{kind=link}

Key Findings

- Property taxes at the moment generate 70 % of all native taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of normal authorities providers, items, and actions. income, some or all of which must get replaced with different taxes underneath property taxA property tax is primarily levied on immovable property like land and buildings, in addition to on tangible private property that’s movable, like automobiles and gear. Property taxes are the only largest supply of state and native income within the U.S. and assist fund faculties, roads, police, and different providers. repeal.

- Changing the property tax with newly granted native taxing authority is exceedingly tough, as a result of native gross sales and revenue tax bases fluctuate broadly throughout jurisdictions; there might, as an illustration, be no possible gross sales taxA gross sales tax is levied on retail gross sales of products and providers and, ideally, ought to apply to all ultimate consumption with few exemptions. Many governments exempt items like groceries; base broadening, corresponding to together with groceries, might preserve charges decrease. A gross sales tax ought to exempt business-to-business transactions which, when taxed, trigger tax pyramiding. price by which an agricultural county or bed room neighborhood might change its property tax income.

- Backfilling forgone native property tax income by new state taxes is tough as a result of it dramatically shifts total tax burdens, undermines native accountability, and can’t simply regulate for altering inhabitants mixes.

- All income options are much less conducive to financial development than the prevailing property tax regime, however some switch regimes are sharply degrowth.

- Taxpayers ought to have the chance to judge plans for changing property tax income, not simply guarantees of repeal with out trade-offs.

Introduction

The property tax won’t ever win any recognition contests. Economists maintain it in excessive regard, however, maybe relatedly, economists are usually not terribly widespread both. It’s one factor, nevertheless, to favor property tax repeal within the summary: many Individuals are clearly for that. However with which taxes ought to it’s changed, and the way will the general bundle of property tax substitute be acquired?

Some proponents of property tax elimination want to postpone this dialog, advancing poll measures that repeal property taxes and cost the legislature with figuring out minor particulars like learn how to change the lion’s share of native tax income. The one accountable solution to think about property tax abolition, nevertheless, is to grapple with the options.

There are a lot of good arguments for reforming quite than changing property taxes, arguments we have now superior elsewhere.[1] This evaluation, nevertheless, largely units these points apart and easily asks: if not the property tax, then what?

Changing the most important supply of native tax income is not any simple activity. It’s rendered nonetheless tougher by the need of changing present revenues—or some substantial share of them—in every taxing jurisdiction, since various income streams have totally different geographic distributions. Even when a high-rate native gross sales tax have been capable of offset property taxes in a neighborhood dominated by retail institutions, as an illustration, it might be woefully insufficient to the duty of changing income in a bed room neighborhood or in farm nation.

New statewide taxes create their very own distributional challenges. As soon as the property tax and its apparatuses (together with assessments) vanish, how ought to revenues be allotted to cities, counties, and different native jurisdictions in future years? Ought to a substitute funding mechanism be based mostly on every jurisdiction’s prior yr collections, in essence subsidizing higher-tax jurisdictions with state funds in perpetuity? Or ought to funding be equalized by inhabitants or a method estimating a jurisdiction’s wants, yielding vastly totally different distributions than exist at current?

Moreover, as communities evolve each in inhabitants and financial standing, how would state funding regulate? Stripped of the property tax as an anchor, might lawmakers design a neighborhood funding system with out an inadvertent incentive construction that stifles development and rewards fiscal mismanagement and financial stagnation?

This paper examines a variety of choices, with pattern calculations and discussions of trade-offs. The unavoidable conclusion: each potential substitute choice has a number of issues that might render it undesirable to most taxpayers. Disposing of the property tax could also be widespread. Changing it gained’t be.

Evaluating Income Options

The property tax generates 70 % of all native tax income. It accounts for greater than 80 % of native tax income in 18 states (with a 95 % share or greater in seven), and provides lower than 50 % in solely 5 states and the District of Columbia. In truth, native governments throughout the nation herald twice as a lot in property tax income as state governments do in revenue taxes, although these numbers are skewed by the choice of 9 states to forgo wage revenue taxes. Even limiting the evaluation to the 41 states (and the District of Columbia) with broad-based revenue taxes, nevertheless, native property taxes elevate 59 % greater than state revenue taxes do.[2]

Not all of this falls on owners, after all. An estimated 42 % of native property tax is imposed on companies—on their land and constructions, but in addition, incessantly, on their equipment and gear.[3] Public utilities additionally pay property taxes, which could be vital, and the rest falls on residential property—each single- and multi-family models, starting from indifferent single-family properties to high-rise residence buildings. Condominium dwellers don’t remit property taxes straight, however they bear a lot of the financial incidence of the tax within the type of greater hire funds, typically with out the advantages (like homestead exemptions and decrease evaluation ratios) obtainable to owners.[4]

We assume, for functions of this publication, that lawmakers will search to interchange all present property tax income. In fact, some might favor to not offset all current income, allowing some stage of total tax discount. Stopping wanting full substitute would cut back the required charges of other taxes, however this may not have an effect on this paper’s broader evaluation of the challenges confronting those that want to change the property tax with one thing else. We start with proposals to offset the property tax by extra native taxing authority earlier than exploring the extra possible approaches involving state-level assumption of forgone property tax income.

Native-Stage Property Tax Alternative Choices

Thirty-eight states authorize native choice gross sales taxes. Some solely grant this authority to sure jurisdictions, although most present broad city- or county-level authority. Sometimes, native gross sales taxes are administered by the state and are imposed on the statewide gross sales tax baseThe tax base is the overall quantity of revenue, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slim tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges., however native governments incessantly have their very own rate-setting authority, and the state merely administers the tax and remits native collections to the suitable jurisdiction.[5]

No less than theoretically, states might elevate or remove any current caps on native gross sales taxes, or authorize such taxes for the primary time, as an alternative choice to native property taxes. In observe, nevertheless, that is nearly definitely a non-starter.

Native choice gross sales taxes can alleviate stress on property taxes. They’re a big supply of native tax income in some states, notably in a number of lower-income southern states the place it’s tough to lift sufficient income per capita from a single tax with out exorbitantly excessive charges.

