{kind=link}

Key Findings

- On common, within the Organisation for Co-operation and Growth (OECD) and European Union, long-term capital positive factors from the sale of shares are taxed at a prime fee of 18.19 %, and dividends are taxed at a prime fee of twenty-two.87 %.

- Funding earnings is normally taxed twice, first on the company stage after which once more on the shareholder stage (on dividends and capital positive factors), producing a median built-in taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of normal authorities companies, items, and actions. fee on distributed company earnings of 40.86 % for dividends and 37.37 % for capital positive factors in OECD and EU international locations.

- The portion of after-tax earnings that staff put aside for financial savings and future consumption is commonly taxed twice, making a bias towards saving. Ideally, staff ought to solely be taxed on their earnings as soon as, both when earned or when withdrawn for spending, to keep away from compounding disincentives to each labor earnings and financial savings.

- To encourage long-term retirement saving, international locations generally present tax preferences for personal retirement accounts. These normally present a tax exemptionA tax exemption excludes sure earnings, income, and even taxpayers from tax altogether. For instance, nonprofits that fulfill sure necessities are granted tax-exempt standing by the Inside Income Service (IRS), stopping them from having to pay earnings tax. for the preliminary principal funding quantity and/or for the funding returns.

- Financial savings accounts that exempt contributions and returns on funding whereas deferring taxation till withdrawal enable policymakers to widen the eligibility to financial savings autos which will embody hybrid earnings streams, similar to start-ups and actively managed portfolios, diversifying family financial savings and eradicating tax penalties on these investments.

- Tax-preferred personal retirement accounts usually have complicated guidelines and limitations. Common financial savings accounts may very well be a less complicated various—or addition—to many international locations’ present programs of personal retirement financial savings accounts.

Introduction

Lengthy-term financial savings and funding play an vital position in people’ monetary stability and the financial system total. Taxes usually affect whether or not, and the way a lot, people set earnings apart for financial savings and investments. Varied elements decide the quantity of taxes one is required to pay on these financial savings and investments, similar to the kind of asset, the person’s earnings stage, the interval over which the asset has been held, and the financial savings goal.

Whereas long-term financial savings and funding can are available many varieties, this paper usually focuses on the tax therapy of shares in publicly traded corporations.[1] Every nation approaches the taxation of shares in another way, however most international locations levy some type of capital positive factors and dividend taxes on people’ earnings from proudly owning shares. Capital positive factors and dividend taxes are levied after company earnings taxes are paid on income on the entity stage, and thus represent a second layer of taxation.

Nevertheless, lawmakers have acknowledged the necessity to incentivize long-term financial savings—significantly with regards to personal retirement financial savings. Thus, international locations generally present tax preferences for people who save and make investments inside devoted personal retirement accounts—normally by exempting the preliminary principal funding quantity or the funding returns from tax. These tax-preferred personal retirement accounts play a major position when an financial system’s whole financial savings and investments. For instance, within the United States, about 30 % of whole US fairness is held in tax-preferred retirement accounts. Foreigners maintain 40 % of US fairness, and solely about 25 % is estimated to be in taxable accounts.[2]

This paper will first clarify how dividends and capital positive factors taxes affect one’s funding earnings, and the way tax-preferred personal retirement accounts decrease the tax burden on such investments. Second, a survey of capital positive factors taxes, dividends taxes, and the tax therapy of personal retirement accounts exhibits how the taxation of financial savings and investments differs throughout international locations. Lastly, we briefly spotlight the significance of simplicity with regards to retirement financial savings and clarify how common financial savings accounts may very well be a step in that path.

Understanding the Tax Remedy of Financial savings and Funding

Financial savings and funding can are available many varieties. This paper focuses on saving within the type of proudly owning shares in publicly traded corporations. Shares present two methods for traders to get earnings.

The primary is by shopping for a inventory and promoting it later at the next value. This leads to a capital achieve. An investor who buys a inventory for EUR 100 and later sells it for EUR 110 has earned a EUR 10 capital achieve.

The second solution to get earnings from shares is to buy shares in corporations that recurrently pay out dividends to shareholders. An organization that pays out annual dividends at EUR 1 per share would offer a person who owns 10 shares of that firm with EUR 10 every year.

Two sorts of taxes apply to these totally different earnings: capital positive factors taxes and dividends taxes, respectively. A capital positive factors taxA capital positive factors tax is levied on the revenue constituted of promoting an asset and is commonly along with company earnings taxes, often leading to double taxation. These taxes create a bias towards saving, resulting in a decrease stage of nationwide earnings by encouraging current consumption over funding. applies to the EUR 10 in positive factors the investor made, and a dividends tax applies to the EUR 10 in dividends that had been paid out.

Each taxes create a burden on financial savings. If a person has a financial savings objective and desires a 5 % whole return on funding to succeed in that objective, a capital positive factors tax would require that particular person’s precise return on funding to be larger than 5 % to fulfill the objective. If the capital positive factors tax is 20 %, then the person’s before-tax return on funding would should be 6.25 %.

Equally, taxes on dividends cut back earnings for traders.

For staff who make investments after paying particular person earnings taxes, capital positive factors and dividend taxes add one other layer of tax on the portion of their after-tax earnings put aside for future use slightly than fast consumption, making a bias towards saving. Ideally, staff ought to solely be taxed on their earnings as soon as, both when earned or when withdrawn for spending, to keep away from compounding disincentives to each labor earnings and financial savings.

In terms of retirement financial savings, governments recurrently present tax exemptions for both the wages used to contribute to a financial savings account or the positive factors from a financial savings account.

Desk 1 exhibits that there are 4 primary tax regimes for traders. The 2 dimensions of taxation concern the principal, or the preliminary deposit, and the returns to funding. Techniques usually fall into one of many 4 classes within the desk.

Some investments are taxed each on the preliminary principal and on the return. These embody investments in brokerage accounts. For the sort of funding, there may be normally no exemption or deduction for the preliminary price of buying shares, and the earnings from the funding (whether or not a capital achieve or a dividend) is taxable.

Personal retirement financial savings, however, normally face an exemption from tax on the preliminary principal funding quantity or on the returns to that funding. Within the US, that is referred to both as “conventional” or “Roth” therapy for particular person retirement preparations (IRAs). With conventional therapy, there is no such thing as a tax on the preliminary funding principal, however there’s a tax on the full quantity (principal plus positive factors) upon withdrawal. Roth therapy consists of taxable principal investments and no tax upon withdrawal.

Within the US, well being financial savings accounts present an exemption from tax each on the principal and the returns upon contribution in addition to withdrawal, representing the fourth kind of tax therapy on funding the place neither the principal nor the returns are taxed at any level.

Desk 1. 4 Tax Regimes for U.S. Traders

The A number of Layers of Taxes on Funding

Particular person traders who save exterior of a retirement account will face a number of layers of taxation. If an investor buys inventory in a company, that firm will owe the company earnings taxA company earnings tax (CIT) is levied by federal and state governments on enterprise income. Many corporations should not topic to the CIT as a result of they’re taxed as pass-through companies, with earnings reportable beneath the person earnings tax., and the investor will owe dividends tax on any dividend earnings or capital positive factors tax if the investor sells the inventory at the next value.

The next instance exhibits how EUR 48.51 in tax would apply to EUR 100 in company income when accounting for each company taxes and taxes on dividends. First, the company earns EUR 100 in income. If it’s a German firm and faces the company earnings tax fee, it could pay EUR 30.06 in company taxes on that earnings.

