{kind=link}

Key Findings

- The One Large Stunning Invoice Act (OBBBA) grew to become legislation on July 4, 2025.

- The legislation makes quite a few adjustments to US taxA tax is a compulsory fee or cost collected by native, state, and nationwide governments from people or companies to cowl the prices of basic authorities providers, items, and actions. legislation, some that enhance the tax code and a few that make it worse.

- By (principally) extending the expiring Tax Cuts and Jobs Act (TCJA) particular person earnings taxA person earnings tax (or private earnings tax) is levied on the wages, salaries, investments, or different types of earnings a person or family earns. The U.S. imposes a progressive earnings tax the place charges improve with earnings. The Federal Earnings Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years outdated, particular person earnings taxes are the biggest supply reforms, the OBBBA preserves a lot of the tax compliance value financial savings from that legislation.

- Nevertheless, the OBBBA loses floor on particular person earnings tax simplification in comparison with post-TCJA tax coverage.

- Exterior of the TCJA framework, the OBBBA additionally provides extra provisions to the person earnings tax than it subtracts.

- The brand new senior deduction, no tax on suggestions, no tax on time beyond regulation, and the automotive mortgage curiosity deduction, amongst others, far outweigh the cuts to consumer-side inexperienced power credit by way of simplification.

- Finally, whereas the OBBBA brings some stability by making lots of the TCJA’s reforms everlasting, it usually fails to reform the code’s accumulating complexity.

Introduction

The One Large Stunning Invoice Act (OBBBA) was handed into legislation on July 4, 2025. The legislation makes many structural enhancements to the tax code, most prominently by making the expiring particular person provisions of the Tax Cuts and Jobs Act (TCJA) everlasting.

Nevertheless, aside from repealing some power credit from the InflationInflation is when the overall value of products and providers will increase throughout the financial system, decreasing the buying energy of a forex and the worth of sure property. The identical paycheck covers much less items, providers, and payments. It is typically known as a “hidden tax,” because it leaves taxpayers much less well-off resulting from increased prices and “bracket creep,” whereas rising the federal government’s spendin Discount Act (IRA) and making everlasting expensing for sure sorts of enterprise funding, the legislation doesn’t develop upon the TCJA’s successes. It particularly fails to reform the tax code’s accumulating complexity, and certainly worsens it in lots of respects, together with via the addition of a number of new tax breaks.

Measuring Tax Complexity

Simplicity is without doubt one of the 4 essential ideas of sound tax coverage.[1] As outlined by the Tax Basis, simplicity “means taxes ought to be simple for taxpayers to pay and straightforward for governments to manage and gather.”[2] Having a easy tax code leads to elevated productiveness as a result of taxpayers shouldn’t have to spend extreme quantities of time on compliance. This elevated productiveness raises tax revenues. A easy tax code additionally makes it simpler and fewer resource-intensive for the federal government to implement compliance, leading to decrease evasion charges and better income collections.

A typical solution to gauge the complexity of the tax code is to have a look at the price of compliance. The IRS supplies estimates of the time required to adjust to every tax type in addition to the related out-of-pocket prices, e.g., for submitting providers. The IRS estimates it takes 13 hours on common to adjust to the principle particular person type, the Kind 1040—8 hours for people with out enterprise earnings, and 24 hours for people with enterprise earnings.[3] That’s one to 3 days of full-time work per individual that should be devoted to a single tax type.

Primarily based on the newest IRS estimates for all tax kinds, the Tax Basis finds that in 2025, compliance with the federal tax code goes to value People 7.1 billion hours of their time.[4] This burden is equal to three.4 million full-time employees doing nothing however tax return paperwork for a full 12 months. As well as, the IRS estimates out-of-pocket prices of $148 billion, leading to complete monetized compliance prices of $536 billion in 2025. Of this, about $147 billion and a pair of.1 billion hours might be spent on the Kind 1040, with a lot of the remaining burden falling on companies.[5]

As one other measure of the tax code’s rising complexity, a latest examine finds that the size of the Inside Income Code has grown to about 4.3 million phrases as of 2021, a rise of about 40 p.c over the past three a long time. The examine additionally compares tax codes throughout six international locations, discovering that the US has by far the longest and most advanced tax code.[6]

The United States tax code is advanced, not easy. Sadly, the OBBBA additional complicates tax submitting.

Core Particular person Tax Reforms

The unique impetus for the OBBBA was extending the expiring particular person earnings tax cuts and reforms handed within the TCJA. The TCJA simplified the tax code via two channels: decreasing the usage of itemized deductions and decreasing the variety of taxpayers topic to the choice minimal tax (AMT).[7] Nevertheless, it additionally added Part 199A, also referred to as the pass-through deduction, an ill-considered tax break from a structural perspective that additionally comes with vital prices.

For essentially the most half, the OBBBA retains the TCJA’s structural adjustments to the person earnings tax. Nevertheless, whether or not these extensions qualify as “enhancements” to the tax code relies on the baseline one makes use of.

Desk 1. How OBBBA Modifications Core Particular person Earnings Tax Provisions

Provision, Description, 1-Yr and 10-Yr Standard Income Impact

Word: Scores are all from Tax Basis, aside from the transferring bills deduction, which comes from the Joint Committee on Taxation.

Supply: H.R.1, One Large Stunning Invoice Act, Tax Basis Basic Equilibrium Mannequin, July 2025; Joint Committee on Taxation , “Estimated Income Results Relative to the Current Legislation Baseline of the Tax Provisions in ‘Title VII: Finance’ of the Substitute Laws as Handed by the Senate to Present for Reconciliation of the Fiscal Yr 2025 Finances,” Jul. 1, 2025, https://www.jct.gov/publications/2025/jcx-35-25/.

Within the OBBBA debate, some policymakers argued the expiring TCJA tax cuts ought to be handled beneath a “present coverage baseline”—that’s, as if the expiring tax cuts could be prolonged completely. In contrast with this baseline, permanence would carry no further fiscal prices. A present legislation baseline, however, assumes the tax cuts would expire as scheduled, so permanence would entail further prices.[8]

These baselines reduce each methods. A present coverage baseline may imply extending expiring tax cuts doesn’t “value” something in a fiscal sense, but it surely additionally means the legislation shouldn’t get any credit score for the tax simplifications which have already been in impact for nearly eight years.

Itemizers

A number of TCJA reforms decreased itemization, each by increasing the commonplace deductionThe usual deduction reduces a taxpayer’s taxable earnings by a set quantity decided by the federal government. Taxpayers who take the usual deduction can not additionally itemize their deductions; it serves in its place. and limiting itemized deductions.

