{kind=link}

If the US has not but entered a brand new “golden age,” by the appears of the inventory market, many individuals are nonetheless doing fairly effectively, particularly founders and others with a big stake within the meteoric rise of a number of profitable tech firms. It’s due to this fact not shocking {that a} new paper by Berkeley economists finds rising wealth focus on the prime lately, with the biggest fortunes primarily held in private and non-private companies.

The authors moreover calculate efficient taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of basic authorities companies, items, and actions. charges (ETRs) based mostly on that wealth, delivering the tantalizing however in the end deceptive outcome that the wealthiest Individuals pay a decrease ETR than the remainder of us because of the 2017 Tax Cuts and Jobs Act (TCJA).

Exaggerated High Revenue Definition Skews Research

Particularly, the authors discover that US federal, state, and native taxes as a share of “financial revenue” for the highest 0.0002 % (roughly the highest 400 wealthiest Individuals) averages to 23.8 % from 2018 to 2020, in comparison with about 30 % for the US inhabitants as an entire and 45 % for prime labor revenue earners. Previous to the TCJA, the examine finds the highest 400’s ETR was nearer to 30 %, with the drop since then primarily on account of diminished enterprise taxes and the expansion of wealth and financial revenue on the prime. Because the authors state, “these low efficient charges [after TCJA] are due considerably to a low ratio of taxable to financial revenue on the prime of the wealth distribution.”

And therein lies the rub. ETR estimates are often based mostly on one thing like taxable revenue, however this examine makes use of a way more expansive definition of revenue that’s effectively past what most individuals perceive revenue to be. The authors outline financial revenue as labor plus capital revenue, with capital revenue for the wealthiest outlined by the income of the companies they personal. Particularly, the authors estimate the shares of companies owned by the highest 400 after which allocate the unrealized ebook income of these companies to the homeowners in accordance with their shares.

This theoretical circulate of income to the person proprietor in the identical 12 months they’re reported is then misleadingly matched with precise taxes paid within the given 12 months (each on the enterprise entity degree and by the person). The impact is to drastically overstate the revenue of high-net-worth people and understate their ETR.

Company income solely turn out to be taxable revenue for shareholders after being distributed as dividends or realized as positive factors. Usually, a big portion of income is retained to gasoline future progress of the corporate, and homeowners solely notice positive factors after holding shares for a number of years. The examine paperwork that the wealthiest Individuals additionally personal pass-through companies, and people income are handed by means of to the homeowners as they’re earned. Nonetheless, solely taxable income are handed by means of versus the extra expansive definition of ebook income assumed by the examine’s authors.

David Splinter, an economist on the Joint Committee on Taxation, finds the examine overstates the wealth and revenue of the highest 400 taxpayers, because it doesn’t break up household wealth throughout a number of tax returns. The examine additionally understates the revenue of the underside half of the inhabitants, because it doesn’t account for transfers. Making these and different changes, Splinter finds the other outcome for a similar interval (2018 to 2020): the highest 400 ETR is 13 share factors greater than the general inhabitants’s ETR (38 % versus 25 %).

Research Makes use of Questionable Window of Evaluation

One other flaw within the examine is together with the pandemic 12 months 2020, which is tainted by large enterprise losses that may not be consultant of a typical 12 months. Moreover, it’s unlikely the examine’s outcomes would maintain if prolonged past 2020, after which federal tax income, and particularly company tax income, rebounded strongly. A part of this rebound was because of the timing results of the TCJA’s enterprise tax cuts.

The authors level to the TCJA’s expensing provision (bonus depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, resembling equipment or a manufacturing facility, to find out the multiyear interval over which the price of that asset might be deducted from taxable revenue. As an alternative of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, lowering their worth and disco) as an element that drastically diminished taxable enterprise revenue, however not financial revenue. However it’s well-known that expensing successfully shifts ahead deductions that may have in any other case occurred sooner or later, so that may counsel the authors’ discovering of a low ETR within the 2018-2020 interval is momentary and never reflective of ETRs within the years after 2020.