This leaves EUR 69.94 accessible for a dividend. The shareholder would owe a further EUR 18.45 in dividend taxes.

From the EUR 100 in income, simply EUR €51.49 in after-tax income stay for the shareholder within the type of a dividend.

Equally, the capital positive factors tax is a further layer on company earnings.

Nevertheless, some international locations have built-in tax programs, which means that company earnings is simply topic to a single layer of taxation.

Beneath (full) imputation programs, as in Australia and Malta, if an organization pays company taxes on its income, an investor can declare a (partial or full) credit score towards taxes on capital positive factors and dividends. This leads to traders solely paying taxes to the extent that capital positive factors or dividends tax liabilities are greater than the (partial or full) credit score for company taxes paid.

Tax Remedy of Personal Retirement Accounts

Most people in OECD international locations can make the most of a tax-preferred financial savings account to construct up particular person retirement financial savings—usually along with public pensions. Two normal types of tax therapy are the commonest and fall into the classes mentioned earlier.

One strategy permits people to contribute to retirement accounts utilizing cash that has already been taxed as wages. Nevertheless, returns on the funding and withdrawals from the account are tax-exempt. That is what known as a taxed, exempt, exempt (or TEE) strategy, referring to the coverage’s therapy of contributions, returns on funding, and withdrawals from a retirement account. Within the US, that is known as the “Roth” therapy for retirement financial savings.[3]

The opposite strategy permits people to contribute to accounts with both pre-tax earnings or present a tax deductionA tax deduction permits taxpayers to subtract sure deductible bills and different gadgets to cut back how a lot of their earnings is taxed, which reduces how a lot tax they owe. For people, some deductions can be found to all taxpayers, whereas others are reserved just for taxpayers who itemize. For companies, most enterprise bills are absolutely and instantly deductible within the 12 months they happen, however ot for contributions. Returns on the funding don’t face tax, however withdrawals from the account (principal plus earnings) are taxed. That is known as an exempt, exempt, taxed (EET) strategy. Within the US, “conventional” retirement autos observe this strategy.

Determine 2 compares how these two preferences for retirement financial savings affect an investor and compares them to an investor who’s saving exterior a retirement account.

In every state of affairs, EUR 1,000 is the preliminary deposit. Within the first and second eventualities, a 20 % tax applies to that preliminary deposit. Consider this as a tax on the wages which can be getting used to fund the funding.

So, proper off the bat, Eventualities 1 and a pair of have EUR 800 for investing. State of affairs 3 doesn’t embody a tax on wages used for contributing to a retirement account and permits the total EUR 1,000 to be invested as a result of it’s an EET strategy (which means that contributions are tax-exempt).

In every state of affairs, the investor leaves the funds of their funding account for 20 years and earns a 5 % annual return. On the finish of this era, each Eventualities 1 and a pair of have the identical sum of money of their funding account, EUR 2,122.64. As a result of State of affairs 3 began off with a bigger preliminary deposit, that state of affairs has EUR 2,653.30 of their funding account.

Now, when funds are withdrawn, taxes apply each to quantities withdrawn in State of affairs 1 and State of affairs 3, however not State of affairs 2. State of affairs 2 operates as a TEE account, so withdrawals are exempt from tax.

Upon withdrawal, State of affairs 1 pays a 20 % tax on the positive factors (last quantity minus the EUR 800 preliminary funding). This leads to last, after-tax earnings of EUR 1,858.11. State of affairs 2 doesn’t owe taxes on positive factors or principal upon withdrawal; the ultimate earnings are EUR 2,122.64. State of affairs 3 owes a 20 % tax on the withdrawn quantity, which incorporates each the principal and positive factors—so the full withdrawal quantity—and has last earnings of EUR 2,122.64, the identical as in State of affairs 2.

This instance exhibits two issues. First, as a result of absolutely taxable accounts have a couple of layer of taxes, they end in decrease after-tax funding earnings. Second, if the tax fee on the principal in State of affairs 2 and the tax fee on principal and achieve upon withdrawal in State of affairs 3 are the identical, then the earnings from each will probably be equal. The tax charges on deposit and withdrawal could not all the time be the identical, nonetheless. Many tax programs have a progressive fee construction for wages, which can imply a person will probably be in a unique tax bracket when the funding is made than once they have retired and start making withdrawals.

If a person faces a 30 % tax fee once they make investments, however a 15 % tax fee once they withdraw their earnings, it could be advantageous to make use of an funding account as in State of affairs 3.

Extra usually, EET regimes—the place contributions and returns on funding are tax-exempt and withdrawals are taxed at strange charges—are effectively suited to accommodate a wider vary of financial savings and funding autos, together with hybrid earnings streams similar to start-ups and actively managed portfolios. By deferring taxation till withdrawal and taxing whole distributions (principal plus positive factors) at strange charges, an EET design captures extra returns from sheer luck or entrepreneurial effort with out creating new distortions in financial savings or consumption selections.[4]

Increasing permitted holdings in particular person financial savings accounts to incorporate these investments would take away the tax penalty they face in any other case and permit people to carry extra diversified portfolios throughout asset courses. For policymakers looking for to strengthen the monetary ecosystem for entrepreneurial investments and actively managed portfolios, an EET framework for particular person financial savings accounts presents a possibility to combine these investments into family financial savings whereas eliminating disincentives to saving and funding.

Different Varieties of Tax-Most popular Financial savings Accounts

Along with retirement accounts, some international locations supply tax preferences for different financial savings functions. Examples embody financial savings for future schooling and health-related prices.

For instance, the US presents so-called “certified tuition plans” for future schooling prices, also called “529 plans.”[5] Relying on the US state and kind of 529 plan, savers might be able to deduct contributions from state earnings taxes or obtain matching grants; positive factors should not topic to tax; and withdrawals are exempt from state and federal earnings taxes. Equally, Canada presents a registered schooling financial savings plan (RESP), which exempts earnings as they accrue, and a authorities financial savings bonus (earnings and bonus are taxed on the pupil’s tax fee upon withdrawal).

In the US, there may be additionally a well being financial savings account (HSA), which can be utilized to pay for certified medical bills. As proven in Desk 1, contributions are constituted of pre-tax earnings, positive factors are tax-exempt, and withdrawals should not taxed both. The 2025 One Huge Stunning Invoice Act provides a brand new kind of TET particular person retirement account, known as “Trump Accounts,” which features a USD 1,000 deposit made by the federal government for sure kids born in 2025 by 2028, permits as much as USD 5,000 of annual after-tax contributions, and permits financial savings to develop tax-deferred.[6]

Survey of Capital Good points Taxes, Dividend Taxes, and Retirement Financial savings in OECD Nations

Whereas most international locations levy some type of tax on financial savings and funding, the tax therapy differs not solely between international locations but in addition between sorts of funding earnings and financial savings functions.

For instance, the typical prime long-term capital positive factors tax fee in OECD and EU international locations is eighteen.19 %, whereas dividends face a median tax fee of twenty-two.87 %. In terms of personal retirement financial savings, the tax therapy in addition to contribution limits additionally range considerably.

Capital Good points Tax Charges

Many international locations tax capital positive factors at numerous charges relying on the holding interval, the person’s earnings stage, and the kind of asset bought.

Recognizing the significance of long-term financial savings, some international locations tax the positive factors from long-term financial savings at a decrease capital positive factors tax fee than these from short-term financial savings. For instance, in Slovenia, capital positive factors on the disposition of immovable property, shares, or different capital participations are taxed at 25 % if held for as much as 5 years, at 20 % if held between 5 and 10 years, at 15 % if held between 10 and 15 years, and at 0 % if held for greater than 15 years.