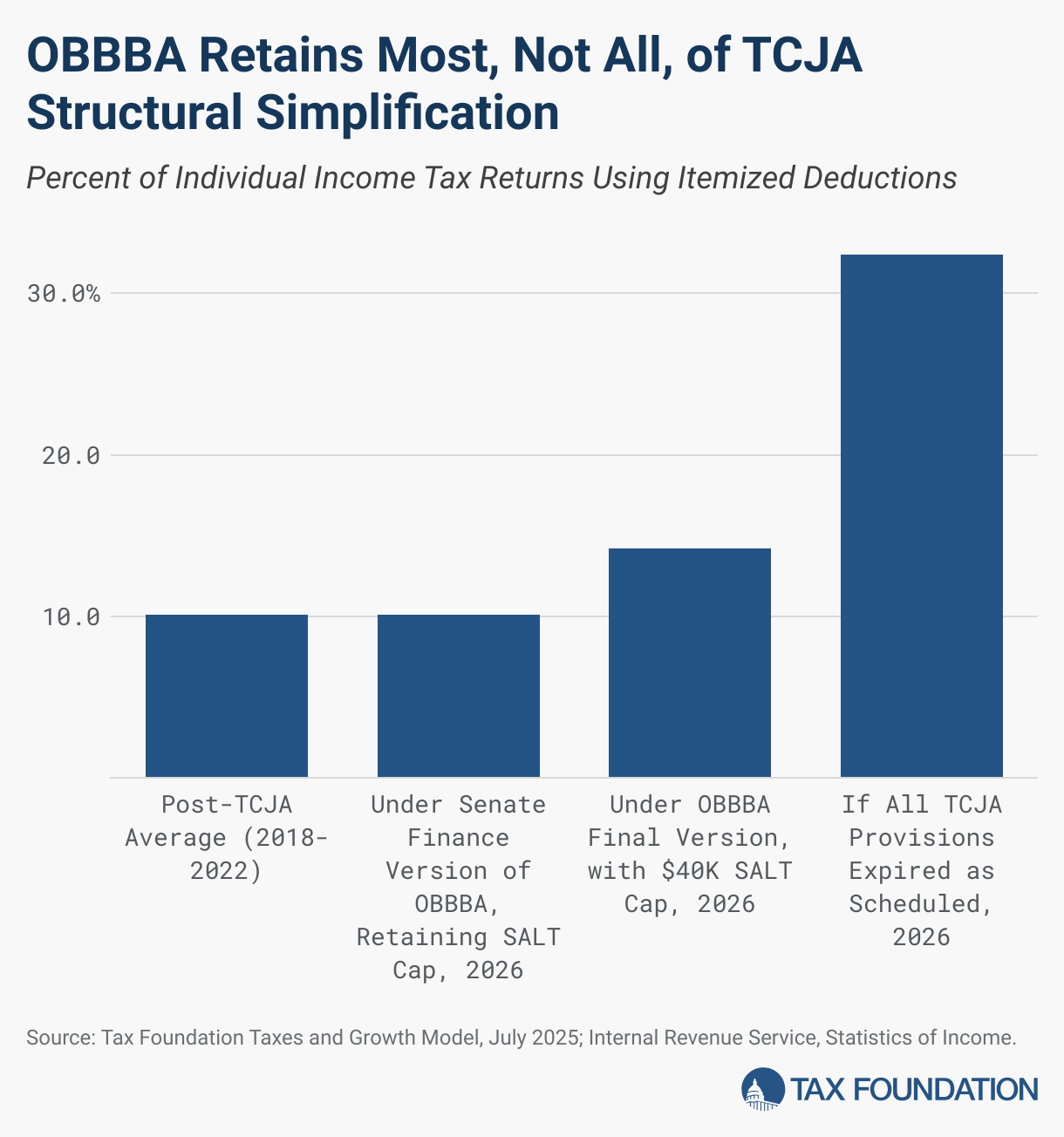

On the entire, the legislation dramatically decreased the variety of itemizers—from 46.9 million in 2017 (31 p.c of complete filers) to 17.5 million in 2018 (11.5 p.c of complete filers). Together with different simplifications, decreasing the variety of itemizers meant the TCJA introduced vital compliance value financial savings—doubtlessly over $5 billion in 2018 alone.[9] And itemization has continued to fall. In 2022 (the newest 12 months with full IRS knowledge out there), the itemization price was beneath 10 p.c.

The OBBBA principally retains the TCJA’s itemization reforms. It eliminates the private exemption completely and makes the usual deduction growth everlasting with a small further increase. On itemized deductions, the OBBBA retains the TCJA’s mortgage curiosity limitation and completely eliminates the miscellaneous itemized deductions, aside from the deduction for unreimbursed educator bills. Nevertheless, the OBBBA offers floor on the state and native tax (SALT) deductionThe state and native tax (SALT) deduction permits taxpayers who itemize when submitting federal taxes to deduct sure taxes paid to state and native governments. The Tax Cuts and Jobs Act (TCJA) capped it at $10,000 per 12 months, consisting of property taxes plus state earnings or gross sales taxes, however not each.: rising the deduction to $40,000 in 2025, and rising it by 1 proportion level annually till 2029, after which it would return to $10,000 completely.

The OBBBA limits itemized deductions in new methods too. The legislation provides a minimal threshold of 0.5 p.c of gross earningsFor people, gross earnings is the overall of all earnings obtained from any supply earlier than taxes or deductions. It consists of wages, salaries, suggestions, curiosity, dividends, capital positive factors, rental earnings, alimony, pensions, and different types of earnings.

For companies, gross earnings (or gross revenue) is the sum of complete receipts or gross sales minus the price of items bought (COGS)—the direct prices of manufacturing items to the itemized charitable deduction and limits the worth of itemized deductions to 35 p.c, even for taxpayers within the 37 p.c bracket. The OBBBA additionally introduces a flooring for the itemized charitable deduction, solely permitting itemizing taxpayers to deduct charitable contributions in extra of 0.5 p.c of their adjusted gross earnings.[10]

If we use a present legislation baseline, then the OBBBA’s impact on itemizers is the distinction between the variety of itemizers projected in 2026 had all the TCJA’s provisions expired, and the quantity projected beneath the OBBBA. Alternatively, beneath a present coverage baseline, the OBBBA’s impact is the distinction between itemizers beneath the OBBBA, and itemizers beneath a situation the place the TCJA was made everlasting with no different adjustments.

Below a present legislation baseline, we projected 32 p.c of filers with constructive earnings would itemize in 2026, that means there could be 54.5 million itemizers. In the meantime, beneath the OBBBA, we projected 14.2 p.c of filers would itemize, or 23.9 million itemizers. Below the present legislation baseline, this interprets to the OBBBA decreasing itemizers by 30.6 million.

