{kind=link}

Key Findings

- Policymakers are contemplating methods to increase the enhancements made to Reasonably priced Care Act premium taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of normal authorities companies, items, and actions. credit (PTCs) that expire on the finish of the 12 months, which might price $350 billion over the subsequent decade.

- Any enlargement of the credit needs to be offset by decreasing different healthcare subsidies or preferences within the tax code, the most important of which is the exclusion for employer-sponsored medical health insurance (ESI) premiums, estimated to price greater than $5 trillion over the subsequent decade as a consequence of lowered earnings and payroll taxA payroll tax is a tax paid on the wages and salaries of workers to finance social insurance coverage packages like Social Safety, Medicare, and unemployment insurance coverage. Payroll taxes are social insurance coverage taxes that comprise 24.8 p.c of mixed federal, state, and native authorities income, the second largest supply of that mixed tax income. income.

- We analyze 4 choices to restrict the earnings tax exclusion for ESI on the 80th and 90th percentiles of premiums, discovering these choices would increase substantial quantities of income—as much as $389 billion over the subsequent decade—with the impacts falling totally on the highest 10 p.c of earners.

Introduction

Policymakers are contemplating methods to increase the enhancements made to Reasonably priced Care Act premium tax credit (PTCs) that expire on the finish of the 12 months, which had been initially offered on a brief foundation as a part of the American Rescue Plan Act of 2021 and later prolonged as a part of the InflationInflation is when the overall worth of products and companies will increase throughout the financial system, decreasing the buying energy of a forex and the worth of sure belongings. The identical paycheck covers much less items, companies, and payments. It is typically known as a “hidden tax,” because it leaves taxpayers much less well-off as a consequence of increased prices and “bracket creep,” whereas growing the federal government’s spendin Discount Act of 2022.[1] The PTC enhancements cut back the utmost quantity eligible enrollees are required to contribute towards medical health insurance premiums for medical health insurance bought by way of the Reasonably priced Care Act exchanges and lengthen eligibility to folks whose earnings is above 400 p.c of the poverty degree.

The Congressional Funds Workplace (CBO) just lately estimated that completely extending the PTC enhancements would enhance the finances deficit by $350 billion over the 2026-2035 interval (relative to a baseline that features adjustments made beneath the One Large Stunning Invoice Act, or OBBBA).[2] The CBO additionally estimated 3.8 million extra folks would have medical health insurance in 2035 due to the extension.

Costing about $1 trillion over the subsequent decade, PTCs are the costliest tax credit score within the tax code, together with outlay results that end result from refundability.[3] Controlling the price of these and different healthcare subsidies, that are a big and rising share of the finances and rising quicker than the general financial system, is a crucial a part of reining within the federal authorities’s unsustainable fiscal trajectory.[4]

Moderately than decreasing healthcare prices, these subsidies have typically contributed to increased prices by boosting demand with out addressing provide constraints and have shifted the burden of the fee from shoppers to taxpayers.[5] Rising healthcare prices are anticipated to extend the price of insurance coverage premiums by greater than 9 p.c in 2026.[6] Any enlargement of PTCs needs to be offset by decreasing different healthcare subsidies or preferences within the tax code.

Whereas the tax code comprises a number of preferences for healthcare along with the PTCs, together with well being financial savings accounts and the deductibility of medical bills, far and away the most important is the exclusion for employer-sponsored medical health insurance (ESI) premiums, which can cut back earnings tax income by $3.9 trillion over the subsequent decade (2025-2034) based on the Treasury Division’s tax expenditureTax expenditures are departures from a “regular” tax code that decrease the tax burden of people or companies by way of an exemption, deduction, credit score, or preferential price. Nevertheless, defining which tax expenditures grant particular advantages to sure teams of individuals or forms of financial exercise isn’t all the time simple. estimates.[7] As a result of the exclusion additionally reduces payroll taxes that will in any other case apply to ESI, the whole lack of federal tax income is estimated at $5.9 trillion over the subsequent decade.