Whereas some international locations levy flat capital positive factors tax charges no matter a person’s earnings stage, others embody capital positive factors when calculating private earnings taxes—which in most international locations leads to the progressive taxation of capital positive factors. Nonetheless, different international locations have a separate progressive capital positive factors tax construction. Some international locations have an annual exempt quantity for capital positive factors. For instance, within the United Kingdom, the primary GBP 3,000 (USD 3,843) of realized capital positive factors is tax-free. The Czech Republic applies an annual exemption to the primary CZK 40 million (USD 1.7 million) of long-term capital positive factors from the sale of shares.

Many international locations exempt owner-occupied residential property from capital positive factors tax.

Desk 2 exhibits the highest marginal capital positive factors tax charges levied on people within the OECD and choose EU international locations, considering exemptions and surtaxes. If a rustic has a couple of capital positive factors tax fee, the desk exhibits the tax fee making use of to the sale of listed shares with out substantial possession after an prolonged time period.

Denmark levies the very best prime marginal capital positive factors tax on long-held shares within the OECD, at a fee of 42 %. Chile’s prime capital positive factors tax fee is the second highest, at 40 %, adopted by Norway at 37.48 % and the Netherlands at 36 %.

Roughly one-fourth of all international locations analyzed don’t levy capital positive factors taxes on the sale of long-held shares. These are Belgium, Greece, Cyprus, Korea, Luxembourg, Malta, New Zealand, Slovakia, Slovenia, Switzerland, and Turkey.

On common, long-term capital positive factors from the sale of shares are taxed at a prime marginal fee of 18.19 % in OECD and EU international locations.

Desk 2. Capital Good points Tax Charges, as of January 2025

Prime Marginal Capital Good points Tax Charges on People Proudly owning Lengthy-Held Listed Shares with out Substantial Possession (consists of Exemptions and Surtaxes)

| Nation | Prime Marginal Capital Good points Tax Fee | Further Feedback |

|---|---|---|

| Australia (AU) | 23.50% | Capital positive factors are topic to the conventional PIT fee and there’s a 50% exemption if the asset was held for not less than 12 months. |

| Austria (AT) | 27.50% | – |

| Belgium (BE) | 0.00% | Capital positive factors are solely taxed if they’re considered skilled earnings. |

| Bulgaria (BG) | 10.00% | Capital positive factors are topic to flat PIT fee at 10%. |

| Canada (CA) | 26.75% | Capital positive factors are topic to the conventional PIT fee however solely 50% of the positive factors are included as taxable earnings. |

| Chile (CL) | 40.00% | Solely sure positive factors on the sale of traded shares of Chilean companies are tax-exempt. |

| Colombia (CO) | 15.00% | The 15% fee applies for property that had been held for 2 or extra years, in any other case capital positive factors are taxed as strange capital earnings at 39%. |

| Costa Rica (CR) | 15.00% | Capital positive factors are topic to a 15% tax. |

| Croatia (HR) | 12.00% | – |

| Cyprus (CY) | 0.00% | Shares listed on any recognised inventory alternate are excluded from CGT. |

| Czech Republic (CZ) | 23.00% | Capital positive factors included in PIT however exempt if shares of a joint inventory firm had been held for not less than three years (5 years if restricted legal responsibility firm). As of 2025, this exemption is proscribed by an annual cap for gross proceeds (i.e. gross sales value of the securities + different shares) of CZK 40 million; proceeds above the cap will probably be topic to plain progressive taxation. |

| Denmark (DK) | 42.00% | Capital positive factors are topic to the conventional PIT fee. |

| Estonia (EE) | 22.00% | Capital positive factors are topic to PIT. |

| Finland (FI) | 34.00% | – |

| France (FR) | 34.00% | Flat 30% tax on capital positive factors, plus 4% for high-income earners. |

| Germany (DE) | 26.38% | Flat 25% tax on capital positive factors, plus a 5.5% solidarity surcharge. |

| Greece (GR) | 0.00% | Capital positive factors tax applies at a 15% fee if a person holds not less than 0.5% of the share capital of the listed entity. |

| Hungary (HU) | 15.00% | Capital positive factors are topic to flat PIT fee at 15%. |

| Iceland (IS) | 22.00% | – |

| Eire (IE) | 33.00% | – |

| Israel (IL) | 30.00% | Flat 25% tax on capital positive factors, plus further 2% and three% tax for high-income earners. |

| Italy (IT) | 26.00% | – |

| Japan (JP) | 20.32% | Flat 20.315% tax on capital positive factors (15.315% nationwide tax and 5% native inhabitant’s tax) |

| Korea (KR) | 0.00% | Capital positive factors on listed shares owned by non-large shareholders should not taxed. Different sorts of capital positive factors are taxed. |

| Latvia (LV) | 28.50% | Flat 25.5% on capital positive factors, plus 3% for high-income earners. |

| Lithuania (LT) | 20.00% | Capital positive factors are topic to PIT, with a prime fee of 20%. |

| Luxembourg (LU) | 0.00% | Capital positive factors are tax-exempt if a movable asset (similar to shares) was held for not less than six months and is owned by a non-large shareholder. Taxed at progressive charges if held |

| Malta (MT) | 0.00% | Transfers of shares listed on acknowledged inventory exchanges are normally exempt from PIT. |

| Mexico (MX) | 10.00% | – |

| Netherlands (NL) | 36.00% | Internet asset worth is taxed at a flat fee of 36% on a deemed annual return (the deemed annual return varies by the full worth of property owned). |

| New Zealand (NZ) | 0.00% | Doesn’t have a complete capital positive factors tax. |

| Norway (NO) | 37.80% | Capital positive factors are taxed at a 22% fee. A multiplier of 1.72 earlier than taxation applies to positive factors from the sale of shares. |

| Poland (PL) | 19.00% | – |

| Portugal (PT) | 19.60% | PIT applies if the property had been held for lower than one 12 months. In any other case, a flat capital positive factors tax fee of 28 % from the sale of shares and different securities. Capital positive factors earnings is 10 % tax-free for holding intervals between 2 and 5 years, 20 % for five to eight years, and 30 % after 8 years. |

| Romania (RO) | 1.00% | Good points derived from the switch of securities and from operations with spinoff monetary devices by intermediaries are taxed at 3 % for holding intervals lower than 356 days and at 1 % thereafter. |

| Slovakia (SK) | 0.00% | Shares are exempt from capital positive factors tax in the event that they had been held for a couple of 12 months and should not a part of the enterprise property of the taxpayer. |

| Slovenia (SI) | 0.00% | Capital positive factors fee of 0% if the asset was held for greater than 15 years (fee as much as 25% for intervals lower than 15 years). |

| Spain (ES) | 30.00% | – |

| Sweden (SE) | 30.00% | – |

| Switzerland (CH) | 0.00% | Capital positive factors on movable property similar to shares are usually tax-exempt. |

| Turkey (TR) | 0.00% | Shares which can be traded on the inventory alternate and which have been held for not less than one 12 months are tax-exempt (two years for joint inventory corporations). |

| United Kingdom (GB) | 24.00% | – |

| United States (US) | 28.74% | 28.74% applies if the asset was held for a couple of 12 months; consists of federal and state taxes on capital positive factors, in addition to the three.8% web funding earnings tax (NIIT) for high-income earners. |

Be aware: “PIT” refers to private earnings tax.

Supply: Bloomberg Tax, “Nation Guides,” https://bloomberglaw.com/product/tax/toc_view_menu/3380/; and PwC, “Worldwide Tax Summaries On-line,” https://taxsummaries.pwc.com/.