Nevertheless, beneath a present coverage baseline the place the TCJA’s reforms are made everlasting with out alteration, we’d anticipate round 10 p.c of filers to itemize, as we’ve seen lately beneath the TCJA regime. We estimated that 10.1 p.c of taxpayers would itemize beneath the Senate Finance Committee’s model of the laws that maintained the $10,000 SALT cap. That interprets to 16.95 million itemizers. With 16.95 million itemizers as a baseline, which means the 23.9 million itemizers beneath the OBBBA interprets to six.9 million further itemizers.

These variations in itemization can translate into vital prices.

Whereas the IRS doesn’t publish detailed schedule-level compliance value estimates, we are able to extrapolate from primary info out there. In 2004, the IRS estimated the typical taxpayer took round 13.6 hours to file their taxes, and that the typical Schedule A itemized deductionItemized deductions permit people to subtract designated bills from their taxable earnings and could be claimed in lieu of the usual deduction. Itemized deductions embrace these for state and native taxes, charitable contributions, and mortgage curiosity. An estimated 13.7 p.c of filers itemized in 2019, most being high-income taxpayers. type took round 5.6 hours to finish.[11] In 2024, the IRS estimated the typical taxpayer took 13 hours to file their taxes.[12] Whereas the IRS didn’t publish a corresponding estimate for Schedule A in 2024, we are able to estimate submitting itemized deductions takes a median of 5.3 hours, assuming submitting time has declined proportionately.

To translate hourly compliance prices to a greenback worth, we sometimes use the typical hourly wage of all occupations ($32.66) plus the typical hourly non-wage compensation for personal sector workers ($13.49), translating to an hourly alternative value of $46.15.[13]

Utilizing these estimates, we are able to convert these variations in itemizers to arduous financial estimates. If we use the present legislation baseline, by extending a lot of the expiring TCJA reforms, the OBBBA will scale back compliance prices by $7.5 billion in 2026 by decreasing the variety of itemizers.

Nevertheless, utilizing a present coverage baseline, the OBBBA will improve compliance prices by $1.7 billion in 2026, largely resulting from rising the SALT deduction cap. In different phrases, the OBBBA will increase compliance prices in comparison with easy TCJA permanence.

It’s price noting that the change in itemizers isn’t the only real measure of tax compliance prices, and these adjustments will not be complete estimates of how the OBBBA adjustments compliance prices in combination.

Little one Tax Credit score

The TCJA elevated the utmost CTC from $1,000 to $2,000, however that improve was scheduled to run out on the finish of 2025. Whereas the CTC growth didn’t in itself simplify the tax code, it was a key a part of repealing the private exemption and rising the usual deduction.

The OBBBA will increase the CTC to $2,200 per little one in 2025 and indexes the utmost quantity for inflation going ahead. This alteration doesn’t add complexity to the CTC. Nevertheless, it doesn’t simplify the CTC both. The CTC has a number of structural points, as does the earned earnings tax credit score (EITC), and a extra bold tax reform may have addressed these points extra comprehensively.[14]

Different Minimal Tax

The AMT is another earnings tax designed to stop high-income households from deducting right down to zero earnings tax legal responsibility. Different minimal taxable earnings (AMTI) usually eliminates or reduces the worth of tax preferences taken beneath the extraordinary particular person earnings tax. As soon as AMTI has been established, an exemption could be taken from AMTI. Below pre-OBBBA legislation, the exemption phases out by $0.25 per greenback of AMTI above a sure threshold. Lastly, the primary $239,100 of AMTI ($119,550 for married separate filers) is taxed at 26 p.c, and the remaining is taxed at 28 p.c.

Earlier than 2017, the AMT exemption was $54,300 for single filers and $84,500 for married filers, and the phaseout threshold began at $120,700 for single filers and $160,900 for married filers. The TCJA raised the exemption to an inflation-adjusted $70,300 and $109,400, respectively, and the phaseout threshold to an inflation-adjusted $500,000 and $1,000,000, respectively. This had a big impact on the variety of filers for the AMT.

In 2017, earlier than the TCJA adjustments, there have been 5.1 million tax returns paying the AMT, which was a 9.5 p.c improve from the 12 months prior. Nevertheless, in 2018, that quantity dropped to solely 244,000 payers—a 95.2 p.c drop from 2017. That quantity continues to remain low, with AMT payers fluctuating between 150,000 and 250,000 between 2018 and 2022 (the newest 12 months of information out there).[15] Nevertheless, the extra related quantity for compliance prices is the change within the variety of filers who must calculate their AMT legal responsibility, no matter what number of find yourself really owing something beneath the AMT. In 2017, there have been 10.78 million particular person AMT kinds filed. Since then, the typical variety of AMT kinds filed is 5.98 million.[16] In the meantime, the Taxpayer Advocate Service has beforehand estimated that calculating AMT legal responsibility roughly doubles the burden of submitting an earnings tax return.[17]

If we assume that relationship nonetheless holds, we are able to estimate compliance financial savings. The change from 10.78 million to five.98 million means 4.8 million fewer taxpayers who have to calculate their AMT legal responsibility. The typical Kind 1040 filer takes 13 hours as of 2025, which suggests the discount in AMT calculators would save 62.43 million hours. Utilizing median wages and advantages of $46.15 as the chance value, we are able to estimate the annual financial savings from the TCJA’s discount in AMT calculators as round $2.9 billion.

The OBBBA extends the TCJA exemption and phaseout threshold ranges completely, sustaining the inflation changes. Nevertheless, the OBBBA reverts the phaseout thresholds again to $500,000 ($1 million for joint filers), adjusted for inflation beginning in 2026. It additionally raises the phaseout price to $0.50 for every greenback of AMTI above the phaseout threshold.

Finally, the OBBBA’s reforms to the AMT mirror its reforms to itemized deductions. If we deal with present legislation (beneath which the AMT would have reverted to the pre-TCJA construction) because the baseline, the OBBBA is a considerable transfer towards simplification. Nevertheless, if we deal with full TCJA permanence because the baseline, the OBBBA will imply barely extra AMT filers, extra AMT calculators, and accordingly extra complexity.

Cross-By way of EnterpriseA pass-through enterprise is a sole proprietorship, partnership, or S company that isn’t topic to the company earnings tax; as an alternative, this enterprise reviews its earnings on the person earnings tax returns of the homeowners and is taxed at particular person earnings tax charges. Deduction

The TCJA launched Part 199A, also referred to as the pass-through deduction. The deduction permits people to deduct the decrease of 20 p.c of their earnings earned in a pass-through enterprise or 20 p.c of their taxable extraordinary earnings.