In Arkansas, as an illustration, median family revenue is 76 % of the nationwide determine, family consumption is 80 % of the nationwide common, and median housing worth is 60 % of the US median.[6] Notably as soon as homestead exemptions, gross sales tax exemptions for widespread family expenditures, and revenue tax deductions are taken into consideration, it may be onerous to lift vital sums from any given tax, on the state or native stage. Arkansas, due to this fact, has excessive native gross sales tax charges along with its property taxes. Different states with higher-income populations might additionally lean on native gross sales taxes to cut back reliance on property taxes. It will be just about not possible, nevertheless, for native gross sales taxes to change property taxes.

That is partly as a result of property taxes are such a big and constant income generator. However it is usually as a result of native governments have been constructed round current funding mechanisms, and any local-level substitute would yield huge geographic disparities or require wildly totally different charges.

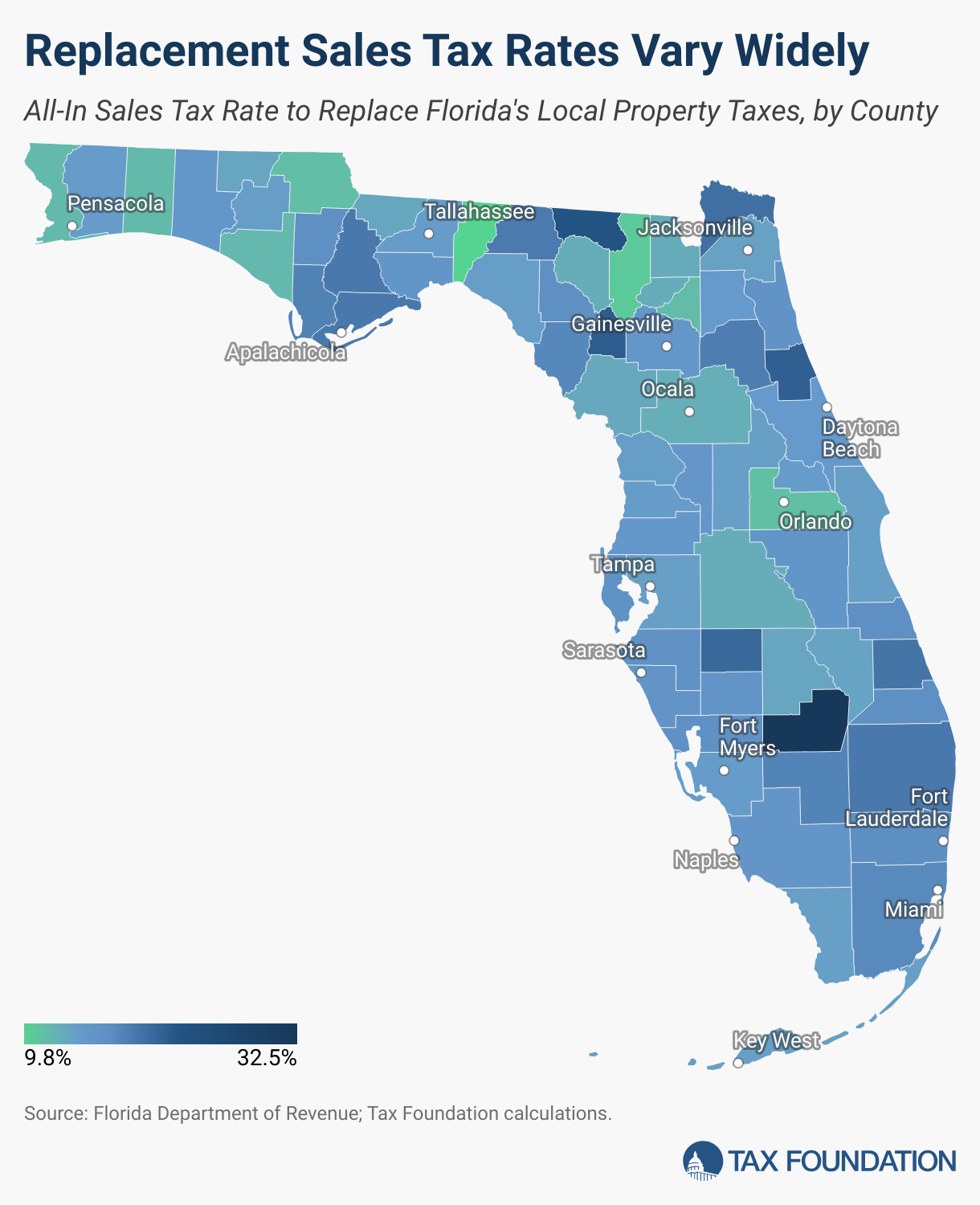

Take Florida, as an illustration. Presently, the mixed state-local common gross sales tax price is 7.02 %, consisting of a 6 % gross sales tax mixed with native charges starting from 0.0 to 1.5 %, with a weighted common of 1.02 %.[7] We estimate that the statewide common gross sales tax price must rise from 7.02 to fifteen.34 % to interchange the property tax, even with out accounting for any discount in taxable gross sales as a result of excessive price. But when counties, municipalities, college districts, and different native taxing authorities have been every answerable for changing the income with their very own native taxes, precise charges would fluctuate broadly.[8]

Tiny Jefferson County, with a inhabitants of lower than 15,000, is situated on the I-10 hall east of Tallahassee. It options truck stops and journey facilities, producing gross sales tax income vastly disproportionate to the inhabitants. For each share level on the gross sales tax, Jefferson raises $378 per capita, in comparison with a statewide common of $283. As a rural county with low inhabitants density, furthermore, property values are low. Jefferson County might change its present property tax collections with a mixed state and native gross sales tax price of solely 9.8 %.

On the different finish of the spectrum, equally small Glades County is basically agricultural and residential, and its retail focus is basically on tribal lands, which the county can’t tax. In Glades, the gross sales tax substitute price is an astronomical 32.5 %. For each share level on the gross sales tax, Glades County solely generates $61 per capita.

These are, after all, outliers, and each have extraordinarily modest populations. However they illustrate a broader problem: an answer which may work for Orange County (11.3 %) or Duval County (13.8 %) might not do for Broward or Miami-Dade (17.0 and 17.3 %, respectively), to say nothing of Palm Seashore (19.0 %) or Nassau (19.9 %).