Dividend Tax Charges

Whereas some international locations tax dividends on the identical fee as capital positive factors, different international locations differentiate between the 2 types of earnings. As well as, as beforehand talked about, a number of international locations have built-in their taxation of company income and dividends paid. Desk 3 exhibits the highest marginal dividends tax charges levied in every nation, considering credit and surtaxes.

As with capital positive factors taxes, some international locations levy private earnings taxes on dividend earnings, whereas others levy a flat, separate dividends tax. Exemption thresholds are additionally comparatively frequent. For instance, the UK gives a GBP 5,000 (USD 6,840) dividend allowance, above which a progressive dividend tax is levied.

On common, the OECD and choose EU international locations levy a prime marginal tax fee of twenty-two.87 % on dividend earnings. Nevertheless, as with capital positive factors, there may be vital variation. Eire’s prime dividend tax fee is the very best, at 51 %.

Estonia and Latvia are the one OECD international locations that don’t levy a tax on dividend earnings. This is because of their cash-flow-based company tax system. As a substitute of levying a dividend tax, Estonia and Latvia impose a company earnings tax of as much as 22 % when a enterprise distributes its income to shareholders. Equally, Malta’s dividend imputation system successfully reduces its tax on dividends to zero resulting from full company integration, because the 35 % company fee exceeds the nation’s prime private earnings tax fee.

Of the OECD and EU international locations with a tax on dividend earnings, Bulgaria’s and Greece’s are the bottom, at 5 %. Second and third are Slovakia and Romania, at 7 % and 10 %, respectively.

Desk 3. Dividends Tax Charges within the OECD and EU Nations, 2025

Prime Marginal Dividends Tax Charges on People (Consists of Credit and Surtaxes)

| Nation | Prime Marginal Dividends Tax Charges |

|---|---|

| Australia (AU) | 24.29% |

| Austria (AT) | 27.50% |

| Belgium (BE) | 30.00% |

| Bulgaria (BG) | 5.00% |

| Canada (CA) | 39.34% |

| Chile (CL) | 23.90% |

| Colombia (CO) | 20.00% |

| Costa Rica (CR) | 15.00% |

| Croatia (HR) | 12.00% |

| Cyprus (CY) | 17.00% |

| Czech Republic (CZ) | 23.00% |

| Denmark (DK) | 42.00% |

| Estonia (EE) | 0.00% |

| Finland (FI) | 28.90% |

| France (FR) | 34.00% |

| Germany (DE) | 26.38% |

| Greece (GR) | 5.00% |

| Hungary (HU) | 15.00% |

| Iceland (IS) | 22.00% |

| Eire (IE) | 51.00% |

| Israel (IL) | 35.00% |

| Italy (IT) | 26.00% |

| Japan (JP) | 20.32% |

| Korea (KR) | 44.45% |

| Latvia (LV) | 0.00% |

| Lithuania (LT) | 15.00% |

| Luxembourg (LU) | 21.00% |

| Malta (MT) | 0.00% |

| Mexico (MX) | 17.14% |

| Netherlands (NL) | 31.00% |

| New Zealand (NZ) | 15.28% |

| Norway (NO) | 37.84% |

| Poland (PL) | 19.00% |

| Portugal (PT) | 28.00% |

| Romania (RO) | 10.00% |

| Slovakia (SK) | 7.00% |

| Slovenia (SI) | 25.00% |

| Spain (ES) | 30.00% |

| Sweden (SE) | 30.00% |

| Switzerland (CH) | 22.16% |

| Turkey (TR) | 20.00% |

| United Kingdom (GB) | 39.35% |

| United States (US) | 28.67% |

Be aware: All sorts of reliefs and gross-up provisions on the shareholder stage are taken under consideration.

Sources: OECD Information Explorer, “Mixed (company and shareholder) statutory tax charges on dividend earnings – Internet private tax,” up to date Apr. 24, 2025, https://data-explorer.oecd.org/ and PwC, “Worldwide Tax Summaries.”

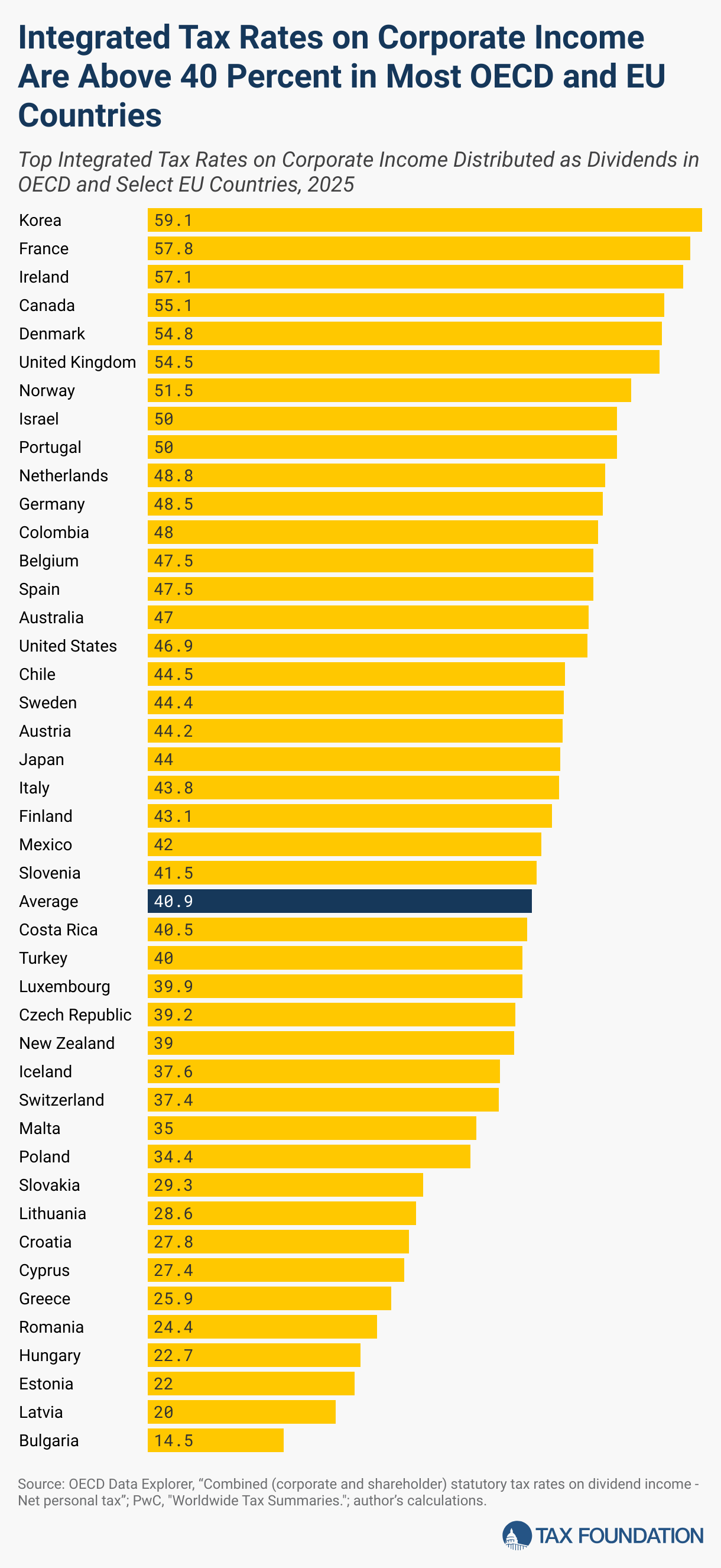

Built-in Charges

Most international locations double tax company earnings by taxing it on the entity and on the shareholder ranges. On common, OECD and choose EU international locations tax company earnings distributed as dividends at a fee of 40.86 % and capital positive factors derived from company earnings at 37.37 %.