For higher-income households, the pass-through deduction additionally consists of limits on earnings earned in specified service and commerce companies (SSTBs) and necessities associated to precise enterprise exercise.[18] These guidelines exist for an excellent cause: to restrict the reclassification of what’s, in observe, worker compensation as capital earnings eligible for the deduction. On the identical time, they create vital complexity. Moreover, the construction of the phaseout creates massive tax cliffs for SSTB homeowners.

The OBBBA makes Part 199A everlasting with some small tweaks. The legislation slows the phaseout from occurring over $50,000 for single filers and $100,000 for married submitting collectively to over $75,000 for single filers and $150,000 for married submitting collectively. The OBBBA additionally introduces a brand new minimal deduction of $400 for any taxpayer incomes above $1,000 in certified enterprise earnings.

In 2024, we estimated the pass-through deduction produced compliance prices of just about $20 billion a 12 months.[19] The pass-through deduction is one other situation the place judging the OBBBA on a present legislation versus a present coverage baseline makes an enormous distinction. Below a present coverage baseline, the OBBBA marginally improves the pass-through deduction. However beneath a present legislation baseline, the OBBBA makes a fancy provision everlasting that might have in any other case expired.

New Particular Tax Breaks

The OBBBA doesn’t persist with tinkering with the structural adjustments the TCJA introduced. As a substitute, the legislation introduces many new, slender tax deductions for particular sorts of earnings or consumption. These provisions decide favorites, as they deal with sure sorts of earnings in sure industries extra generously than others, whereas additionally including to the legislation’s price ticket.

Desk 2. New Tax Breaks Value Nearly $400 Billion, Concentrated within the First 4 Years of Finances Window

Provision, Description, 1-Yr and 10-Yr Standard Income Impact

Word: Scores from Tax Basis, aside from the Trump Accounts and the tax credit score for scholarship-granting organizations.

Supply: H.R.1, One Large Stunning Invoice Act, Tax Basis Basic Equilibrium Mannequin, July 2025; Joint Committee on Taxation , “Estimated Income Results Relative to the Current Legislation Baseline of the Tax Provisions in ‘Title VII: Finance’ of the Substitute Laws as Handed by the Senate to Present for Reconciliation of the Fiscal Yr 2025 Finances,” Jul. 1, 2025, https://www.jct.gov/publications/2025/jcx-35-25/.

Extra time Deduction

The time beyond regulation deduction is the same as the certified time beyond regulation compensation obtained with a deduction cap of $12,500 ($25,000 for married submitting collectively) and a phaseout provision when AGI exceeds $150,000 ($300,000 for married submitting collectively). This deduction is simply relevant to the “and-a-half” little bit of the “time-and-a-half” compensation for time beyond regulation work, and is simply out there in 2025 via 2028.

Economically, this provision creates a tax bias for time beyond regulation earnings and industries topic to the time-and-a-half rule. It introduces a wholly new distinction within the tax code. The time-and-a-half rule comes from the Honest Labor Requirements Act (FLSA), and resides in labor legislation, not tax legislation. Incorporating this labor legislation idea into the tax code in a means that limits abuse would require substantial administration and compliance work.[20]

Tax DeductionA tax deduction permits taxpayers to subtract sure deductible bills and different objects to scale back how a lot of their earnings is taxed, which reduces how a lot tax they owe. For people, some deductions can be found to all taxpayers, whereas others are reserved just for taxpayers who itemize. For companies, most enterprise bills are totally and instantly deductible within the 12 months they happen, however ot for Suggestions

The brand new deduction for suggestions permits employees in traditionally tipped industries to deduct as much as $25,000 in certified suggestions in tax years 2025 via 2028. There’s a phaseout of $100 per $1,000 of AGI beginning at $150,000 ($300,000 for married joint filers).

It additionally features a transition rule to offer taxpayers time to regulate to this new provision. This provides complication to the tax code by unnecessarily distinguishing tip earnings, which solely about 3 p.c of the US workforce makes, from different earnings.[21] Just like the deduction for time beyond regulation, it would require considerably sophisticated guardrails to stop abuse, leading to further administrative and compliance work.

Automobile Mortgage Curiosity Deduction

The automotive mortgage curiosity deduction, out there from 2025 via 2028, supplies a $10,000 deduction for auto mortgage curiosity with a phaseout beginning for taxpayers with AGI of over $100,000 ($200,000 for married submitting collectively). Vehicles should meet a number of standards to be eligible. Remaining meeting should happen in the USA, they should be handled as a automobile beneath the Clear Air Act, they usually should have a gross automobile weight score beneath 14,000 kilos. Taxpayers should additionally present a automobile identification quantity.

These numerous circumstances will almost definitely require the IRS to publish and preserve an inventory of automotive fashions eligible for this new tax profit, very similar to they did for the electrical automobile tax credit handed within the Inflation Discount Act of 2022, which additionally got here with circumstances associated to content material origin.[22] Automobile sellers and particular person consumers might want to incorporate and confirm this and different info, together with earnings of the client, to adjust to the principles, and the IRS might want to independently confirm it, resulting in substantial administrative and compliance prices.

Senior Deduction

As a substitute of exempting Social Safety from earnings tax, the OBBBA provides a $6,000 deduction for taxpayers over 65.[23] This provision begins to part out when the taxpayer’s AGI exceeds $75,000 ($150,000 for married submitting collectively), requires a Social Safety quantity to obtain the deduction, and solely permits the deduction for taxable years 2025 via 2028, at a value of $137 billion.[24]

This coverage has fewer compliance challenges than the deductions for suggestions and time beyond regulation. It supplies extra advantages to lower-middle-income seniors in comparison with what no tax on Social Safety would have completed.[25] Nonetheless, it’s an costly tax break giving preferential remedy to taxpayers based mostly on age, including yet one more wrinkle to the tax code.

Trump Accounts

Trump Accounts intention to encourage saving for a kid’s future by permitting dad and mom and others to contribute as much as a mixed $5,000 yearly for the kid to make use of after reaching age 18.[26] Youngsters born in 2025 via 2028 (as US residents with Social Safety numbers) might be robotically enrolled and obtain a one-time deposit of $1,000 from the federal authorities into their account.[27]

The account grows tax-deferred till account homeowners make withdrawals, which might solely begin at age 18. At this level, it basically follows the principles in place for particular person retirement accounts (IRAs). As such, withdrawals, internet of after-tax contributions, made earlier than age 59 ½ are topic to common earnings tax and a ten p.c penalty, with many exceptions, together with for faculty tuition (limitless) and for a first-time residence buy (as much as $10,000).[28]

Whereas computerized enrollment will broaden the attain of Trump Accounts, it is going to be an administrative problem to implement and preserve such a system. The restricted tax advantages and sophisticated guidelines are unlikely to encourage substantial further saving for many enrollees, which is why virtually all the estimated fiscal value of the supply is from the federal government’s preliminary one-time deposit.