With Orlando as its county seat, Orange County would require one of many decrease charges within the state, because it generates a lot gross sales tax income from guests and has such massive, tourism-driven leisure, amusement, and restaurant sectors. The ensuing 11.3 % offsetting price is due to this fact the bottom for a big county—and nonetheless, Orlando would instantly have the next gross sales tax price than any main metropolis within the nation has now. Presently, solely six main cities (outlined as these with a inhabitants of 200,000 or extra) have gross sales tax charges above 10 %, led by Seattle, Washington, at 10.35 %.

The upshot: even localities with vital retail focus or tourism exercise would require gross sales tax charges greater than any at the moment imposed within the US, whereas bed room communities and different predominantly residential or agricultural areas lack the gross sales tax base to recoup forgone property tax income at any possible gross sales tax price.

Essentially, such price differentials would induce cross-border buying, which might solely sharpen the disparities. Glades County residents might save 19 share factors on the gross sales tax by crossing the border to buy in neighboring Highland County. Tallahassee residents might save 4.4 % in neighboring Jefferson, and Miami-Dade residents might save 3.4 % buying in adjoining Monroe County. Additional reducing gross sales within the high-rate counties places nonetheless extra upward stress on the substitute income stream.

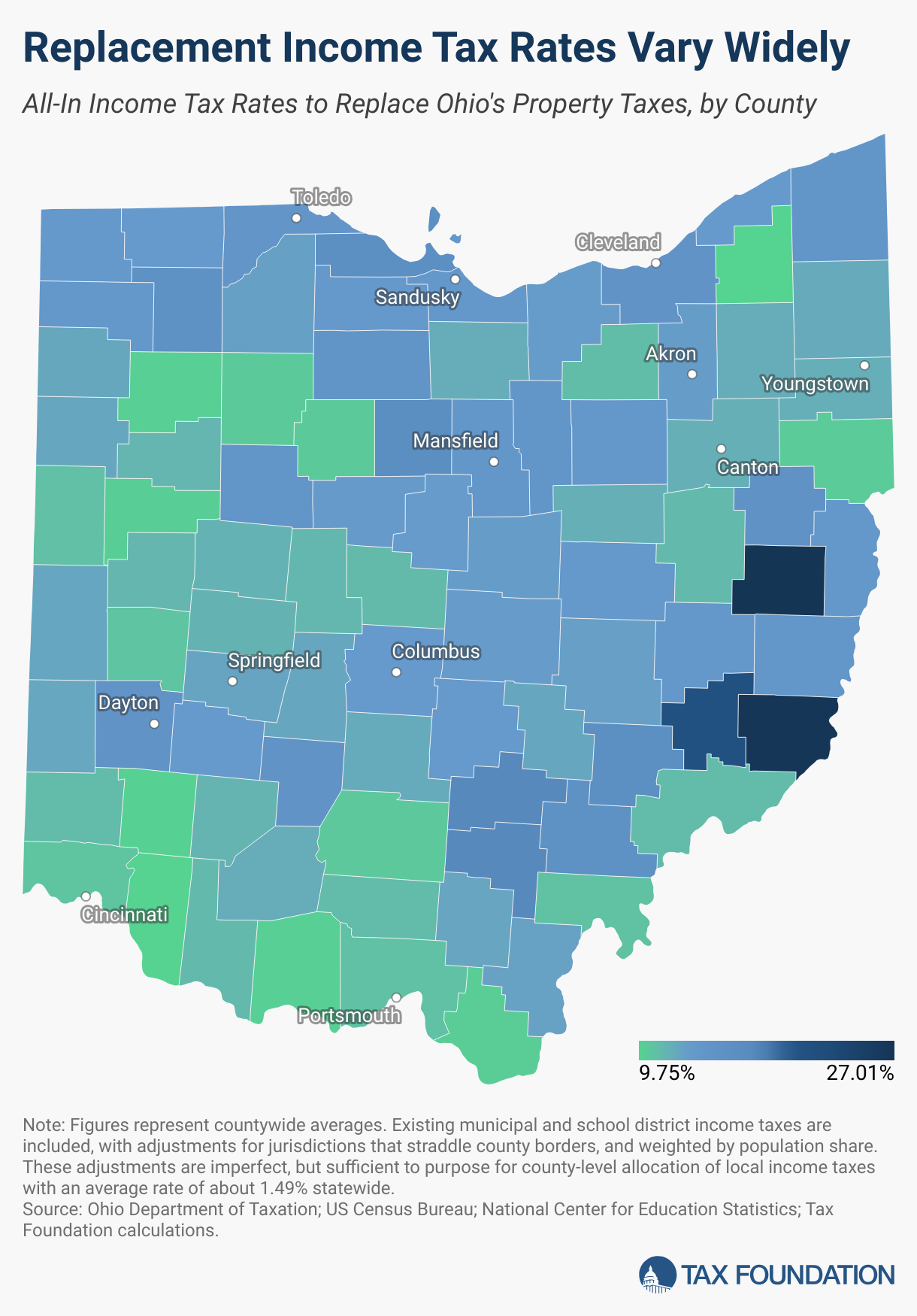

Native choice gross sales taxes are way more widespread than county or municipal revenue taxes, however native revenue taxation presents related distributional challenges. Ohio, which already authorizes municipal and faculty district revenue taxes, supplies a great living proof.

In 2026, Ohio’s state revenue tax will decline to a flat 2.75 %, whereas mixed municipal and faculty district taxes add an estimated additional 1.49 % statewide, although with vital variation throughout the state. If additional revenue taxes have been licensed on the county stage to offset the lack of property tax income in every county, these extra charges would common 8.35 %. That might deliver the statewide common, together with current state and municipal revenue taxes, to a 12.59 % flat taxAn revenue tax is known as a “flat tax” when all taxable revenue is topic to the identical tax price, no matter revenue stage or property., nearly on par with California’s prime marginal price on revenue over $1 million.[9] Presently, the nation’s highest state-level single price particular person revenue taxA person revenue tax (or private revenue tax) is levied on the wages, salaries, investments, or different types of revenue a person or family earns. The U.S. imposes a progressive revenue tax the place charges enhance with revenue. The Federal Earnings Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years outdated, particular person revenue taxes are the most important supply is 4.95 % in Illinois, and the best mixed state-local price is 6.65 % in Detroit, Michigan.