For capital positive factors, France (57.85 %), Chile (56.2 %), Denmark (54.76 %), and the Netherlands (52.51 %) have the very best built-in charges within the OECD, whereas Cyprus (12.5 %), Bulgaria (19 %), Switzerland (19.61 %), and Slovenia (22 %) levy the bottom charges. A number of international locations—particularly Belgium, Cyprus, Greece, Luxembourg, Malta, New Zealand, Slovakia, Slovenia, South Korea, Switzerland, and Turkey—don’t levy capital positive factors taxes on long-term capital positive factors, making the company tax the one layer of tax on company earnings realized as long-term capital positive factors.

For dividends, South Korea’s prime built-in tax fee of 59.12 % is the very best amongst OECD and EU international locations, adopted by France (57.85 %), Eire (57.13 %), and Canada (55.10 %). Bulgaria (14.5 %), Latvia (20 %), Estonia (22 %), Hungary (22.65 %), and Romania (24.40 %) levy the bottom charges. Estonia and Latvia’s dividend exemption system implies that the company earnings tax is the one layer of taxation on company earnings distributed as dividends.

Tax Remedy of Retirement Financial savings within the OECD

Along with common pension programs, most OECD international locations present tax preferences for personal retirement financial savings. As defined above, the commonest tax therapy of retirement financial savings accounts is TEE (contributions are taxed, however positive factors are tax-exempt and there’s no tax upon withdrawal) and EET (contributions and positive factors are tax-exempt, however withdrawals—principal plus positive factors—are taxed).

OECD and EU international locations usually restrict the quantity of financial savings one can place in tax-preferred retirement accounts. That is accomplished by annual contribution caps. For instance, in Spain, whole employer and worker contributions made to private and occupational pension plans are restricted to EUR 8,500 (USD 9,197 per 12 months). Australia and Eire are the one two OECD international locations that even have a lifetime contribution restrict for tax-preferred retirement financial savings accounts, at AUD 1.9 million (USD 1.25 million) and AUD 2 million (USD 2.16 million), respectively. Australia’s lifetime contribution restrict solely applies to its EET system, whereas lifetime TTE contributions are limitless.

Some international locations impose penalty charges on withdrawals made earlier than a sure age is reached. For instance, in the US, early withdrawal from an IRA previous to age 59½ is topic to being included in gross earningsFor people, gross earnings is the full of all earnings obtained from any supply earlier than taxes or deductions. It consists of wages, salaries, ideas, curiosity, dividends, capital positive factors, rental earnings, alimony, pensions, and different types of earnings.

For companies, gross earnings (or gross revenue) is the sum of whole receipts or gross sales minus the price of items bought (COGS)—the direct prices of manufacturing items plus a ten % further tax penalty.

Particulars on the tax therapy of personal retirement financial savings in every OECD nation could be present in Appendix Desk 2.

Simplifying the Tax Remedy for Financial savings and Investments

Lengthy-term financial savings and investments play an vital position in people’ monetary stability and the financial system total. Lawmakers have acknowledged the necessity to incentivize saving by tax- and non-tax-related insurance policies. Nevertheless, in lots of instances, tax-preferred financial savings accounts include a myriad of complicated guidelines and limitations, which finally could deter people from opening such tax-preferred financial savings accounts and probably decrease the quantity of whole financial savings.

Common financial savings accounts can considerably simplify a rustic’s tax-preferred financial savings system. These accounts should not restricted to a sure kind of financial savings (e.g., retirement financial savings) and don’t have any earnings limitations or withdrawal penalties. Returns to the account wouldn’t be topic to tax, mirroring the tax therapy of most tax-preferred personal retirement financial savings accounts within the OECD. Annual contribution limits may very well be set to make sure that the tax advantages are capped at a sure stage.[7]

Since 2009, Canada has had a sort of common financial savings account—the tax-free financial savings account (TFSA). The annual contribution restrict in 2024 is CAD 7,000 (USD 5,109). Contributions are made with after-tax {dollars}, earnings develop tax-free, and withdrawals could be made for any cause with out triggering further taxes or penalties. If somebody makes lower than the utmost contribution one 12 months, the remaining contribution eligibility is added to the subsequent 12 months’s most contribution.[8] These options have made TFSAs an simply accessible wet day financial savings car with excessive utilization throughout earnings teams.[9]

The UK has had the same program of particular person financial savings accounts (ISAs) since 1999. ISAs have an annual contribution restrict of GBP 20,000 (USD 25,560). As with TFSAs, contributions are made with after-tax earnings, and earnings develop tax-free; not like TFSAs, nonetheless, the rollover possibility isn’t allowed.[10] Sweden launched its mannequin of particular person retirement financial savings accounts (ISKs) in 2012 with out contribution limits or minimal holding intervals. Contributions are made with after-tax earnings, and withdrawals are tax-free. Nevertheless, an annual tax on the principal applies at 0.888 % in 2025. The primary SEK 150,000 (USD 14,180 held in an ISK is tax-free, rising to SEK 300,000 (USD 28,360) in 2026.

The Canadian, UK, and Swedish fashions are among the many most generally adopted particular person financial savings accounts in worldwide comparability, holding property equal to 18 to 48 % of the international locations’ nationwide GDP and reaching voluntary participation between 21 and 54 % of the inhabitants aged 15 and above.[11]

Some EU and OECD international locations have began to acknowledge these successes and are implementing their very own insurance policies to permit for particular person financial savings accounts. In 2025, Lithuania launched a person financial savings account that permits limitless contributions in after-tax earnings, with earnings rising tax-free till tax on withdrawal.

Poland plans to introduce Private Funding Accounts (OKI), which might let people make investments as much as PLN 100,000 (USD 25,120) with out capital positive factors tax. For investments above that threshold, a low annual tax of 1 % will apply solely to the surplus quantity. As much as PLN 25,000 (USD 6,280) of the tax-free quantity may very well be used for deposits and financial savings bonds; the rest may very well be put in the direction of shares or exchange-traded funds.[12]

US lawmakers have made a number of proposals to introduce a common financial savings account, although none have been enacted.[13] Establishing a common financial savings account in the US that has an annual contribution restrict of USD 2,500 per 12 months, makes use of after-tax contributions, and permits earnings to develop tax-free would scale back federal income by about USD 15.1 billion over the subsequent 10 years. Because of the annual contribution restrict of USD 2,500, the losses in federal tax income could be comparatively small. Nevertheless, it could barely improve the after-tax return to saving, resulting in small will increase in output and after-tax incomes.[14]

Conclusion

Because of the significance of long-term financial savings and funding for people and the financial system total, dividend and capital positive factors taxes needs to be saved at a comparatively low stage—significantly when considering the company taxes paid on the entity stage. On common, in OECD and EU international locations, long-term capital positive factors from the sale of shares with out substantial possession are taxed at a prime fee of 18.19 %, and dividends are taxed at a prime fee of twenty-two.87 %. Nevertheless, since company earnings is taxed twice, on common, OECD and choose EU international locations tax company earnings distributed as dividends at a fee of 40.86 % and capital positive factors derived from company earnings at 37.37 %.