Trump Accounts are one other layer to an already overcomplicated financial savings account system within the United States. The tax code already supplies for not less than 11 tax-advantaged financial savings autos,[29] every with totally different guidelines, limitations, and laws. Trump Accounts will additional complicate financial savings for taxpayers, Treasury, and the IRS.

Including one other boutique financial savings account to the pile is a step towards complexity, not alternative.

Tax Credit score for Scholarship-Granting Organizations

The OBBBA creates a tax credit score for charitable contributions to tax-exempt organizations that present scholarships to elementary and secondary faculty college students. The credit score is as much as a most of $1,700. College students who profit from the scholarship funds should be eligible to enroll in public faculty and be a member of a family with an earnings not higher than 300 p.c of the realm’s median gross earnings.

The objective of this provision is to allow state-level faculty alternative applications, however one other tax credit score provides pointless litter to the code, together with new administrative and compliance challenges.

Enlargement of Present or Historic Tax Breaks

The OBBBA doesn’t simply create new particular tax breaks; it additionally boosts some current tax breaks, significantly these associated to well being care, little one care, and schooling.

Desk 3. How OBBBA Expands Handful of Present Tax Breaks

Provision, Description, 1-Yr and 10-Yr Standard Income Impact

Word: Scores for CDCTC, charitable deduction swap from Tax Basis; different scores from Joint Committee on Taxation.

Supply: H.R.1, One Large Stunning Invoice Act, Tax Basis Basic Equilibrium Mannequin, July 2025; Joint Committee on Taxation , “Estimated Income Results Relative to the Current Legislation Baseline of the Tax Provisions in ‘Title VII: Finance’ of the Substitute Laws as Handed by the Senate to Present for Reconciliation of the Fiscal Yr 2025 Finances,” Jul. 1, 2025, https://www.jct.gov/publications/2025/jcx-35-25/.

Well being Saving Accounts

Well being financial savings accounts (HSAs) are individually owned financial savings accounts that can be utilized for certified medical bills and might solely be contributed to when the beneficiary has a high-deductible insurance coverage plan.[30] HSAs are totally tax exempt—the cash is tax free on entry and exit.[31] The OBBBA makes three adjustments to how HSAs can be utilized and who can use them.

First, the legislation adjustments how deductible telehealth providers decide a plan’s classification as a “high-deductible plan.” Beforehand, plans with out a deductible for telehealth providers wouldn’t qualify as high-deductible and subsequently couldn’t be paired with HSAs. Now, such plans do qualify. Equally, Bronze and Catastrophic Plans, choices bought via the Reasonably priced Care Act (ACA) Alternate, qualify as “high-deductible plans,” and could be paired with HSAs.

Lastly, the OBBBA permits people to retain eligibility for HSAs if they’ve enrolled in a direct major care service association, supplied these preparations don’t value greater than $150 monthly per particular person. Bills for these direct major care service preparations additionally change into eligible HSA bills.

These new provisions simplify HSAs by making extra plans and bills eligible, and the growth of direct major care by way of HSAs could simplify the supply of and billing for health-care providers. Nevertheless, it is a trade-off because it leaves an advanced morass of tax-preferred saving choices within the tax code, which ought to ideally be consolidated and streamlined.

Above-the-Line Charitable Deduction

As talked about earlier, the OBBBA created a flooring for the itemized deduction for charitable contributions. Nevertheless, the OBBBA reintroduces the above-the-line deduction for charitable contributions. The CARES Act of 2020 launched a $300 above-the-line deduction for charitable contributions for 2020, and the Consolidated Appropriations Act of 2020 prolonged the coverage into 2021 whereas rising the utmost deduction to $600 for joint filers.[32] This coverage expired after 2021.

The OBBBA completely reintroduces the above-the-line charitable deduction at increased ranges, permitting as much as $1,000 for single filers and $2,000 for married submitting collectively. Whereas a small above-the-line deduction might need been a worthwhile commerce in a broader reform that totally eradicated itemized deductions, it provides pointless complexity within the broader context of the OBBBA. Primarily based on the expertise with the COVID pandemic-era above-the-line charitable deduction, this provision could not considerably improve charitable contributions however as an alternative present windfall positive factors for individuals who would have donated anyway.[33]

Schooling

The OBBBA extends the tax exclusion for employer-sponsored pupil mortgage funds. First launched in 2020, this provision creates a brand new type of untaxed non-wage compensation. Employer funds for pupil loans are a type of compensation and shouldn’t be tax-preferred relative to wages and salaries.[34]

The OBBBA additionally expands eligible bills for 529 accounts. The act provides each elementary, secondary, and homeschool bills and postsecondary credentialing bills as certified schooling bills. Whereas broadening the definition of academic bills eligible for 529s could make them simpler to make use of, as with HSAs, policymakers ought to search for methods to consolidate the multitude of tax-preferred financial savings accounts quite than increasing expense eligibility for every one in comparatively minor methods.

Little one and Dependent Care

The OBBBA expands a number of insurance policies geared toward youngsters and dependents along with the kid tax credit score. Two of these applications, the dependent care help program (DCAP) and the kid and dependent care tax credit score (CDCTC), have been structurally sophisticated earlier than the OBBBA and stay so afterward.

DCAP permits taxpayers to put aside pre-tax wages to pay for dependent care (together with little one care and elder care). The OBBBA raised the utmost quantity eligible for this pre-tax profit from $5,000 to $7,500 for joint filers. Equal to a deduction, DCAP is one other employer-sponsored fringe profit that receives particular tax remedy by way of a delegated account that should be tracked by the worker and employer.

The legislation additionally adjustments the CDCTC. The credit score covers as much as $3,000 of care bills for a single dependent and $6,000 for 2 or extra dependents. The credit score worth is calculated as a proportion of these certified bills that varies in line with the taxpayer’s AGI. Earlier than the OBBBA, the credit score price began at 35 p.c of care bills (that means a most credit score of $1,050 for one dependent) and phased down incrementally beginning at $15,000 in AGI to twenty p.c for taxpayers incomes over $43,000.[35]

The OBBBA expands the credit score however retains an analogous construction. Beginning in 2026, the utmost credit score might be 50 p.c of eligible childcare bills, which is able to part down incrementally to 35 p.c between $15,000 and $43,000 in AGI. Then the credit score phases down from 35 p.c to twenty p.c between $43,000 and $75,000 in AGI. Whereas the credit score is bigger, it nonetheless has a fancy construction. If the coverage objective is to supply further assist to folks, it will be preferable to easily develop switch funds or the CTC as an alternative of utilizing one other sophisticated coverage lever.