Right here too, nevertheless, statewide averages disguise dramatic variation. 5 counties would require extra charges beneath 6 %, the most important of which is Miami County outdoors of Dayton. Twenty would require double-digit extra revenue tax charges, led by Monroe County, a small, low-income county bordering West Virginia. Monroe County’s substitute price is 24.0 %. Whereas no municipality or college district in Monroe County levies its personal revenue tax at current, a brand new 26.75 % price in Monroe County will surely be a boon for its three West Virginia border counties throughout the Ohio River, the place the highest revenue tax price is 4.82 %.

Cuyahoga County, which comprises Cleveland, would require a 9.93 % substitute revenue tax price. Inside the metropolis of Cleveland itself, there may be a further 2.5 % municipal revenue tax, yielding an all-in price of 15.18 % for Cleveland (14.87 % averaged throughout the county). Cincinnati, in Hamilton County, would require a 6.68 % extra revenue tax to interchange its property taxes, atop a 1.8 % current metropolis price, for an all-in price of 11.23 % (and 10.63 % for the county as an entire). Cincinnati borders Kentucky, which is able to boast a state revenue tax price of three.5 % in 2026, plus 1.45 % in mixed native revenue taxes in adjoining Boone County. Toledo residents, in the meantime, may rue the choice that gave the Toledo Strip to Ohio quite than Michigan.

Native governments’ financial bases merely fluctuate too broadly to swap one tax system for one more and anticipate related revenues. If one had to decide on a neighborhood tax base for a completely new state, property can be a prudent selection, as relative property values are a fairly good proxy for the good thing about providers that every property proprietor receives. The property tax additionally strikes a wholesome center floor between the geographic distributions of revenue taxes, that are principally based mostly on place of residence (and generally place of employment), and gross sales taxes, which carry out higher in areas with retail focus. However this isn’t to say that the distribution of income underneath property taxes is the one conceivable selection, simply that it is the selection round which cities and counties have been structured, and that no various tax obtainable to native governments might change that income in every jurisdiction with out impossibly massive price variations.

That actuality is why most proposals for property tax elimination contain the state choosing up most or all the substitute value, to the extent that these plans counsel any particular supply of substitute income in any respect.

State-Stage Property Tax Alternative Choices

If the state assumes accountability for changing native income, that solves the preliminary geographic disparities however creates new ones. Lawmakers should determine whether or not to interchange revenues at current ranges—embedding financial inequalities and completely rewarding jurisdictions that beforehand imposed greater charges—or to make use of another method for income distribution, thereby inducing the dramatic income swings of the kind related to local-level replacements. Even when the state undertakes full income substitute, furthermore, lawmakers should work out learn how to regulate in future years, since there is not going to be new assessments on which to base the transfers.

Allow us to first think about the political problem of income backfill, which makes each jurisdiction complete, however underneath which the income to take action is generated from a statewide tax with a really totally different distribution of burdens.

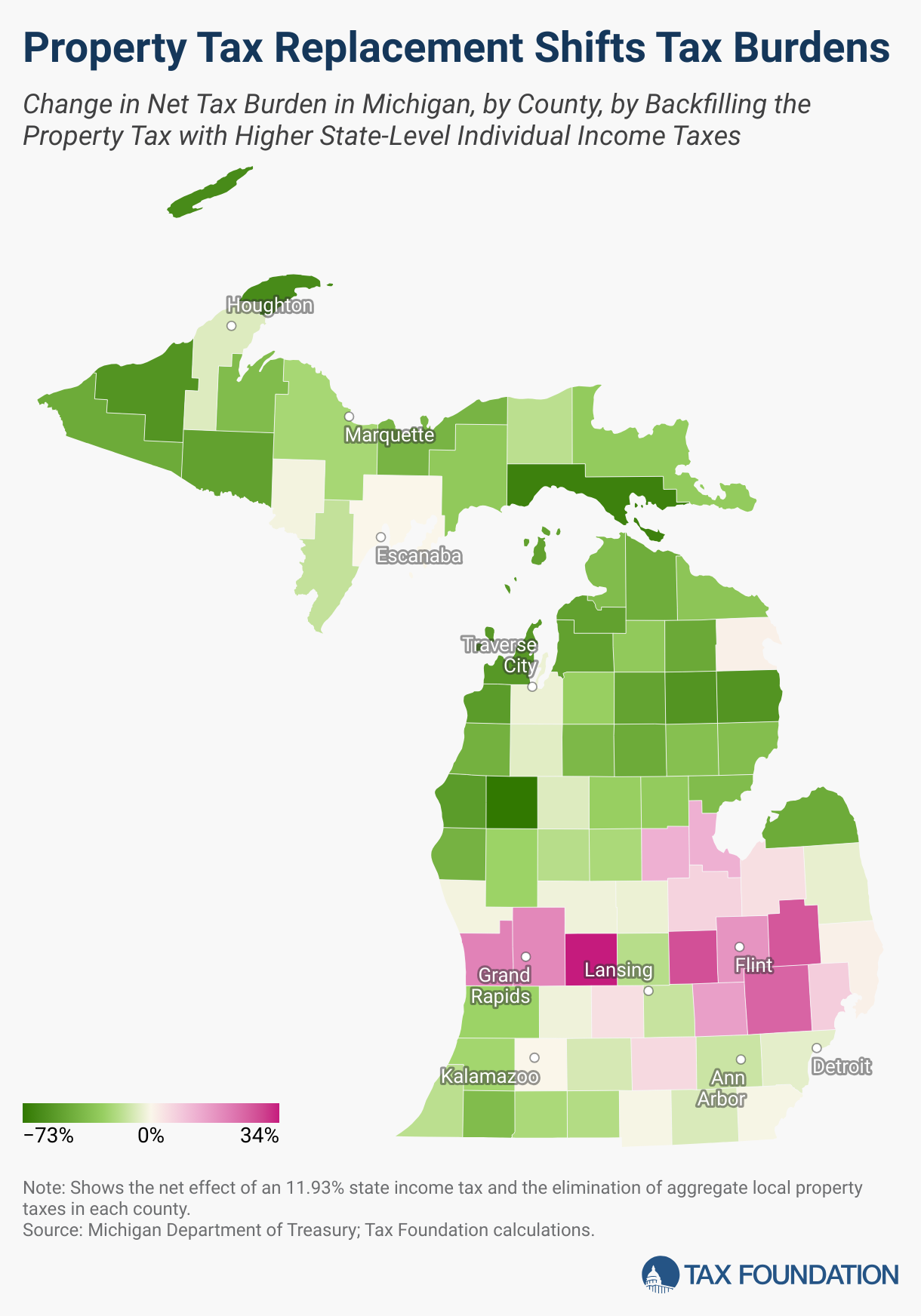

Michigan at the moment imposes a flat 4.25 % particular person revenue tax. To switch the property tax, the revenue tax must be imposed at a price of 11.93 %.[10] (Detroit, the one jurisdiction in Michigan with native revenue tax authority, would have a brand new all-in particular person revenue tax price of 14.33 %.)