To encourage personal retirement saving, international locations generally present tax-preferred retirement accounts. Nevertheless, in lots of international locations, the system of tax-preferred retirement accounts is complicated, which can deter savers from utilizing such accounts—and probably decrease total financial savings. Canada and the UK have carried out common financial savings accounts, and thus present an instance for the way the system of tax-preferred retirement accounts could be simplified whereas offering extra flexibility for what the funds can be utilized for.[15] Policymakers might simplify the tax system and encourage saving with the objective of constructing monetary safety for low- and middle-income households.

For staff who make investments after paying particular person earnings taxes, capital positive factors and dividend taxes add one other layer of tax on the portion of their after-tax earnings put aside for future use slightly than fast consumption, making a bias towards saving. Ideally, staff ought to solely be taxed on their earnings as soon as, both when earned or when withdrawn for spending, to keep away from compounding disincentives to each labor earnings and financial savings.

An EET tax therapy that permits people to contribute from their pre-tax earnings and defer taxation till withdrawal at strange tax charges is well-suited to retirement and particular person financial savings accounts that embody a broad set of property. The EET design captures extra returns from luck or entrepreneurship with out distorting financial savings and consumption conduct and permits policymakers to develop permitted holdings to a wider vary of property and portfolios whereas defending the broader tax baseThe tax base is the full quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slim tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges. towards erosion dangers.

Policymakers ought to maintain dividend and long-term capital-gains taxes comparatively low after accounting for company taxation, simplify and consolidate tax-preferred retirement accounts, and undertake versatile EET accounts that allow a wider vary of investments.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted specialists delivered straight to your inbox.

Appendix

Appendix Desk 1. Prime Built-in Tax Charges on Company Earnings in OECD and EU Nations, 2025

| Nation | Statutory Company Earnings Tax Fee | Capital Good points | Dividends | ||

|---|---|---|---|---|---|

| Prime Private Capital Good points Tax Fee | Built-in Tax on Company Earnings (Capital Good points) | Prime Private Dividend Tax Fee | Built-in Tax on Company Earnings (Dividends) | ||

| Australia (AU) | 30.00% | 23.50% | 46.45% | 24.29% | 47.00% |

| Austria (AT) | 23.00% | 27.50% | 44.18% | 27.50% | 44.18% |

| Belgium (BE) | 25.00% | 0.00% | 25.00% | 30.00% | 47.50% |

| Bulgaria (BG) | 10.00% | 10.00% | 19.00% | 5.00% | 14.50% |

| Canada (CA) | 25.98% | 26.75% | 45.78% | 39.34% | 55.10% |

| Chile (CL) | 27.00% | 40.00% | 56.20% | 23.90% | 44.45% |

| Colombia (CO) | 35.00% | 15.00% | 44.75% | 20.00% | 48.00% |

| Costa Rica (CR) | 30.00% | 15.00% | 40.50% | 15.00% | 40.50% |

| Croatia (HR) | 18.00% | 12.00% | 27.84% | 12.00% | 27.84% |

| Cyprus (CY) | 12.50% | 0.00% | 12.50% | 17.00% | 27.38% |

| Czech Republic (CZ) | 21.00% | 23.00% | 39.17% | 23.00% | 39.17% |

| Denmark (DK) | 22.00% | 42.00% | 54.76% | 42.00% | 54.76% |

| Estonia (EE) | 22.00% | 22.00% | 39.16% | 0.00% | 22.00% |

| Finland (FI) | 20.00% | 34.00% | 47.20% | 28.90% | 43.12% |

| France (FR) | 36.13% | 34.00% | 57.85% | 34.00% | 57.85% |

| Germany (DE) | 30.06% | 26.38% | 48.51% | 26.38% | 48.51% |

| Greece (GR) | 22.00% | 0.00% | 22.00% | 5.00% | 25.90% |

| Hungary (HU) | 9.00% | 15.00% | 22.65% | 15.00% | 22.65% |

| Iceland (IS) | 20.00% | 22.00% | 37.60% | 22.00% | 37.60% |

| Eire (IE) | 12.50% | 33.00% | 41.38% | 51.00% | 57.13% |

| Israel (IL) | 23.00% | 30.00% | 46.10% | 35.00% | 49.95% |

| Italy (IT) | 27.81% | 26.00% | 46.58% | 26.00% | 43.76% |

| Japan (JP) | 29.74% | 20.32% | 44.01% | 20.32% | 44.02% |

| Korea (KR) | 26.40% | 0.00% | 26.40% | 44.45% | 59.12% |

| Latvia (LV) | 20.00% | 28.50% | 42.80% | 0.00% | 20.00% |

| Lithuania (LT) | 16.00% | 20.00% | 32.80% | 15.00% | 28.60% |

| Luxembourg (LU) | 23.87% | 0.00% | 23.87% | 21.00% | 39.86% |

| Malta (MT) | 35.00% | 0.00% | 35.00% | 0.00% | 35.00% |

| Mexico (MX) | 30.00% | 10.00% | 37.00% | 17.14% | 42.00% |

| Netherlands (NL) (a) | 25.80% | 36.00% | 52.51% | 31.00% | 48.80% |

| New Zealand (NZ) | 28.00% | 0.00% | 28.00% | 15.28% | 39.00% |

| Norway (NO) | 22.00% | 37.84% | 51.52% | 37.84% | 51.52% |

| Poland (PL) | 19.00% | 19.00% | 34.39% | 19.00% | 34.39% |

| Portugal (PT) | 30.50% | 19.60% | 44.12% | 28.00% | 49.96% |

| Romania (RO) | 16.00% | 1.00% | 16.84% | 10.00% | 24.40% |

| Slovakia (SK) | 24.00% | 0.00% | 24.00% | 7.00% | 29.32% |

| Slovenia (SI) | 22.00% | 0.00% | 22.00% | 25.00% | 41.50% |

| Spain (ES) | 25.00% | 30.00% | 47.50% | 30.00% | 47.50% |

| Sweden (SE) | 20.60% | 30.00% | 44.42% | 30.00% | 44.42% |

| Switzerland (CH) | 19.61% | 0.00% | 19.61% | 22.16% | 37.42% |

| Turkey (TR) | 25.00% | 0.00% | 25.00% | 20.00% | 40.00% |

| United Kingdom (GB) | 25.00% | 24.00% | 43.00% | 39.35% | 54.51% |

| United States (US) (b) | 25.57% | 28.87% | 47.06% | 28.67% | 46.91% |

| Common | 23.51% | 18.19% | 37.37% | 22.87% | 40.86% |

Notes:

Built-in tax charges are calculated as follows: (Company Earnings Tax) + [(Distributed Profit – Corporate Income Tax) * Dividends or Capital Gains Tax].

In some international locations, the capital positive factors tax fee varies by the kind of asset bought. The capital positive factors tax fee used on this report is the speed that applies to the sale of listed shares after an prolonged time period. Whereas the built-in tax fee on dividends captures subcentral taxes, this will not be the case for all built-in tax charges on capital positive factors resulting from information availability.

(a) Within the Netherlands, the web asset worth is taxed at a flat fee on a deemed annual return.

(b) The built-in prime tax fee on company earnings distributed as dividends or as capital positive factors consists of each federal and state dividend and capital positive factors taxes.”

Supply: OECD Information Explorer, “Mixed (company and shareholder) statutory tax charges on dividend earnings”, up to date Apr. 24, 2025, https://data-explorer.oecd.org/; PwC, “Fast Charts: Capital positive factors tax (CGT) charges,” https://taxsummaries.pwc.com/quick-charts/capital-gains-tax-cgt-rates; Writer’s calculations.