The legislation additionally tweaks the adoption credit score. Taxpayers could declare a most credit score of $16,810 (adjusted for inflation yearly) for qualifying adoption bills. The credit score phases out for adjusted gross incomes over $252,150 and utterly phases out for incomes over $292,150. The legislation makes the credit score partially refundable, as much as $5,000 (listed for inflation) starting in 2024, however it may now not be carried ahead.

Further Base-Broadening: Repealing Inflation Discount Act Inexperienced Vitality Credit

The principle supply of further base-broadening within the OBBBA is eliminating or proscribing inexperienced power credit. Most of these credit are primarily for companies.[36] Nevertheless, on the person facet, the OBBBA does repeal credit for electrical autos, residence power property, and power effectivity enhancements. Mixed, these repeals account for nearly $260 billion in income over the following decade.

Desk 4. How OBBBA Pulls Again Particular person IRA Tax Credit

Provision, Description, 1-Yr and 10-Yr Standard Income Impact

Word: Some EV credit are paid to companies.

Supply: Tax Basis Basic Equilibrium Mannequin, July 2025.

Electrical Car Credit

The OBBBA repeals 4 tax credit for electrical autos. The electrical automobile credit score (30D) supplied a $7,500 tax credit score for shoppers buying electrical autos, supplied the autos meet home battery and sourcing necessities.[37] The certified industrial electrical automobile tax credit score (45W) was initially meant for industrial automobile operators, and it supplies a $7,500 tax credit score for EVs with out the battery and sourcing necessities.

Nevertheless, the legislation options what some name the leasing loophole: automotive dealerships can declare the 45W tax credit score for automobiles they buy and cross the advantages of the credit score on to leaseholders, even when these automobiles don’t meet the necessities related to the 30D credit score.[38] There are two different related smaller credit: a tax credit score for used EV purchases (25E) and a tax credit score for refueling property (30C). The OBBBA repeals all these credit after September 30, 2025, aside from the tax credit score for refueling property, which expires as of June 30, 2026.

These repeals are simple and justifiable. Though they’re fairly beneficiant, EV credit sometimes don’t transfer the needle for EV purchases. Proof suggests most EV credit score recipients would have bought an EV with out the subsidy.[39] EVs are sometimes pushed lower than inner combustion engine autos per 12 months—that means a rise in EV possession may not translate to a proportional discount in transportation emissions.[40] Accordingly, the EV credit are costly relative to the discount in CO2 emissions they supply.

Eliminating the credit may also eradicate the compliance prices related to them as nicely. In 2023, the electrical automobile credit score appeared on just below half one million returns, whereas the beforehand owned electrical automobile credit score appeared on lower than 30,000.[41] Primarily based on the expansion of EV leasing, the variety of industrial EV credit related to people was additionally vital.[42] Whereas an estimate of the hours required to adjust to these credit isn’t out there, the voluminous laws issued to elucidate the credit signifies compliance isn’t easy.[43]

Residential Property

The OBBBA additionally repeals a number of credit aimed on the residential sector. The 2 most important credit, the power environment friendly residence enchancment credit score (25C) and residential clear power credit score (25D), will now expire after December 31, 2025. The power environment friendly residence enchancment credit score supplies advantages for the acquisition of recent energy-efficient structural elements, akin to sure sorts of doorways, home windows, water heaters, or central air-con programs.[44] In the meantime, the residential clear power credit score targets power manufacturing, predominantly rooftop photo voltaic panels, however consists of another applied sciences.

Some proof exhibits the energy-efficient property credit score can stimulate new purchases. Nevertheless, the residential clear power credit score traditionally encourages rooftop photo voltaic, which is rather more costly per kilowatt hour of electrical energy than utility-scale photo voltaic era.[45] In 2023, the residential clear power credit score appeared on 1.2 million returns, whereas the energy-efficient residence enchancment credit score appeared on 2.3 million. Eliminating the credit will considerably scale back compliance prices—though, as with the EV credit, a exact estimate of hours required to conform is unavailable.[46]

Quantifying the Results of OBBBA on Tax Complexity

Tax compliance prices are a great way to measure tax complexity. However at this level, we shouldn’t have sufficient info to quantify the compliance value adjustments of the brand new provisions. It’s potential to estimate shifts in itemization charges, AMT submitting, and the pass-through deduction based mostly on historic knowledge. Nevertheless, we are able to solely speculate on the compliance prices related to new provisions just like the deductions for suggestions and time beyond regulation pay.

Yale Finances Lab not too long ago estimated how the brand new tax provisions would change the submitting time burden of the person earnings tax.[47] Nevertheless, there are two essential challenges to this strategy. We merely have no idea how lengthy the brand new provisions will add to submitting time. Extra essentially, the time burden of a person submitting their taxes doesn’t seize the complete value of compliance. Some provisions require vital compliance work from payroll departments.

One may level to the OBBBA’s phrase depend exceeding 100,000 as proof for its complexity. Alternatively, one may add collectively the income results of all base-broadening provisions and all base-narrowing provisions to see if the tax on internet broadened or narrowed tax bases. However this strategy has a number of issues.

For one, it flattens the excellence between having a number of main tax breaks and lots of small ones. Rising the utmost little one tax credit score doesn’t improve tax code complexity the identical means introducing 10 new separate applications for kids does. Within the case of some provisions, simplification may slender the tax baseThe tax base is the overall quantity of earnings, property, property, consumption, transactions, or different financial exercise topic to taxation by a tax authority. A slender tax base is non-neutral and inefficient. A broad tax base reduces tax administration prices and permits extra income to be raised at decrease charges.. The choice minimal tax is arguably a base-broadening provision within the tax code, but it surely broadens the bottom by successfully making a second tax system quite than simplifying the principle one we now have.

Setting apart the TCJA-related structural adjustments, we are able to see how the most important base-broadening and base-narrowing provisions examine. In 2026, the brand new tax breaks are projected to value virtually $89 billion, with the expansions to a handful of current tax breaks projected so as to add one other $3 billion. In the meantime, the individual-side rollbacks of the IRA credit increase just below $29 billion.

Trying on the decade-long impression of those provisions makes the base-broadening seem barely extra proportional. The person IRA credit score cuts offset over half of the brand new and expanded slender tax breaks over the course of a decade. Nevertheless, the price of the brand new tax breaks over a decade solely consists of the 4 years they’re in full impact. If these momentary insurance policies have been prolonged completely, their cumulative prices would doubtless strategy $1 trillion, additional dwarfing the repeals of the EV and residential power credit.