US High ETR Is Excessive Relative to Friends

As it’s, based mostly on the authors’ measure of ETRs, they notice that top-end ETRs are greater within the US than in lots of European international locations, together with the Netherlands, Sweden, and Norway. They attribute this partly to the widespread use of non-public wealth-holding firms in Europe that enable high-net-worth people to keep away from the particular person revenue taxA person revenue tax (or private revenue tax) is levied on the wages, salaries, investments, or different types of revenue a person or family earns. The U.S. imposes a progressive revenue tax the place charges improve with revenue. The Federal Revenue Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years outdated, particular person revenue taxes are the biggest supply.

One other unspoken issue is that the US doesn’t have significantly low taxes on enterprise and different capital revenue earned by high-net-worth people, and, by some measures, the US is above common relative to different international locations. The US company tax charge, together with each federal and state taxes, is about 5 share factors greater than the common company tax charge amongst European international locations. The highest US capital positive factors taxA capital positive factors tax is levied on the revenue produced from promoting an asset and is commonly along with company revenue taxes, ceaselessly leading to double taxation. These taxes create a bias in opposition to saving, resulting in a decrease degree of nationwide revenue by encouraging current consumption over funding. charge is about 10 share factors greater than the common amongst Organisation for Financial Co-operation and Growth (OECD) and choose EU international locations.

In the end, what is sensible is to make sure that US taxes are aggressive and certainly enticing to extremely cell capital. The TCJA did simply this. It diminished the company tax charge from the best within the OECD to extra close to the center of the pack and concurrently improved the enterprise tax baseThe tax base is the full quantity of revenue, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slim tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges. by permitting firms to instantly expense funding. A few of these concepts have been carried ahead on this 12 months’s One Massive Lovely Invoice Act (OBBBA), specifically everlasting full expensingFull expensing permits companies to instantly deduct the total price of sure investments in new or improved expertise, gear, or buildings. It alleviates a bias within the tax code and incentivizes firms to speculate extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs. for gear, home analysis and growth, and (quickly) sure buildings.