Think about that Michigan imposed an 11.93 % revenue tax. Taxpayers in each jurisdiction would pay considerably extra in revenue tax, however their property tax burdens can be eradicated. Statewide, the 2 offset. However that might not be true on the particular person or jurisdictional ranges. Suppose that Michigan sought to make counties complete, utilizing the brand new state-level income to backfill no matter had been raised by property taxes in every county beforehand.

In Lake County, which, regardless of its identify, shouldn’t be on a Nice Lake and is only one.2 % water, revenue taxpayers contribute lower than $4.5 million to the state underneath the present system (on the 4.25 % price), however property taxes herald $29.5 million. There, residents would pay a further $8.1 million in state revenue taxes whereas being relieved of their $29.5 million property tax burden—a web tax discount of 73 %. In Ionia County, the place many prosperous Grand Rapids commuters reside, the alternative is true: residents would pay a further $96.8 million in revenue tax to keep away from $72.5 million in property tax payments, a 34 % tax enhance. Wayne County, house of Detroit, would see a 6 % discount in total tax burdens, whereas Oakland County, the location of Detroit’s northern suburbs, would take up a 25 % tax enhance. Ingham County, the place Lansing is situated, would get a 14 % web tax discount. Alternatively, Kent County, house of Grand Rapids, would expertise a 19 % tax hike.

Any substitute of current property tax income locks the impact of present charges (mill levies) in place, successfully subsidizing counties and municipalities with excessive current property tax charges. Presently, at the least, these taxes are paid by residents who additionally profit from the providers supplied by these excessive charges. If states have been to backfill property tax income, localities that beforehand taxed at excessive charges would nonetheless get the good thing about them although residents would not be paying them, whereas jurisdictions with decrease property taxes would, in impact, subsidize the higher-tax jurisdictions. In observe, this may largely be a rural to city switch, with main cities—which generally impose greater property tax charges—receiving extra income than rural counties, although the state’s substitute tax income (from no matter supply) would apply statewide.

Not solely would residents of some jurisdictions subsidize the higher spending of different localities, however they might additionally lose their enter on the dimensions of native authorities. Localities would have much less motive to economize, as a result of doing so wouldn’t permit them to return any cash to native taxpayers. Jurisdictions the place taxpayers would like extra providers would likewise be hamstrung: they may not enhance their income even when there was overwhelming help for doing so.

