAT or tax them at a decreased price, requiring the next normal price than would in any other case be crucial, or apply the tax to enterprise inputs, rising the price of capital.

VAT/Gross sales Tax ExemptionA tax exemption excludes sure revenue, income, and even taxpayers from tax altogether. For instance, nonprofits that fulfill sure necessities are granted tax-exempt standing by the Inside Income Service (IRS), stopping them from having to pay revenue tax. Threshold

Most OECD nations set exemption thresholds for his or her VATs/gross sales taxes. If a enterprise is beneath a sure annual income threshold, it’s not required to take part within the VAT system. Which means that small companies—in contrast to companies above that threshold—don’t accumulate VAT on their outputs offered to clients but additionally can’t obtain a refund for VAT paid on enterprise inputs.[56] Though exempting very small companies saves administrative and compliance prices, unnecessarily giant thresholds create a distortion by favoring smaller companies over bigger ones.

International locations obtain higher scores for decrease thresholds. The Czech Republic receives the worst threshold rating with a VAT threshold of $154,336.[57] Seven nations obtain the most effective scores for having no common VAT/gross sales tax exemption threshold (Chile, Colombia, Costa Rica, Mexico, Spain, Turkey, and the US). The typical throughout the OECD nations which have a VAT threshold is roughly $69,000.[58]

Consumption Tax Base as a P.c of Complete Consumption

One technique to measure a rustic’s VAT base is the VAT income ratio. This ratio seems on the distinction between the VAT income really collected and collectible VAT income below a VAT that was utilized at the usual price on all remaining consumption. The distinction in precise and potential VAT revenues is because of 1) coverage decisions to exempt sure items and companies from VAT or tax them at a decreased price, and a couple of) missing VAT compliance.[59]

For instance, if remaining consumption in a rustic is $100 and a rustic levies a ten p.c VAT on all items and companies, a pure base would increase $10. Income assortment beneath $10 displays both a excessive variety of exemptions or decreased charges constructed into the tax code or low ranges of compliance (or each). The bottom is measured as a ratio of the pure base collections to the precise collections. International locations with tax base ratios close to 1—signifying a pure tax base—rating higher.

Beneath this measure, New Zealand has the broadest tax base overlaying roughly 96 p.c of whole consumption. Luxembourg and Korea comply with with ratios of 0.82 and 0.70, respectively. Mexico (0.35), the US (0.36), and Colombia (0.39) have the worst ratios. The OECD common tax base ratio is 0.55.[60]

Property Taxes

Property taxes are authorities levies on the property of a person or enterprise. The strategies and intervals of assortment range extensively among the many sorts of property taxes. Property and inheritance taxes, for instance, are due upon the dying of a person and the passing of his or her property to an inheritor, respectively. Taxes on actual property, however, are paid at set intervals–usually yearly–on the worth of taxable property corresponding to land and actual property.

Many sorts of property taxes are extremely distortive and add important complexity for taxpayers. Property and inheritance taxes create disincentives towards further work and saving, which damages productiveness and output. Monetary transaction taxes improve the price of capital, which limits the move of funding capital to its most effective allocations.[61] Taxes on wealth restrict the capital out there within the economic system, which damages long-term financial progress and innovation.[62]

Sound tax coverage minimizes financial distortions. Apart from taxes on land, most property taxes improve financial distortions and have long-term unfavorable results on the economic system and its productiveness.

Desk 6 reveals the ranks and scores for the Property Taxes class and every of its subcategories, that are actual property taxes, wealth and property taxes, and capital and transaction taxes.

Actual Property Taxes

Actual property taxes are levied on a recurrent foundation on taxable property. For instance, in most states or municipalities in the US, companies and people pay a property tax primarily based on the worth of their actual property.

Construction of Property Taxes

Though taxes on actual property are typically an environment friendly technique to increase income, some actual property taxes can develop into direct taxes on capital. This happens when a tax applies to extra than simply the worth of the land itself, such because the buildings or buildings on the land. This will increase the price of capital, discourages the formation of capital (such because the constructing of buildings), and may negatively affect enterprise location selections.

When a enterprise needs to enhance its property by means of renovations or increasing a manufacturing unit, a property tax that applies to each the land and people enhancements straight will increase the prices of these enhancements. Nevertheless, a tax that simply applies to the worth of the land would normally not create an incentive towards property enhancements.

International locations that tax the worth of buildings and buildings, in addition to land, obtain the worst scores on the ITCI. Some nations mitigate this therapy with a deduction for property taxes paid towards company taxable revenue. These nations obtain barely higher scores. International locations obtain the very best rating if they’ve both no property tax or solely tax land.