Desk 5. How OBBBA’s Additions Slim the Tax Base

Supply: Tax Basis Basic Equilibrium Mannequin, July 2025; Joint Committee on Taxation , “Estimated Income Results Relative to the Current Legislation Baseline of the Tax Provisions in ‘Title VII: Finance’ of the Substitute Laws as Handed by the Senate to Present for Reconciliation of the Fiscal Yr 2025 Finances,” Jul. 1, 2025, https://www.jct.gov/publications/2025/jcx-35-25/.

What This Paper Does Not Cowl

This paper focuses on how adjustments to the person earnings tax impression private returns. The OBBBA additionally consists of vital adjustments to enterprise taxes. Most significantly, it made one hundred pc bonus depreciationDepreciation is a measurement of the “helpful life” of a enterprise asset, akin to equipment or a manufacturing facility, to find out the multiyear interval over which the price of that asset could be deducted from taxable earnings. As a substitute of permitting companies to deduct the price of investments instantly (i.e., full expensing), depreciation requires deductions to be taken over time, decreasing their worth and disco for short-lived property and full expensingFull expensing permits companies to instantly deduct the complete value of sure investments in new or improved know-how, tools, or buildings. It alleviates a bias within the tax code and incentivizes firms to take a position extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs. for home analysis and growth everlasting. Each of these insurance policies repair tax penalties for broad classes of capital funding.

The enterprise facet of the legislation included some base-broadening (repealing or proscribing a number of different IRA credit) but additionally launched or expanded different slender provisions (the low-income housing tax credit score, the brand new markets tax credit score, and the clear gasoline manufacturing credit score, amongst others). It additionally expanded the Alternative Zone program and made it everlasting, and raised the certified small enterprise inventory capital positive factors exclusion.

The opposite facet of the OBBBA that this paper doesn’t cowl, however might be thought-about as the person earnings tax, is the premium tax credit related to the Reasonably priced Care Act marketplaces. The OBBBA makes a number of adjustments to the premium tax credit, most notably proscribing entry to the credit for non-citizens, introducing a extra thorough eligibility verification course of, disallowing the tax credit score for protection enrolled in throughout particular enrollment durations, and eliminating limits to recapture of extra superior premium tax credit.

Premium tax credit, much more than different tax credit, are successfully a type of authorities spending. The overwhelming majority of expenditures related to the premium tax credit are counted as outlays.[48] Nevertheless, it’s on the very least price noting the substantial cumulative fiscal impression of those adjustments: $4.8 billion in 2026 and $184.6 billion from 2025-2034 in deficit discount.

Conclusion

The principle impetus for the OBBBA was the looming expiration of the tax cuts and reforms handed within the TCJA on the finish of 2025. The OBBBA makes most of these adjustments everlasting, which is commendable. Nevertheless, it doesn’t construct on the TCJA’s accomplishments by way of simplification. As a substitute, with the most important exception of reforms to the Inflation Discount Act’s inexperienced power credit, the OBBBA primarily complicates the person tax code, introducing or increasing slender tax breaks for several types of earnings or bills.

The post-OBBBA tax code leaves loads of room for enchancment. For one, many OBBBA provisions must be rolled again sooner or later. And provisions that the OBBBA left untouched, such because the exclusion for employer-sponsored medical health insurance, also needs to be on the desk for future reform.

Whereas the OBBBA itself might not be a tax reform that improves the tax code via simplification, it does sarcastically set the desk for one. Lots of the new provisions are scheduled to run out on the finish of 2028. That second will present the chance to eschew a number of the errors of the OBBBA whereas constructing on the TCJA adjustments it made everlasting.

Keep knowledgeable on the tax insurance policies impacting you.

Subscribe to get insights from our trusted consultants delivered straight to your inbox.

[1] TaxEDU, “Ideas of Sound Tax Coverage,” Tax Basis, https://taxfoundation.org/taxedu/ideas/#simplicity.

[2] TaxEDU, “It Pays to Maintain It Easy,” Tax Basis, https://taxfoundation.org/taxedu/movies/it-pays-to-keep-it-simple/.

[3] Inside Income Service, “1040 (and 1040-SR) Directions,” 2024, https://www.irs.gov/directions/i1040gi.

[4] Sam Cluggish and Alex Muresianu, “Tax Complexity Now Prices the US Financial system over $536 Billion Yearly,” Tax Basis, Aug. 27. 2025, https://taxfoundation.org/knowledge/all/federal/irs-compliance-complexity-tax-costs/.

[5] These numbers have been calculated by taking the hourly burden info supplied by the White Home Workplace of Data and Regulatory Affairs (OIRA) and multiplying them by both the imply hourly wage and advantages for all occupations within the case of particular person earnings taxes or 13-2011 Accountants and Auditors within the case of all different taxes. The imply hourly wages and the typical advantages for personal sector employees have been every taken from the Bureau of Labor Statistics (BLS). The out-of-pocket prices supplied by OIRA have been additionally accounted for within the calculations.

[6] Youssef Benzarti and Luisa Wallossek, “Rising Earnings Tax Complexity,” NBER Working Paper 31944, December 2023, https://www.nber.org/papers/w31944.

[7] Alex Muresianu, “How Did the Tax Cuts and Jobs Act Simplify the Tax Code,” Tax Basis, Aug. 7, 2024, https://taxfoundation.org/weblog/tcja-complexity-compliance/.

[8] Daniel Bunn and Garrett Watson, “All About that Base(line),” Tax Basis, Dec. 5, 2024, https://taxfoundation.org/weblog/extending-tax-cuts-budgetary-impact/.

[9] Erica York and Alex Muresianu, “The Tax Cuts and Jobs Act Simplified the Tax Submitting Course of for Thousands and thousands of Households,” Tax Basis, Aug. 7, 2018, https://taxfoundation.org/analysis/all/federal/the-tax-cuts-and-jobs-act-simplified-the-tax-filing-process-for-millions-of-americans/.

[10] The income impact of this provision is accounted for in a later part of the paper.

[11] Inside Income Service, “2004 1040 Directions,” https://www.irs.gov/pub/irs-prior/i1040–2004.pdf.

[12] Inside Income Service, “1040 (and 1040-SR) Directions, Tax Yr 2024,” https://www.irs.gov/pub/irs-pdf/i1040gi.pdf.

[13] Bureau of Labor Statistics, “Desk 4. Non-public Business Employees by Occupational and Business Group,” March 2025, https://www.bls.gov/information.launch/ecec.t04.htm; Bureau of Labor Statistics, “Occupational Employment and Wage Statistics,” Might 2024, https://knowledge.bls.gov/oesprofile/.

[14] Garrett Watson and Alex Durante, “Troublesome Commerce-Offs Make Coverage Consensus on Little one Tax Credit score Elusive,” Tax Basis, Nov. 10, 2022, https://taxfoundation.org/weblog/child-tax-credit-reform/.