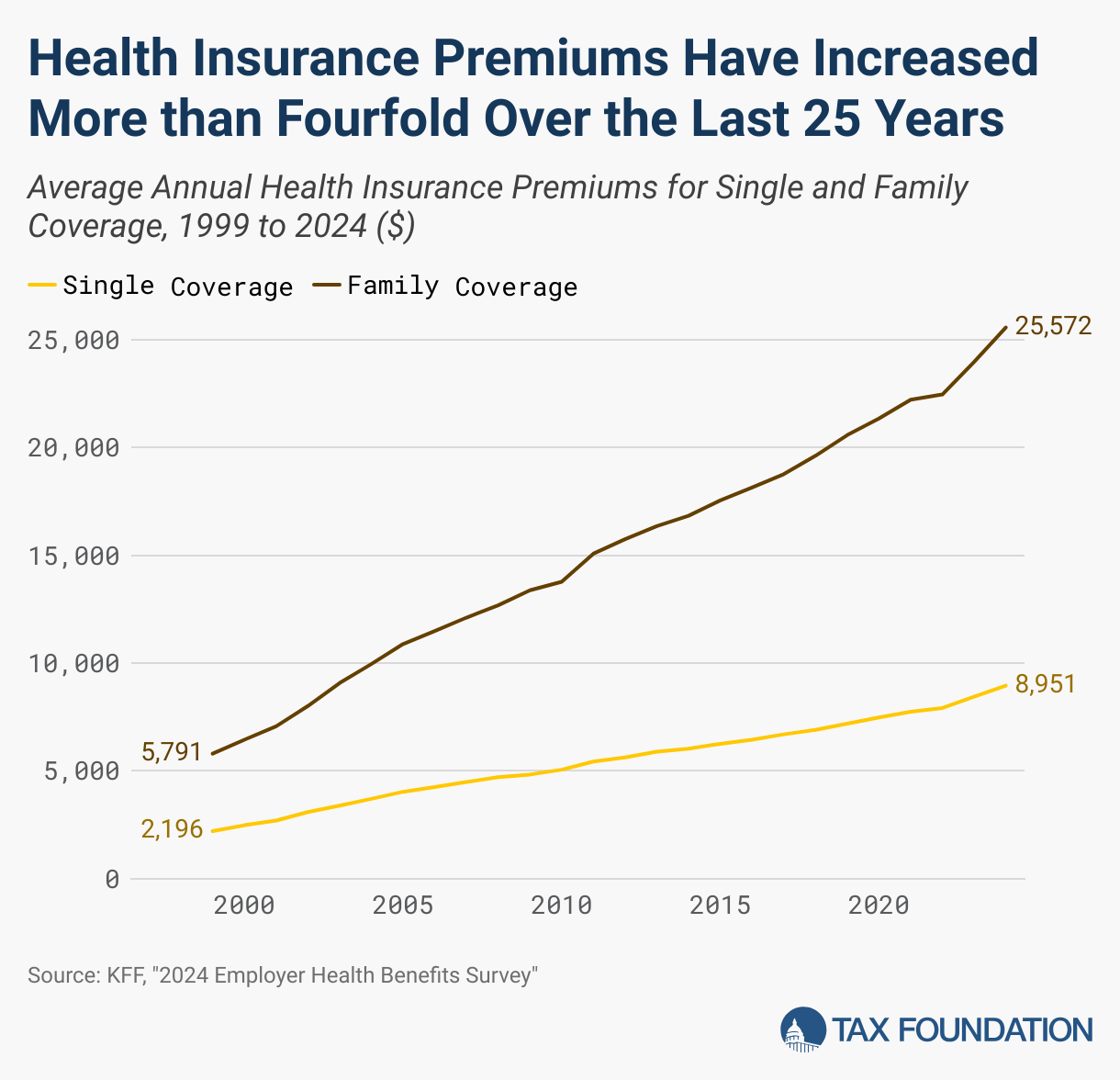

The exclusion for ESI has been in place since World Conflict II, creating an incentive for employers to shift pay packages towards untaxable ESI advantages quite than taxable wages and salaries, resulting in more and more beneficiant ESI advantages that increase demand for healthcare and put upward strain on healthcare costs.[8] During the last 25 years, progress in ESI advantages has outstripped progress in staff’ wages and inflation, with common annual premiums for ESI reaching $8,951 for single protection and $25,572 for household protection in 2024, based on the most recent survey by KFF.[9] The exclusion distorts the labor market and the healthcare market, because it favors expensive insurance coverage protection tied to employment quite than protection that travels from one job to the subsequent or direct funds to healthcare suppliers.[10]

Totally eliminating the exclusion for ESI would take away these distortions however lead to a significant tax enhance on staff. A extra incremental reform that caps the exclusion would scale back distortions on the margin, limiting the most expensive healthcare plans, and nonetheless increase substantial quantities of income. Within the evaluation that follows, we look at 4 choices to restrict the earnings tax exclusion (leaving the payroll tax exclusion in place) for ESI on the 80th and 90th percentiles of premiums, estimating income and distributional impacts over the subsequent decade.