Appendix Desk 2. Tax Remedy of Funded Personal Retirement Financial savings in OECD and EU Nations, as of July 2024

| Nation | Kind of Fund/Contributions | Contributions | Returns on Investments/Funds Gathered | Withdrawals | Annual Contribution Restrict | Lifetime Contribution Restrict |

|---|---|---|---|---|---|---|

| Australia (AU) | Concessional Contributions | T | T (15%) | E | AUD 30,000 (15% tax fee on contributions as much as cap, particular person’s marginal tax fee for contributions above cap; 30% tax fee on contributions from high-income earners). Unused contribution allowances could also be carried ahead for as much as 5 years. | None (lifetime restrict solely applies to ETT system) |

| Austria (AT) | Pension Firms (Pensionskassen) and Occupational Group Insurance coverage (Betriebliche Kollektivversicherung) | T | E | T | Worker contributions are capped to the sum of annual employer contributions (cap doesn’t apply for first EUR 1,000). | None |

| Belgium (BE) | Occupational Pension Plans | E | E | T | Tax advantages restricted to whole retirement contributions (together with the statutory pension) not exceeding 80% of the final gross annual wage. | None |

| Bulgaria (BG) | All | E | E | E | Worker contributions into voluntary pension funds are tax deductible as much as 10% of the person’s taxable earnings. | None |

| Canada (CA) | All | E | E | T | Tax advantages restricted by numerous caps primarily based on annual earnings (18% of earnings plus greenback quantity caps) and month-to-month contributions (in some instances restricted to CAD 2,000); 1% penalty for month-to-month extra over-contributions can apply. Unused contribution allowances could also be carried ahead for as much as 5 years. | None |

| Chile (CL) | Obligatory Particular person Accounts | E | E | T | 10% of a person’s wage as much as 84.3 UF (UF—Unidad de Fomento—is a price-indexed unit of account). | None |

| Colombia (CO) | All | E | E | E | Voluntary contributions (that are along with necessary contributions) can’t exceed 30% of the annual taxable earnings as much as UVT 3,800 yearly (worth of every tax unit UVT—Unidad de Valor Tributario—is equal to COP 47,065 in 2024); totally different cap applies if particular person makes contribution to personal pension fund that additionally receives his/her necessary contributions. | None |

| Costa Rica (CR) | Obligatory Supplementary Pension (ROP) | T | E | E | Workers’ contributions to the necessary scheme (ROP) should not tax-deductible, whereas employer contributions should not included within the worker’s taxable earnings. | None |

| Croatia (HR) | Obligatory Pension Plans | E | E | T | Contributions into necessary pension funds (5% of wages) are tax exempt. The utmost month-to-month earnings thought of to compute contributions are EUR 9,360 (in 2024). | None |

| Cyprus (CY) | Provident Funds | E | T (3%) | E | Tax-exempt worker contributions are restricted to 10% of worker renumeration. | None |

| Czech Republic (CZ) | Supplementary Plans (Particular person’s Contributions) | T | E | E | Tax advantages capped at CZK 48,000 yearly. | None |

| Denmark (DK) | All Plans Besides “Age Financial savings Plans” | E | T (15.3%) | T | Tax advantages capped at DKK 63,100 (in 2024) for contributions to funds which have programmed withdrawal. | None |

| Estonia (EE) | Obligatory Pension Plan | E | E | T | No cap per se, however fastened contribution charges (worker contributions are set at 2% of the gross wage and authorities matching contributions are set at 4% of the gross wage). | None |

| Finland (FI) | Obligatory Occupational Plans and Voluntary Occupational Group Plans | E | E | T | Tax advantages capped for people on the lesser of 5% of wage or EUR 5,000 per 12 months for voluntary occupational group plans. | None |

| France (FR) | All | T | E | T | Tax advantages capped at 10% of earnings web {of professional} prices of the earlier 12 months, with a most deduction of EUR 35,149. | None |

| Germany (DE) | Pension Funds and Direct Insurance coverage | E | E | T | Tax advantages capped at 8% of the social safety contribution ceiling (SSC ceiling was EUR 90,600 in 2024). | None |

| Greece (GR) | Occupational Insurance coverage Funds and Group Pension Insurance coverage Contracts | E | T (5%) | T | Tax advantages capped at 20% of the worker’s gross earnings from salaried employment. | None |

| Hungary (HU) | All | T | E | E | Complete tax aid (considering all sorts of private pension plans) is capped at HUF 280,000 per 12 months, further caps apply for every plan; tax refund can’t exceed private earnings tax legal responsibility. | None |

| Iceland (IS) | All | E | E | T | Tax aid for workers restricted to 4% of their salaries. | None |

| Eire (IE) | All | E | E | T | Contributions are capped at % of earnings and a worth quantity (each range by age); there may be additionally an higher restrict on the quantity of earnings which can be taken under consideration (EUR 115,000). | Lifetime restrict of EUR 2 million on tax-relieved pension merchandise |

| Israel (IL) | All | T | E | E | Tax advantages capped at 7.5% of the wage (max. of two.5 occasions the nationwide common wage) for employer contributions and worker contributions are capped at 20.5% of twice the nationwide common wage. | None |

| Italy (IT) | All | E | T (0%/12.5%/20%) | T | Contributions (employer and worker) exempt from private earnings tax as much as EUR 5,165 per 12 months. | None |

| Japan (JP) | All | E | E | T | Contributions to outlined profit company pension funds are deductible as much as a yearly restrict of JPY 40,000. | None |

| Korea (KR) | All | T (13.2% or 16.5% credit score relying on earnings) | E | T | Particular person contributions to occupational outlined contribution pension plans can’t exceed KRW 18,000,000 per 12 months. Particular person contributions should not potential in an outlined profit pension plan. | None |

| Latvia (LV) | Obligatory Contributions | E | E | T | The joint restrict for contributions to voluntary pension funds and insurance coverage premiums could not exceed 10% of annual taxable earnings with a cap of EUR 4,000. | None |

| Lithuania (LT) | Pillar Two” Plans | T | E | E | Particular person contributions should equal not less than 3% of gross wage or earnings. The overall quantity of deductible pension contributions, life insurance coverage premiums, and academic bills should not exceed 25% of taxable earnings, with an annual cap of EUR 1,500 per 12 months. | None |

| Luxembourg (LU) | Occupational Plans | T (20%) | E | E | Employer contributions of as much as 20% of worker earnings are taxed at 20% however not taxable for the workers. Worker contributions are tax deductible as much as EUR 1,200 per 12 months. | None |

| Malta (MT) | Occupational Plans | E | E | T | Entitlement to a tax credit score amounting to 25% of the quantity contributed to the pension scheme is capped at an annual tax credit score of EUR 750 per worker (EUR 3,000 in annual contributions). | None |

| Mexico (MX) | Obligatory Contributions | T | E | E | The utmost deductible quantity of voluntary contributions to occupational plans is 12.5% of an worker’s wage. The cap applies collectively to worker and employer contributions. | None |

| Netherlands (NL) | All | E | E | T | The utmost earnings for eligibility within the EET system is EUR 137,800. Above that threshold, a TEE system applies. The utmost contributions to the EET system depend upon age and vary from 3.9% to 27.5% of annual earnings. The utmost contributions to the TEE system depend upon age and vary from 2.3% to 13.9% of annual earnings. | None |

| New Zealand (NZ) | All | T | T (10.5% – 28%) | E | Worker contributions are taxed on the particular person’s marginal earnings tax fee. Employer contributions are taxed at charges starting from 10.5% to 39%. No annual contribution restrict applies. | None |