Desk 6. Property Taxes

Each OECD nation besides Australia and Estonia applies its property tax to all capital (land and buildings/buildings).[63] These two nations solely tax the worth of land, which excludes the worth of any buildings or buildings on the land. Of the 36 OECD nations with taxes on all capital, 31 permit for a deduction towards company taxable revenue.[64]

Actual Property Tax Collections

The variable “property tax collections” measures property tax revenues as a p.c of a rustic’s non-public capital inventory. Increased tax burdens, particularly when on capital, are inclined to sluggish funding, which damages productiveness and financial progress.

International locations with a excessive degree of collections as a p.c of their capital inventory place a bigger tax burden on taxpayers and obtain a worse rating on the ITCI. Seven nations within the OECD have property tax collections which can be larger than 1 p.c of the non-public capital inventory. Main this group are the UK (2.6 p.c), the US (1.8 p.c), and Canada (1.6 p.c). 13 nations have an actual property tax burden of beneath 0.1 p.c of the non-public capital inventory.[65]

Wealth and Property Taxes

Many nations additionally levy property taxes on a person’s wealth. These taxes can take the type of property or inheritance taxes which can be levied both upon a person’s property at dying or upon the property transferred from the decedent’s property to the heirs. These taxes also can take the type of a recurring tax on a person’s wealth. Property and inheritance taxes restrict sources out there for funding or manufacturing and scale back the inducement to save lots of and make investments.[66] This discount in funding adversely impacts financial progress. Furthermore, these taxes, the property and inheritance taxAn inheritance tax is levied upon the worth of inherited property obtained by a beneficiary after a decedent’s dying. To not be confused with property taxes, that are paid by the decedent’s property primarily based on the dimensions of the full property earlier than property are distributed, inheritance taxes are paid by the recipient or inheritor primarily based on the worth of the bequest obtained. particularly, may be prevented with sure planning methods, which makes the tax an inefficient and unnecessarily complicated income.

Wealth Taxes

Along with property and inheritance taxes, some nations levy wealth taxes. Wealth taxes are sometimes low-rate, progressive taxes on a person’s or household’s property or the property of a company. Not like property taxes, wealth taxes are levied on an annual foundation. Whereas some nations levy a complete tax on web wealth, others restrict their wealth taxes to chose property, corresponding to safety accounts, monetary property held overseas, or actual property.

4 nations levy web wealth taxes, particularly Colombia, Norway, Spain, and Switzerland. Belgium, France, and Italy impose wealth taxes on chosen property. International locations with no kind of wealth tax obtain the most effective rating, nations with wealth taxes on chosen property obtain a mean rating, and nations with web wealth taxes obtain the bottom rating.[67]

Property, Inheritance, and Present Taxes

Property taxes are levied on the worth of a person’s taxable property on the time of dying and are paid by the property itself, whereas inheritance taxes are levied on the worth of property transferred to a person’s heirs upon dying and are paid by the heirs (not the property of the deceased particular person). Present taxes are taxes on the switch of property (money, shares, and different property) which can be usually used to forestall people from circumventing property and inheritance taxes by giving freely their property earlier than dying.

Charges, exemption ranges, and guidelines range considerably amongst nations. For instance, the US levies a prime price of 40 p.c on estates however has an exemption degree of $12.92 million. Belgium’s Brussels capital area, however, has an inheritance tax with an exemption of EUR 15,000 (USD 16,250)[68] and quite a lot of tax charges relying on who receives property from the property and what the property are.[69]

Property, inheritance, and present taxes create important compliance prices for taxpayers whereas elevating insignificant quantities of income. In keeping with OECD information for 2023, property, inheritance, and present taxes throughout the OECD raised a mean of 0.14 p.c of GDP in tax income, with the very best quantity raised being solely 0.8 p.c of GDP in France, regardless of France’s prime inheritance tax price of as much as 60 p.c in some circumstances.[70]

International locations with out these taxes rating higher than nations which have them. Twelve nations within the OECD don’t have any property, inheritance, or present taxes: Australia, Austria, Canada, Costa Rica, Estonia, Israel, Latvia, Mexico, New Zealand, Norway, Slovakia, and Sweden. All others levy an property, inheritance, or present tax.[71]

Capital, Wealth, and Property Taxes on Companies

There are numerous taxes nations levy on the property and glued capital of companies. These embody taxes on the switch of actual property, taxes on the web property of companies, taxes on elevating capital, and taxes on monetary transactions. These taxes contribute on to the price of capital for companies and scale back the after-tax price of return on funding.

Property Switch Taxes

Property switch taxes are taxes on the switch of actual property (actual property, land enhancements, equipment) from one particular person or agency to a different. A standard instance in the US is the true property switch tax, which is often levied on the state degree on the worth of properties which can be bought by people.[72] Property switch taxes symbolize a direct tax on capital and improve the price of buying property.