Federal Income Impacts of Limiting the ESI Exclusion

We modeled the next 4 choices for limiting the earnings tax exclusion for ESI starting in 2026, relative to present regulation and accounting for the OBBBA:

- Restrict the earnings tax exclusion for ESI above the 80th percentile of premiums beginning in 2026 (estimated to be $14,329 for particular person protection and $36,929 for household protection in 2026 and rising thereafter to stay on the 80th percentile of premiums)[11]

- Restrict the earnings tax exclusion for ESI above the 80th percentile of premiums in 2026, thereafter indexing the 2026 nominal ESI cap to inflation (as measured by core PCE)

- Restrict the earnings tax exclusion for ESI above the 90th percentile of premiums beginning in 2026 (estimated to be $18,752 for particular person protection and $49,201 for household protection in 2026 and rising thereafter to stay on the 90th percentile of premiums)

- Restrict the earnings tax exclusion for ESI above the 90th percentile of premiums in 2026, thereafter indexing the 2026 nominal ESI cap to inflation (as measured by core PCE)

We estimate a spread of federal income results for these proposals (see Desk 1).[12] Choice 3 would increase the least income over the finances window, from 2026 to 2035: $138 billion on a standard foundation, or $135 billion on a dynamic foundation (i.e., accounting for financial impacts arising from a rise in marginal tax charges on labor earnings).[13]

Choice 2 would increase essentially the most income over the finances window: $389 billion on a standard foundation, or $371 billion on a dynamic foundation. Choices 2 and 4 increase further income within the years after 2026, relative to Choices 1 and three, as a result of the ESI cap that grows with inflation applies to a rising share of healthcare plans over time.

Desk 1. Income Results of Limiting the Tax Exclusion for ESI ($ Billions)

Supply: Tax Basis Basic Equilibrium Mannequin, September 2025

Distributional Impacts of Limiting the ESI Exclusion

Distributionally, we estimate that Choice 1 would scale back after-tax earnings by 0.2 p.c general in 2026 and in 2035, conventionally measured, with primarily the entire influence falling on the highest 10 p.c of earners. Accounting for the financial impacts doesn’t considerably change the distributional impacts. The opposite three coverage choices lead to related distributional impacts (see Desk 2).

Desk 2. Distributional Results of Limiting the Tax Exclusion for ESI (% Change in After-Tax Revenue, Conventionally Measured)

Be aware: Market earnings consists of adjusted gross earningsFor people, gross earnings is the whole of all earnings acquired from any supply earlier than taxes or deductions. It consists of wages, salaries, suggestions, curiosity, dividends, capital positive aspects, rental earnings, alimony, pensions, and different types of earnings.

For companies, gross earnings (or gross revenue) is the sum of whole receipts or gross sales minus the price of items bought (COGS)—the direct prices of manufacturing items (AGI) plus 1) tax-exempt curiosity, 2) non-taxable Social Safety earnings, 3) the employer share of payroll taxes, 4) imputed company tax legal responsibility, 5) employer-sponsored medical health insurance and different fringe advantages, 6) taxpayers’ imputed contributions to defined-contribution pension plans. Market earnings ranges are adjusted for the variety of exemptions reported on every return to make tax models extra comparable. After-tax earnings is market earnings much less: particular person earnings taxA person earnings tax (or private earnings tax) is levied on the wages, salaries, investments, or different types of earnings a person or family earns. The U.S. imposes a progressive earnings tax the place charges enhance with earnings. The Federal Revenue Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years previous, particular person earnings taxes are the most important supply, company earnings taxA company earnings tax (CIT) is levied by federal and state governments on enterprise income. Many corporations usually are not topic to the CIT as a result of they’re taxed as pass-through companies, with earnings reportable beneath the person earnings tax., payroll taxes, property and reward taxA present tax is a tax on the switch of property by a residing particular person, with out fee or a helpful alternate in return. The donor, not the recipient of the reward, is usually accountable for the tax., customs duties, and excise taxes. The 2026 earnings break factors by percentile are: 20%-$17,735; 40%-$38,572; 60%-$73,905; 80%-$130,661; 90%-$188,849; 95%-$266,968; 99%-$611,194. Tax models with destructive market earnings and non-filers are excluded from the percentile teams however included within the totals.

Supply: Tax Basis Basic Equilibrium Mannequin, September 2025

Conclusion

Enhancing neutrality is a crucial purpose of tax coverage, and limiting the exclusion for ESI would supply extra impartial therapy of main types of compensation, decreasing distortions within the labor market and healthcare market. Capping the exclusion on the 80th or 90th percentile of premiums, as proposed right here, would scale back distortions and lift substantial quantities of income, primarily impacting excessive earners with exceptionally beneficiant ESI advantages.