| Norway (NO) | Occupational Outlined Contribution Plans (Contributions from Employers) | E | E | T | When staff are required to contribute, contributions should not exceed 2% of wage within the municipal and public sector outlined profit plans and 4% of wage or the contribution made by the employer. | None |

| Poland (PL) | OFE Plans | E | E | T | Contributions into OFE plans are tax deductible with no restrict. | None |

| Portugal (PT) | All | E | E | T | Annual employer contributions are topic to a cap of 15% of annual whole prices of wages and salaries (25% if staff should not coated by social safety). Worker contributions to personal pension plans are topic to a 20% cap on deductible contributions and a yearly restrict primarily based on the person’s age. | None |

| Romania (RO) | Obligatory/Voluntary Personal (Pillar Two/Three) | E | E | E | Contributions into necessary personal pension funds are tax deductible. The contribution fee is 4.75% of gross incomes in 2024. Voluntary worker contributions are tax deductible as much as the RON equal of EUR 400 per 12 months. There is no such thing as a deductibility restrict on voluntary employer contributions. | None |

| Slovakia (SK) | Pillar Two” Plans | E | E | E | Employers are required to make annual contributions of 4% of wage in 2024. Obligatory contributions are tax deductible. Workers could make further contributions that aren’t topic to a cap and never tax deductible. | None |

| Slovenia (SI) | All | E | E | T | Employer contributions should not included in worker’s taxable earnings as much as 5.844% of worker’s gross wages. The quantity can’t exceed EUR 2,903.66 (in 2023) per 12 months. | None |

| Spain (ES) | All | E | E | T | The final restrict on particular person and employer contributions to private and occupational plans is the bottom of 30% of whole web earnings, and EUR 1,500 per 12 months. Complete worker and employer contributions are restricted to EUR 8,500 per 12 months if the contribution is completed by the employer or by the worker into the identical occupational plan. | None |

| Sweden (SE) | Plans Different Than Premium Pension | E | T (15%) | T | For particular person pension financial savings plans, the annual cap on particular person contributions is 35% of eligible earnings (SEK 573,000 in 2024). | None |

| Switzerland (CH) | All | E | E | T | Particular person contributions to occupational pension plans are tax-deductible however capped at CHF 7,056. If a person doesn’t have an occupational plan, tax-deductible contributions are capped at 20% of annual earnings and the deduction can’t exceed CHF 35,280. | None |

| Turkey (TR) | Private Plans | T | T (5%/10%/15%) | E | There is no such thing as a restrict on contributions, however contributions are post-tax and topic to the stamp tax fee of 0.759%. | None |

| United Kingdom (GB) | All | E | E | T | The utmost amongst of pension contributions that a person can get tax aid on yearly is the upper of GBP 3,600 and 100% of taxable UK earnings. Pension contributions of greater than GBP 60,000 (tax 12 months 2023-2024) are topic to taxes that successfully restrict aid in a 12 months. Unused allowances could also be carried ahead for as much as three years. | None. Previous to 2024, lifetime allowance was set at GBP 1,073,100. |

| United States (US) | Conventional Plans (Not Roth Remedy) | E | E | T | Elective deferral contribution limits depend upon the kind of plan, however vary from USD 16,000 (SIMPLE plans) to USD 22,500 for 457(b) in 2024. Some plans enable further contributions for people age 50 years and older. | None |

Sources: OECD, “Annual Survey on Monetary Incentives for Retirement Financial savings: OECD Nation Profiles 2024,” Dec. 31, 2024, https://oecd.org/content material/dam/oecd/en/matters/policy-sub-issues/asset-backed-pensions/Annual-survey-financial-incentives-retirement-savings-2024-web.pdf; PwC, “Tax Summaries – Cyprus – Particular person,” Jul. 2, 2025, https://taxsummaries.pwc.com/cyprus/particular person/; Pitsas Insurances, “Provident Funds in Cyprus in 2025. An entire information,” https://pitsasinsurances.com/en/article/provident-funds-cyprus; PwC Malta, “The facility of occupational pension schemes,” Mar. 29, 2024, https://pwc.com/mt/en/publications/tax-legal/maximising-talent-retention-and-tax-efficiency.html.

[1] Typically, shares or possession shares of personal corporations or different tradeable properties obtain comparable tax therapy to that of publicly traded shares.

[2] Steve Rosenthal and Theo Burke, “Who’s Left to Tax? US Taxation of Firms and Their

Shareholders,” New York College College of Regulation, Oct. 27, 2020, https://regulation.nyu.edu/websites/default/recordsdata/WhopercentE2percent80percent99spercent20Leftpercent20topercent20Taxpercent3Fpercent20USpercent20Taxationpercent20ofpercent20Corporationspercent20andpercent20Theirpercent20Shareholders-%20Rosenthalpercent20andpercent20Burke.pdf.

[3] Named for the late Senator William Roth (R-DE).

[4] Alan Cole, “The 4 Completely different Methods the Tax Code Treats Saving and Funding,” Tax Basis, Could 24, 2016, https://taxfoundation.org/weblog/four-different-ways-tax-code-treats-saving-and-investment/.

[5] Named for the related part of the US tax code.

[6] Alex Muresianu and Sam Cluggish, “‘Trump Accounts’ May Be Higher. Right here’s How.” Tax Basis, Jul. 18, 2025, https://taxfoundation.org/weblog/trump-accounts-could-be-better/.

[7] For extra particulars on common financial savings accounts, see Robert Bellafiore, “The Case for Common Financial savings Accounts,” Tax Basis, Feb. 26, 2019, https://taxfoundation.org/case-for-universal-savings-accounts/.

[8] Authorities of Canada, “The Tax-Free Financial savings Account,” https://canada.ca/en/revenue-agency/companies/tax/people/matters/tax-free-savings-account.html.

[9] Will McBride, “Canada’s Tax-Free Financial savings Accounts Are a Large Success. U.S. Lawmakers Ought to Take Be aware,” Tax Basis, Feb. 8, 2024, https://taxfoundation.org/weblog/tax-free-savings-accounts-tfsa-canada/.

[10] Gov.uk, “Particular person Financial savings Accounts (ISAs),” https://gov.uk/individual-savings-accounts;

[11] Maximilian Bierbaum, “Designing financial savings and funding accounts within the EU,” New Monetary, Could 2025, https://newfinancial.org/stories/designing-savings-and-investment-accounts-in-the-eu.

[12] Polska Agencja Prasova, “Poland to launch tax-free funding accounts,” Aug. 5, 2025, https://pap.pl/en/information/poland-launch-tax-free-investment-accounts.

[13] See H.R. 937, H.R. 6757, and S. 232 from the 115th Congress and Alex Durante, William McBride, and Garrett Watson, “Dwindling Financial savings and Rising Monetary Stress Highlights Want for Tax Reforms,” Tax Basis, Nov. 9, 2023, https://taxfoundation.org/weblog/personal-saving-retirement-taxes/.

[14] See Possibility 63 in Tax Basis, “Choices for Reforming America’s Tax Code 2.0,” Apr. 19, 2021, https://taxfoundation.org/analysis/federal-tax/tax-reform-options/?possibility=63.

[15] William McBride, Huaqun Li, Garrett Watson, and Alex Durante, “Simplifying Saving and Enhancing Monetary Safety by Common Financial savings Accounts,” Tax Basis, Could 29, 2024, https://taxfoundation.org/analysis/all/federal/universal-savings-accounts-financial-security/.

Share this text