Federal Tax Code Is Extremely Progressive

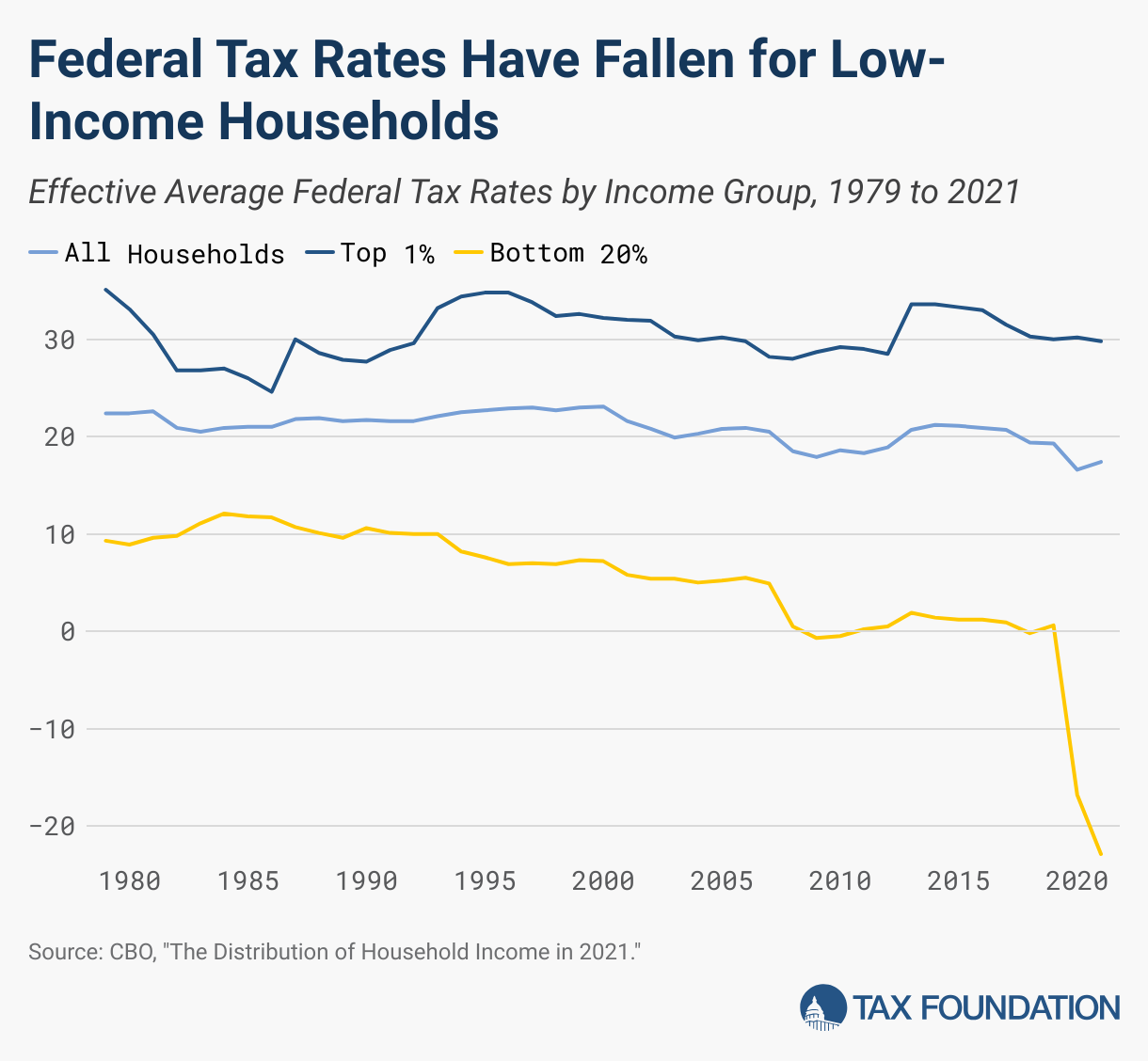

As for ETRs, extra normal approaches typically point out that US federal taxes are extremely progressive and that the tax code’s progressivity has elevated over time, even for the reason that TCJA by some measures. As an illustration, in accordance with the newest estimates from the Congressional Price range Workplace (CBO), which accounts for all federal taxes (however not state or native), the highest 1 % of earners in 2021 had an ETR of 29.8 %, in comparison with 17.4 % for the inhabitants as an entire and -22.9 % for the underside 20 % of households.

Pandemic aid applications, together with beneficiant refundable tax credit, clarify the significantly low and unfavorable ETRs for low-income households in 2021. Nonetheless, ETRs had been trending down for low-income households previous to the pandemic. As an illustration, the underside 20 % of households had an ETR of about 10 % within the Nineteen Eighties and early Nineties earlier than trending right down to 0.6 % in 2019. In distinction, the highest 1 % of earners had an ETR of 30.0 % in 2019, barely greater than the common ETR for this group in the course of the Nineteen Eighties and early Nineties. Many different research help this fundamental outcome, attributing the drop in ETRs for low-income households for the reason that Nineteen Eighties to more and more beneficiant refundable tax credit such because the earned revenue tax credit score and youngster credit score.

As many of the pandemic aid applications have wound down, ETRs have typically bounced again to pre-pandemic ranges. The OBBBA doesn’t drastically alter the downward pattern of ETRs for low-income households, in accordance with evaluation by the Joint Committee on Taxation.

Concentrating on wealth on the prime by means of greater taxes has a sure attraction, however it additionally comes with a whole lot of drawbacks, together with elevated avoidance and diminished incentives to speculate. The financial system wouldn’t be buzzing alongside with out the innovation, funding, and doubtlessly large productiveness positive factors arising from America’s tech sector and its entrepreneurs. Elevating taxes on probably the most profitable entrepreneurs and their companies dangers knocking out a key progress pillar for the inventory market and the financial system extra broadly, lowering retirement financial savings (most Individuals personal inventory), productiveness, wages, and job alternatives.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted specialists delivered straight to your inbox.

Share this text