As a result of the proposals increase marginal tax charges on compensation, we discover small destructive impacts on GDP. Nevertheless, to the extent the proposals lead employers to shift towards different types of compensation, similar to money, which are most well-liked by staff, the financial hurt can be lowered. To the extent the proposals cut back demand for healthcare and enhance effectivity within the healthcare market, they could cut back healthcare costs usually, broadly benefiting shoppers of healthcare (employer-sponsored or in any other case).

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

[1] Robert King and Benjamin Guggenheim, “Home Republicans Launch Invoice to Lengthen Well being Subsidies Previous Midterms,” Politico, Sep. 4, 2025, https://www.politico.com/information/2025/09/04/aca-enhanced-tax-credits-extension-00544565.

[2] Congressional Funds Workplace, “The Estimated Results of Enacting Chosen Well being Protection Insurance policies on the Federal Funds and on the Variety of Individuals With Well being Insurance coverage,” Sep. 18, 2025, https://www.cbo.gov/system/information/2025-09/61734-Well being.pdf.

[3] US Treasury Division, “Tax Expenditures Fiscal Yr 2026,” Nov. 27, 2024, https://house.treasury.gov/system/information/131/Tax-Expenditures-FY2026.pdf; Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for Fiscal Years 2024-2028,” Dec. 11, 2024, https://www.jct.gov/publications/2024/jcx-48-24/.

[4] William McBride, Erica York, Alex Durante, and Garrett Watson, “The Unsustainable US Debt Course and Impacts of Potential Tax Modifications, “ Tax Basis, Jan. 14, 2025, https://taxfoundation.org/analysis/all/federal/us-debt-budget-taxes-spending-social-security-medicare/; PTCs and different main healthcare packages are about 28 p.c of the federal finances this 12 months and projected to develop to greater than 30 p.c over the subsequent 10 years. Main healthcare packages are projected to develop about 5.6 p.c yearly over the subsequent decade, versus about 3.8 p.c progress for nominal GDP. See: Congressional Funds Workplace, “The Funds and Financial Outlook: 2025 to 2035,” Jan. 17, 2025, https://www.cbo.gov/publication/60870.

[5] Maria Polyakova and Stephen P. Ryan, “Subsidy Focusing on with Market Energy,” NBER working paper 26367, Aug. 2021, https://www.nber.org/papers/w26367; Marika Cabral, Michael Geruso, and Neale Mahoney, “Do Bigger Well being Insurance coverage Subsidies Profit Sufferers or Producers? Proof from Medicare Benefit,” American Financial Evaluate 108:8 (August 2018), https://www.aeaweb.org/articles?id=10.1257/aer.20151362; Cynthia Cox, Jared Ortaliza, Emma Wagner, and Krutika Amin, “Well being Care Prices and Affordability,” KFF, Might 28, 2024, https://www.kff.org/health-costs/health-policy-101-health-care-costs-and-affordability/?entry=table-of-contents-introduction; Jared Ortaliza, Anna Wire, Matt McGrough, Justin Lo, and Cynthia Cox, “Inflation Discount Act Well being Insurance coverage Subsidies: What’s Their Impression and What Would Occur if They Expire?,” KFF, Jul. 26, 2024, https://www.kff.org/affordable-care-act/inflation-reduction-act-health-insurance-subsidies-what-is-their-impact-and-what-would-happen-if-they-expire/; Mark Pauly, Scott Harrington, and Adam Leive, “Sticker Shock in Particular person Insurance coverage beneath Well being Reform,” NBER working paper 20223, June 2014, https://www.nber.org/papers/w20223.

[6] Anna Wilde Mathews, “Well being Insurance coverage Prices for Companies to Rise by Most in 15 Years,” The Wall Avenue Journal, Sep. 10, 2025, https://www.wsj.com/well being/healthcare/health-insurance-costs-rise-6cc1b934.