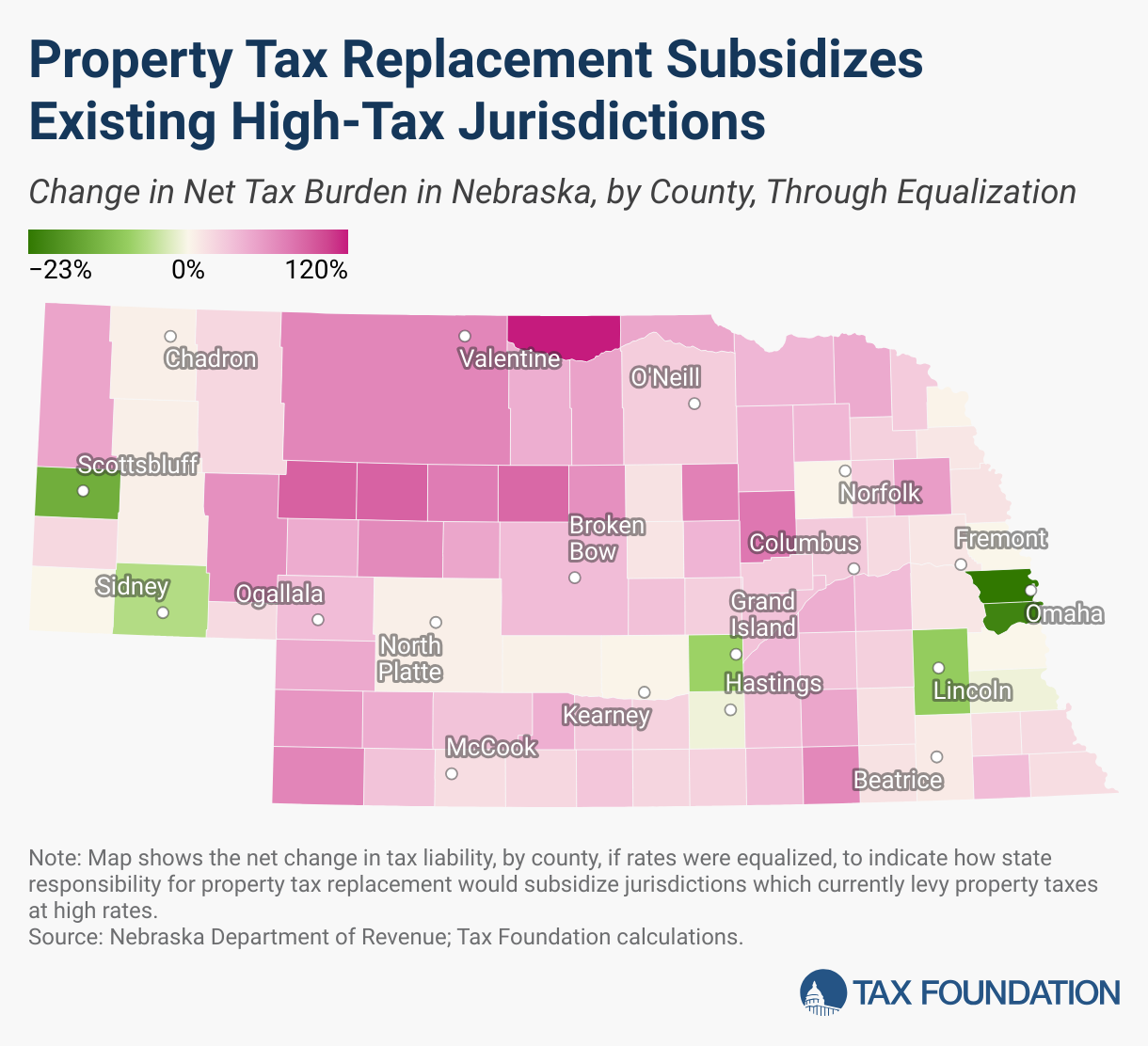

Utilizing Nebraska for instance, be aware that prime charges in Omaha, Lincoln, Grand Island, and Scottsbluff yield excessive subsidies to their counties, whereas many of the state’s remaining counties emerge as losers. Within the excessive, the county of Keya Paha would see its tax burden enhance by 120 % if it have been compelled to contribute an equalized share, whereas Douglas County (Omaha) would see a 23 % tax discount.[11]

This final calculation is, after all, largely a thought experiment, as no matter substitute income stream is chosen (possible revenue or gross sales taxes) will add additional layers of distortion not taken into consideration right here. However it might be useful to see the impact of those transfers damaged out, to see how states could be obligated to switch revenues to jurisdictions in perpetuity based mostly on charges they set earlier than repeal. Omaha residents at the moment pay extra in change for higher (or at the least extra expensive) authorities providers. Why ought to rural Nebraskans’ taxes enhance to subsidize Omaha’s greater spending?

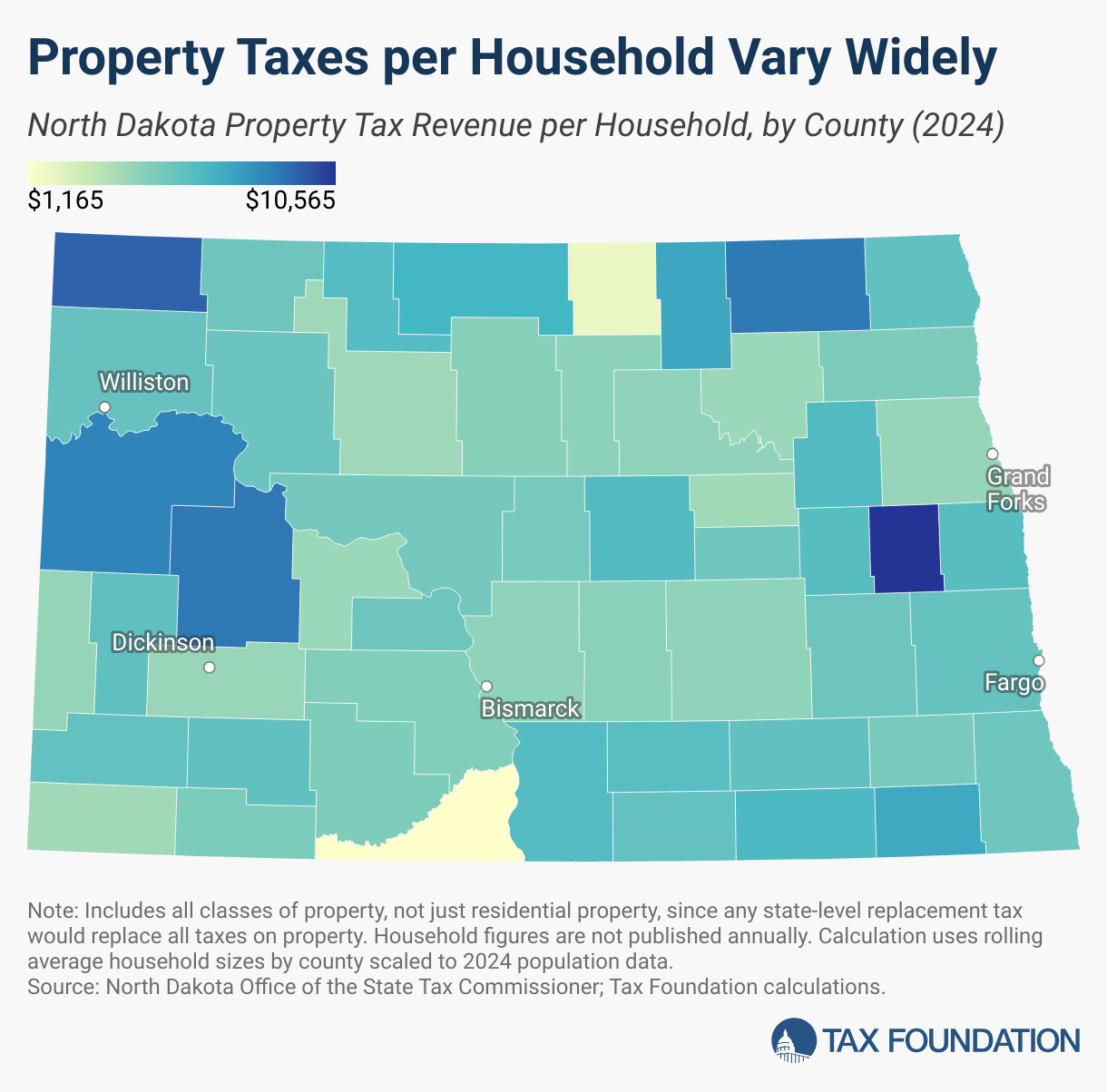

Current collections per family present additional perception into the challenges going through lawmakers hoping to centralize tax collections on the state stage and backfill current native tax collections. In North Dakota, the best variation in property tax collections arises from oil and fuel exercise, whereas in different states, disparities may mirror city versus rural areas, or the variations throughout enterprise districts, bed room communities, and farm nation. However nevertheless the variations come up, they are often substantial. Can residents of a North Dakota county the place property tax income runs $1,165 per family be anticipated to pay extra state-level revenue or gross sales taxes at a price that provides one other county a switch value $10,565 per family?[12]

Even when these challenges are surmounted and taxpayers settle for the brand new redistributions, policymakers should set a mechanism for adjusting transfers year-over-year. Some proposals notably lack any provision for such changes, suggesting that each jurisdiction ought to obtain the identical quantity—maybe inflationInflation is when the final worth of products and providers will increase throughout the financial system, lowering the buying energy of a foreign money and the worth of sure property. The identical paycheck covers much less items, providers, and payments. It is usually known as a “hidden tax,” because it leaves taxpayers much less well-off on account of greater prices and “bracket creep,” whereas rising the federal government’s spendin-adjusted, maybe not—in perpetuity, however this creates a perverse incentive for financial decay.