International locations obtain a worse rating if they’ve property switch taxes. Six OECD nations shouldn’t have property switch taxes: Chile, the Czech Republic, Estonia, Lithuania, New Zealand, and Slovakia.[73]

Company Asset Taxes

Much like wealth taxes, asset taxes are levied on the wealth, or property, of a enterprise. For example, Luxembourg levies a 0.5 p.c tax on the worldwide web wealth of nontransparent Luxembourg-based firms yearly.[74] Equally, cantons in Switzerland levy taxes on the web property of firms, various from 0.001 p.c to 0.5 p.c of company web property.[75] Different nations levy these taxes completely on financial institution property.

Twenty OECD nations have some kind of company wealth or asset tax. Fourteen of those nations have financial institution taxes of some kind.[76]

Capital Duties

Capital duties are taxes on the issuance of shares of inventory. Sometimes, nations both levy these taxes at very low charges or require a small, flat price. For instance, Switzerland requires resident firms to pay a 1 p.c tax on the issuance of shares of inventory.[77] A lot of these taxes improve the price of capital, restrict funds out there for funding, and make it tougher to type companies.[78]

International locations with capital duties rating worse than nations with out them. Ten nations within the OECD levy some kind of capital obligation.[79]

Monetary Transaction Taxes

A monetary transaction tax is a levy on the sale or switch of a monetary asset. Monetary transaction taxes take totally different kinds in numerous nations. Finland levies a tax of 1.6 p.c on the switch of Finnish securities. Then again, Poland levies a 1 p.c stamp obligation on exchanges of property rights primarily based on the transaction worth. For transactions on a inventory alternate, the tax is the duty of the customer.[80]

Monetary transaction taxes impose a further layer of taxation on the acquisition or sale of shares. Markets run on effectivity, and capital must move rapidly to its most economically productive use. A monetary transaction tax impedes this course of.[81]

The ITCI ranks nations with monetary transaction taxes worse than nations with out them. Fifteen nations within the OECD have monetary transaction taxes, together with France and the UK, whereas 23 nations don’t impose monetary transaction taxes.[82]

Cross-Border Tax Guidelines

In an more and more globalized economic system, companies usually increase past the borders of their house nations to succeed in clients and construct provide chains all over the world. International locations have outlined guidelines that decide how, or if, company revenue earned in overseas nations is taxed domestically. Cross-border tax guidelines comprise the programs and laws that nations apply to these enterprise actions.

There was a rising pattern of transferring from worldwide taxation towards a system of territorial taxation, wherein a rustic’s company tax is restricted to earnings earned inside its borders.[83] In a pure territorial tax system, firms solely pay taxes to the nation wherein they earn revenue. For the reason that Nineties, the variety of OECD nations with worldwide tax programs has dropped from greater than 20 to a handful.[84]

The US has a considerably distinctive strategy. Along with normal managed overseas company (CFC) guidelines and an exemption for foreign-sourced dividends, it has each inbound and outbound anti-avoidance measures. As a part of the Tax Cuts and Jobs Act (TCJA) in December 2017, the US adopted a hybrid worldwide tax system that exempted foreign-sourced dividends from home taxation, but additionally erected stronger and extra complicated base erosion guidelines.[85] The US system below the TCJA has three items: international intangible low-taxed revenue (GILTI), foreign-derived intangible revenue (FDII), and the bottom erosion and anti-abuse tax (BEAT). GILTI legal responsibility is successfully a ten.5 p.c minimal tax on supra-normal returns derived from sure overseas investments earned by US firms. FDII is designed to be a decreased price on exports of US firms related to mental property situated within the US. Successfully, FDII earnings are taxed at 13.125 p.c. Paired collectively, GILTI and FDII create a worldwide tax on intangible revenue.

BEAT is a coverage centered on cross-border deductible funds. It’s designed as a ten p.c minimal tax on US-based multinationals with gross receipts of $500 million or extra. The tax applies to funds by these giant multinationals if funds to CFCs exceed 3 p.c (2 p.c for sure monetary corporations) of whole deductions taken by a company.

The One Massive Lovely Invoice Act (OBBBA) of July 2025 amended a few of these provisions by eradicating their limitation to revenue from intangible property and renamed them. Starting in 2026, GILTI can be changed with web CFC-tested revenue (NCTI) and FDII can be changed with foreign-derived deduction eligible revenue (FDDEI). NCTI acts at the least tax of between 12.6 and 14 p.c on all overseas revenue of US firms. FDDEI is a 14 p.c tax on US revenue related to exports.[86]

The proposal for a worldwide minimal tax is dramatically altering the panorama for cross-border tax guidelines.[87] Many OECD nations are continuing to implement the worldwide minimal tax guidelines. As of July 2025, 27 OECD nations have adopted an income-inclusion rule below Pillar Two. Eleven nations haven’t adopted an IIR but. Additional, 24 OECD nations have up to now adopted an undertaxed-profits rule (UTPR), much like BEAT within the US.[88]

Desk 7 shows the general rank and rating for the Cross-Border Tax Guidelines class in addition to the ranks and scores for the subcategories—which embody a class for dividends and capital positive aspects exemptions (territoriality), withholding taxes, tax treaties, and anti-tax avoidance guidelines.