[7] In line with Treasury Division estimates, after the exclusion for ESI, the most important healthcare tax expenditure is the PTC, adopted by the deductibility of medical bills (costing $243 billion over the subsequent decade), well being financial savings accounts ($181 billion), the deductibility of charitable contributions to well being establishments ($153 billion), and the deductibility of self-employed medical insurance coverage premiums ($143 billion) amongst different smaller tax expenditures. As well as, nonprofit hospitals are exempt from company tax, which, though unaccounted for in official estimates, might cut back federal income by roughly $200 billion or extra over the subsequent decade. See: US Treasury Division, “Tax Expenditures Fiscal Yr 2026,” Nov. 27, 2024, https://house.treasury.gov/system/information/131/Tax-Expenditures-FY2026.pdf; Scott Hodge, “Reining in America’s $3.3 Trillion Tax-Exempt Financial system,” Jun. 18, 2024, https://taxfoundation.org/analysis/all/federal/501c3-nonprofit-organization-tax-exempt/; Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for Fiscal Years 2024-2028,” Dec. 11, 2024, https://www.jct.gov/publications/2024/jcx-48-24/.

[8] Michael Cannon, “Tackling America’s Elementary Well being Care Downside,” Cato Institute, July/August 2022, https://www.cato.org/policy-report/july/august-2022/tackling-americas-fundamental-health-care-problem; Congressional Funds Workplace, “Cut back Tax Subsidies for Employment-Based mostly Well being Insurance coverage,” Dec. 7, 2022, https://www.cbo.gov/budget-options/58627; David Powell, “The Distortionary Results of the Well being Insurance coverage Tax Exclusion,” American Journal of Well being Economics 5:4 (Fall 2019), https://www.journals.uchicago.edu/doi/10.1162/ajhe_a_00126.

[9] KFF, “2024 Employer Well being Advantages Survey,” Oct. 9, 2024, https://www.kff.org/health-costs/2024-employer-health-benefits-survey/.

[10] Well being financial savings accounts can now be used to pay charges for direct major care preparations, as a consequence of adjustments made as a part of OBBBA, and can be utilized to pay for different out-of-pocket healthcare bills, topic to annual contribution limits and different constraints. The tax code supplies different restricted preferences for sure forms of out-of-pocket healthcare bills, similar to deductibility of medical bills above a sure threshold. See: David Kopans, Erin Sweeney, and Lindsey LePlae, “Paying for Direct Main Care Preparations with HSAs is Now Permitted – with Caveats,” DLA Piper, Aug. 6, 2025, https://www.dlapiper.com/en-us/insights/publications/2025/08/paying-for-direct-primary-care-arrangements-with-hsa;

Michael Cannon, “Tackling America’s Elementary Well being Care Downside,” Cato Institute, July/August 2022, https://www.cato.org/policy-report/july/august-2022/tackling-americas-fundamental-health-care-problem.

[11] US Bureau of Labor Statistics (BLS), “Medical Care Premiums within the United States, March 2023,” https://www.bls.gov/ebs/factsheets/medical-care-premiums-in-the-united-states.htm; BLS, “Desk 3. Medical Plans: Share of Premiums Paid by Employer and Worker for Single Protection,” https://www.bls.gov/information.launch/ebs2.t03.htm; BLS, “Desk 4. Medical Plans: Share of Premiums Paid by Employer and Worker for Household Protection,” https://www.bls.gov/information.launch/ebs2.t04.htm.

[12] For an outline of Tax Basis’s mannequin, see: Huaqun Li, Garrett Watson, and Erica York, “Overview of the Tax Basis’s Basic Equilibrium Mannequin,” Tax Basis, Mar. 5, 2025, https://taxfoundation.org/analysis/all/federal/general-equilibrium-model/. We assume ESI advantages develop on the identical price as wages and salaries (as do the 80th and 90th percentile of premiums), which is a quicker progress price than the CBO initiatives for the core private consumption expenditures (PCE) worth index, used to cap the ESI exclusion in Choices 2 and 4. We don’t assume employers shift pay packages towards taxable wages and salaries in response to the proposals, and thus would possibly understate further payroll tax income that would end result. Our mannequin doesn’t seize the micro-level heterogeneity of ESI advantages at every earnings degree, and thus would possibly understate the income results of capping the ESI exclusion. Our mannequin doesn’t seize tax avoidance conduct that’s explicit to ESI and different untaxed fringe advantages. To the diploma that employers substitute different untaxed fringe advantages for ESI, our mannequin will overstate the income results of limiting the ESI exclusion. Moreover, our mannequin doesn’t explicitly seize the interplay results with PTCs, which can overstate the income results of limiting the ESI exclusion. On web, these results could also be largely offsetting for income estimating functions.

[13] All 4 coverage choices cut back GDP over the long term by a small quantity (lower than 0.05 p.c). We assume staff are detached between a greenback of money compensation and a greenback of ESI, which overstates the financial hurt to the extent staff favor money and employers accommodate this choice by growing money compensation as a share of whole compensation.

Share this text