Rising communities would obtain fewer {dollars} per capita, whereas shrinking communities would see their per capita switch revenues enhance. The “good” coverage, due to this fact, is degrowth. Residents would have sturdy incentives to discourage new improvement and to drive out new or increasing companies. As a substitute of financial vitality serving as a supply of extra income, development would stretch a locality’s funds skinny. All replacements for the property tax are much less pro-growth than the prevailing system, however the distribution mechanism could make the general system profoundly degrowth.

Conversely, dying communities would discover themselves flush with money on a per capita foundation, although they might be disincentivized from spending it in ways in which would revitalize the neighborhood and entice new residents. Native leaders can be incentivized to determine spending that lavishes advantages on current residents with out constructing out facilities or providers which may entice new ones. That is hardly a recipe for fulfillment, on the native stage or statewide.

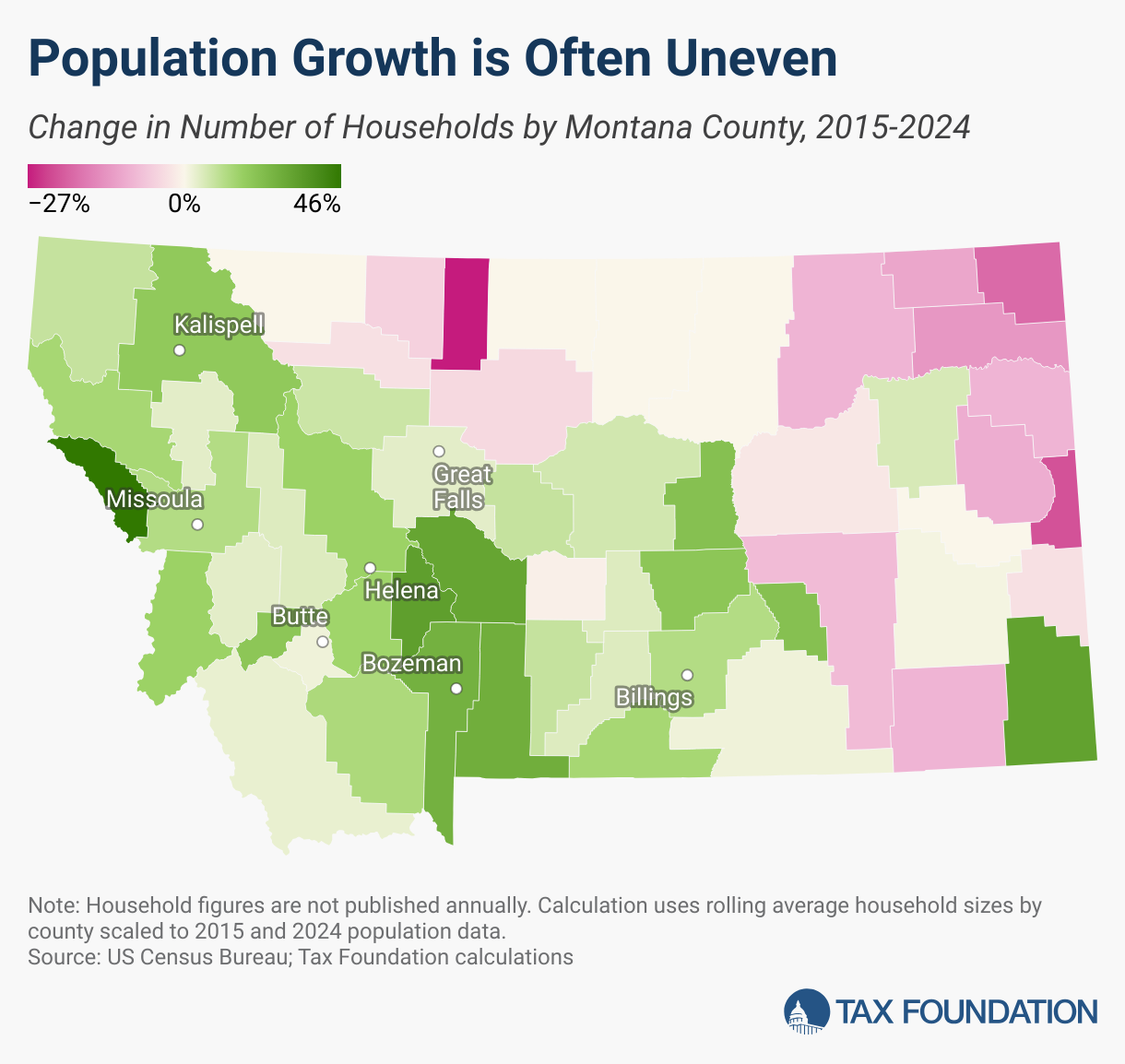

In some states, populations are at the moment rising fairly quickly, although erratically. In Montana, as an illustration, counties within the jap a part of the state are dropping inhabitants, whereas the western half of the state is booming. What would occur if Bozeman acquired the identical quantity of income now (maybe inflation-adjusted) because it did for a a lot smaller inhabitants a decade in the past?

A per capita or per family adjustment might tackle this concern, however fairly imperfectly. New developments, as an illustration, could be dearer and have higher-value properties or companies. Moreover, blockbuster development may require funding in new infrastructure and expanded providers that require greater than only a per capita adjustment. A hard and fast state method can’t account for these wants and is unresponsive to native preferences. A rising and extra prosperous inhabitants may need higher facilities and be keen to pay for them, but it surely can’t accomplish that if native funding is overwhelmingly concentrated on the state stage. One other neighborhood may favor extra restricted authorities and the decrease taxes that associate with it, however that selection is taken away from residents, too, for the reason that jurisdiction’s funding is about by state lawmakers, utilizing statewide tax income.

Even with inhabitants changes, native governments can be incentivized to withstand any new financial exercise that will increase authorities prices, irrespective of how vital the broader financial advantages. Native financial development makes no distinction for the property tax’s state-level income substitute, whereas any prices are borne out of that fastened sum.