Territoriality

Beneath a territorial tax system, multinational companies pay taxes to the nations wherein they earn their revenue. Which means that territorial tax regimes don’t typically tax company revenue firms earn in overseas nations. A worldwide tax systemA worldwide tax system for firms, versus a territorial tax system, consists of foreign-earned revenue within the home tax base. As a part of the 2017 Tax Cuts and Jobs Act (TCJA), the US shifted from worldwide taxation in direction of territorial taxation.—such because the system beforehand employed by the US—requires firms to pay taxes on worldwide revenue, no matter the place it’s earned. A number of nations—as is now the case within the US—function some type of hybrid system.

International locations enact territorial tax programs by means of so-called “participation exemptions,” which embody full or partial exemptions for foreign-earned dividend or capital positive aspects revenue (or each). Participation exemptions remove the extra home tax on overseas revenue by permitting firms to disregard—some or all—overseas revenue when calculating their taxable revenue. A pure territorial system absolutely exempts foreign-sourced dividends and capital positive aspects revenue.

Firms primarily based in nations with worldwide tax programs are at a aggressive drawback as a result of they face doubtlessly greater ranges of taxation than their rivals primarily based in nations with territorial tax programs. Moreover, taxes on repatriated company revenue in an organization’s house nation improve complexity and discourage funding and manufacturing.[89]

The territoriality of a tax system is measured by the diploma to which a rustic exempts foreign-sourced revenue by means of dividend and capital positive aspects exemptions.

Desk 7. Cross-Border Tax Guidelines

Dividends Obtained Exemption

When a overseas subsidiary of a father or mother firm earns revenue, it pays company revenue tax to the nation wherein it does enterprise. After paying the tax, the subsidiary can both reinvest its earnings into ongoing actions (by buying gear or hiring extra staff, for instance) or it will probably distribute its earnings again to the father or mother firm within the type of dividends.

Beneath a worldwide tax system, the dividends obtained by a father or mother firm are taxed once more by the father or mother firm’s house nation, minus a tax credit score for taxes already paid on that revenue. Beneath a pure territorial system, these dividends are exempt from taxation within the father or mother’s nation.

International locations obtain a rating primarily based on the extent of dividend exemption they supply. International locations with no dividend exemption (worldwide tax programs) obtain the worst rating.

Twenty-seven OECD nations exempt all foreign-sourced dividends obtained by father or mother firms from home taxation. Eight nations permit 95 p.c or 97 p.c of foreign-sourced dividends to be exempt from home taxation. Three OECD nations—Chile, Colombia, and Mexico—have a worldwide or hybrid tax system that typically doesn’t exempt foreign-sourced dividends from home taxation. Eire is the newest nation to undertake a dividends-received exemption ranging from 2025.[90]

Department or Subsidiary Capital Positive aspects Exclusion

One other function of a world tax system is its therapy of capital positive aspects earned by means of overseas investments. When a father or mother firm invests in a overseas subsidiary (i.e., purchases shares in a overseas subsidiary), it will probably understand a capital acquire on that funding if it later divests the asset. A territorial tax system would exempt these positive aspects from home taxation, as they’re derived from abroad exercise.

Taxing foreign-sourced capital positive aspects revenue at home tax charges can discourage saving and funding.

International locations that exempt foreign-sourced capital positive aspects from home taxation obtain a greater rating on the ITCI. International-sourced capital positive aspects are absolutely excluded from home taxation in 25 OECD nations. Six nations partially exclude foreign-sourced capital positive aspects. Seven nations don’t exclude foreign-sourced capital positive aspects revenue from home taxation.[91]

Restrictions on Eligible International locations

A great territorial system would solely concern itself with the earnings earned inside the house nation’s borders. Nevertheless, many nations have restrictions on their territorial programs that decide when a enterprise’ dividends or capital positive aspects obtained from overseas subsidiaries are exempt from home tax.

Some nations deal with overseas company revenue otherwise relying on the nation wherein the overseas revenue was earned. For instance, a number of nations limit their territorial programs primarily based on a “blacklist” of nations that don’t comply with sure necessities. Amongst EU nations, it is not uncommon to limit the participation exemption to member states of the European Financial Space.