Lawmakers might as an alternative use another support method (as states already do for varsity equalization), although a system that makes an attempt to supply the identical quantity of funding per family statewide shall be grossly inadequate to satisfy the wants of some communities the place service supply prices are greater, and a system that tries to deal with native value disparities will contain a large-scale, perpetual switch from inexpensive communities to extra expensive ones.

In all circumstances, there may be an erosion of native autonomy. Presently, high-tax jurisdictions should justify these greater taxes, however underneath a system of full state backfill, they might obtain the identical quantity no matter what providers they ship or how properly they ship them.

Conclusion

Given the pitfalls of every potential strategy to property tax substitute, it’s unsurprising that many advocates of repeal wish to defer deliberations on a substitute till after the property tax’s abolition is accepted. However that’s no excuse. Each coverage selection includes trade-offs, and for a coverage change as radical as property tax elimination, it’s irresponsible to contemplate repeal individually from proposals to interchange the forgone income.

Proponents of property tax repeal ought to be having frank conversations about which taxes would change it, what charges can be essential, and who would pay extra. They need to have a plan for the way the substitute revenues can be allotted, and the way changes can be made in future years. And they need to grapple with the motivation construction created by a system by which native governments might not management their very own revenues, and the place expenditures could also be impartial of the tax prices of these selections, which could possibly be socialized throughout all taxpayers, no matter the place they reside.

Repealing the property tax is an aspiration, not a plan. If proponents of property tax elimination have plans for learn how to change it, voters ought to have a possibility to judge these plans upfront. And in the event that they don’t have a plan, voters ought to know that too.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted specialists delivered straight to your inbox.

[1] See Jared Walczak, “Confronting the New Property Tax Revolt,” Tax Basis, Nov. 5, 2024, https://taxfoundation.org/analysis/all/state/property-tax-relief-reform-options/, notably the sections on levy (income) limits and deferral packages.

[2] US Census Bureau, “Annual Survey of State and Native Authorities Funds,” 2023 knowledge (July 2025), https://www.census.gov/knowledge/datasets/2023/econ/native/public-use-datasets.html.

[3] Tax Basis estimate based mostly on EY/COST enterprise figures. See Council on State Taxation, “Complete State and Native Enterprise Taxes,” December 2024, https://www.value.org/globalassets/value/state-tax-resources-pdf-pages/cost-studies-articles-reports/score_ey-50-state-tax-burden-study_final_121824.pdf.

[4] On the incidence of property taxes on renters, see, e.g., Robert J. Carroll and John Yinger, “Is the Property Tax a Profit Tax? The Case of Rental Housing,” Nationwide Tax Journal 47 (June 1994): 295-316; and Leah J. Tsoodle and Tracy M. Turner, “Property Taxes and Residential Rents,” Journal of Actual Property Economics 36:1 (2008): 63-80.

[5] For a dialogue of variations in gross sales tax administration, see Jared Walczak and Janelle Fritts, “State Gross sales Taxes within the Put up-Wayfair Period,” Tax Basis, Dec. 12, 2019, https://taxfoundation.org/analysis/all/state/state-remote-sales-tax-collection-wayfair/.

[6] Tax Basis calculations based mostly on US Census Bureau and IRS knowledge. See US Census Bureau, “Annual Survey of State and Native Authorities Funds”; and Inside Income Service, “Statistics of Earnings” by state.

[7] Jared Walczak, “State and Native Gross sales Tax Charges, Midyear 2025,” Tax Basis, Jul. 8, 2025, https://taxfoundation.org/knowledge/all/state/sales-tax-rates/.

[8] Tax Basis calculations utilizing income from the Florida Division of Income, utilizing grossed-up 2024 knowledge. For current native surtaxA surtax is a further tax levied on prime of an already current enterprise or particular person tax and might have a flat or progressive price construction. Surtaxes are usually enacted to fund a particular program or initiative, whereas income from broader-based taxes, like the person revenue tax, usually cowl a mess of packages and providers. charges, see Florida Division of Income, “Discretionary Gross sales Surtax Info for Calendar 12 months 2024,” https://floridarevenue.com/Forms_library/present/dr15dss_24.pdf. For property tax knowledge, see Id., “Florida Advert valorem Valuation and Tax Knowledge Guide,” https://floridarevenue.com/property/Pages/DataPortal_DataBook.aspx. Further knowledge on normal tax collections are from the Workplace of Tax Analysis Collections and Distributions, https://floridarevenue.com/dataPortal/Pages/TaxResearch.aspx.

[9] Tax Basis calculations utilizing knowledge from the Ohio Division of Taxation and the US Census Bureau, with college districts mapped utilizing Nationwide Heart for Training Statistics knowledge. A industrial massive language mannequin (LLM) was used to course of college district form information. See Ohio Division of Taxation, Tax Knowledge Sequence, https://tax.ohio.gov/researcher/tax-data-series; and Id., “The Finder” (for municipal and faculty district revenue tax price databases), https://tax.ohio.gov/help-center/the-finder/the-finder.

[10] Tax Basis calculations utilizing knowledge from the Michigan Division of Treasury with changes for base years. See Michigan Division of Treasury, “Michigan’s Particular person Earnings Tax 2020,” December 2022, https://www.michigan.gov/mdhhs/-/media/Challenge/Web sites/treasury/Uncategorized/2022/ORTA-Tax-Studies/IIT-report_TY2020-data_UPDATED_Final.pdf; and Id., “2023 Advert Valorem Property Tax Report,” https://www.michigan.gov/taxes/-/media/Challenge/Web sites/taxes/Tax-Levy-Studies/2023-Advert-Valorem-Tax-Levy-Report.pdf.

[11] Tax Basis calculations; Nebraska Division of Income, “2022 Certificates of Taxes Levied Studies,” 2023, https://income.nebraska.gov/websites/default/information/doc/pad/analysis/valuation/2023/avgrate2022.pdf.

[12] Tax Basis calculations based mostly on North Dakota Workplace of the State Tax Commissioner and US Census knowledge. See North Dakota Workplace of the State Tax Commissioner, “Taxable Valuation of Property Topic to the Normal Property Tax – 2024,” https://www.tax.nd.gov/websites/www/information/paperwork/property-tax/2024-Property-Tax-Statistical-Report.pdf.

Share this text