[15] Statistics of Earnings, “Desk A: All Particular person Earnings Tax Returns: Chosen Earnings and Tax Objects in Present and Fixed 1990 {Dollars}, Tax Years 1990-2022,” Inside Income Service.

[16] Statistics of Earnings, “Particular person Earnings Tax Returns Line Merchandise Estimates,” Inside Income Service, https://www.irs.gov/statistics/soi-tax-stats-individual-income-tax-returns-line-item-estimates-publications-4801-and-5385.

[17] Taxpayer Advocate Service, “Repeal the Different Minimal Tax,” August 2013, https://www.taxpayeradvocate.irs.gov/wp-content/uploads/2020/08/2013-ARC_VOL-1_S2-LR-1.pdf.

[18] Scott Greenberg, “Reforming the Cross-By way of Deduction,” Tax Basis, Jun. 21, 2018, https://taxfoundation.org/analysis/all/federal/reforming-pass-through-deduction-199a/.

[19] Scott Hodge and Claire Rock, “Tax Complexity Now Prices the US Financial system Over $546 Billion Yearly,” Tax Basis, Aug. 6, 2024, https://taxfoundation.org/knowledge/all/federal/irs-tax-compliance-costs/.

[20] Garrett Watson and Erica York, “Trump’s ‘No Tax on Extra time Pay’ Proposal Would Distort Work Choices,” Tax Basis, Sep.13, 2024, https://taxfoundation.org/weblog/trump-overtime-tax-exemption/.

[21] Alicia Parlapiano and Andrew Duehren, “An Illustrated Information to Who Actually Advantages From ‘No Tax On Suggestions,’” The New York Instances, Jun. 4, 2025, https://www.nytimes.com/interactive/2025/06/04/upshot/no-tax-on-tips.html.

[22] Inside Income Service, “Credit for New Clear Automobiles Bought in 2023 or After,” IRS, up to date Aug. 3, 2025, https://www.irs.gov/credits-deductions/credits-for-new-clean-vehicles-purchased-in-2023-or-after.

[23] Alex Durante, “How Does the Extra Senior Deduction Examine to No Tax on Social Safety?,” Tax Basis, Jul, 4, 2025, https://taxfoundation.org/weblog/no-tax-on-social-security-senior-tax-deduction/.

[24] Tax Basis Taxes and Progress Mannequin, July 2025.

[25] Alex Durante, “How Does the Extra Senior Deduction Examine to No Tax on Social Safety?”

[26] “Sen. Cruz Introduces the Make investments America Act,” Workplace of Senator Ted Cruz, Might 12, 2025, https://www.cruz.senate.gov/newsroom/press-releases/sen-cruz-introduces-the-invest-america-act.

[27] H.R.1, One Large Stunning Invoice Act.

[28] Ashlea Ebeling, “’Trump Accounts’ for Youngsters Come With $1,000 – and Tax Problems,” The Wall Road Journal, Jul. 15, 2025, https://www.wsj.com/personal-finance/trump-accounts-for-kids-come-with-1-000and-tax-complications-4b75b803; see additionally “Retirement Matters – Exceptions to tax on early distributions,” Inside Income Service, https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-exceptions-to-tax-on-early-distributions.

[29] William McBride, Huaqun Li, Garrett Watson, and Alex Durante, “Simplifying Saving and Enhancing Monetary Safety via Common Financial savings Accounts,” Tax Basis, Might 29, 2024, https://taxfoundation.org/analysis/all/federal/universal-savings-accounts-financial-security/.

[30] Garrett Watson and Claire Rock, “American Retirement and Tax-Most popular Financial savings Accounts, Tax Yr 2018,” Tax Basis, Aug. 14, 2024, https://taxfoundation.org/knowledge/all/federal/401k-ira-retirement-savings-accounts/.

[31] Alan Cole, “The 4 Totally different Methods the Tax Code Treats Saving and Funding,” Tax Basis, Might 24, 2016, https://taxfoundation.org/weblog/four-different-ways-tax-code-treats-saving-and-investment/.

[32] Rick Meyer, “Hidden Gems within the Consolidated Appropriations Act of 2021,” The CPA Journal, February 2021, https://www.cpajournal.com/2021/02/05/hidden-gems-in-the-consolidated-appropriations-act-of-2021/.

[33] Penn-Wharton Finances Mannequin, “New Charitable Deduction within the CARES Act: Budgetary and Distributional Evaluation,” Mar. 27, 2020, https://budgetmodel.wharton.upenn.edu/points/2020/3/27/charitable-deduction-the-cares-act.

[34] Arnav Gurudatt, Garrett Watson, and Will McBride, “Inconsistent Tax Remedy of Scholar Mortgage Debt Forgiveness Creates Confusion,” Tax Basis, Aug. 10, 2023, https://taxfoundation.org/weblog/student-loan-debt-forgiveness/.

[35] IRS, “Kind 2441: Little one and Dependent Care Bills, 2024,” https://www.irs.gov/pub/irs-pdf/f2441.pdf.

[36] Alex Muresianu, “How the One Large Stunning Invoice Modifications Inexperienced Vitality Tax Credit,” Tax Basis, Jul. 31, 2025, https://taxfoundation.org/weblog/big-beautiful-bill-green-energy-tax-credit-changes/.

[37] IRS, “Credit for New Clear Automobiles Bought in 2023 or After,” Inside Income Service, up to date Jul. 8, 2025, https://www.irs.gov/credits-deductions/credits-for-new-clean-vehicles-purchased-in-2023-or-after.

[38] Nicholas Buffie, “The Tax Credit score Exception for Leased Electrical Automobiles,” Congressional Analysis Service, Mar. 1, 2024, https://www.congress.gov/crs-product/IF12603.

[39] Hunt Allcott, Reigner Kane, Maximilian S. Maydanchik, Joseph S. Shapiro, and Felix Tintelnot, “The Results of ‘Purchase American’: Electrical Automobiles and the Inflation Discount Act,” Nationwide Bureau of Financial Analysis Working Paper No. 33032 (Revised December 2024), https://www.nber.org/system/recordsdata/working_papers/w33032/w33032.pdf.

[40] Lujin Zhao, Elizabeth Ottinger, Arthur Hong Chun Yip, and John Paul Helveston, “Quantifying Electrical Car Mileage in the USA,” Joule 7:11 (November 2023), https://www.cell.com/joule/fulltext/S2542-4351(23)00404-X.

[41] IRS, “SOI Tax Stats – Clear Vitality Tax Credit score Statistics,” https://www.irs.gov/statistics/soi-tax-stats-clean-energy-tax-credit-statistics.

[42] Cox Automotive, “Electrical Car Gross sales Mark One other Document in Q3, Because of Larger Incentives, Extra Decisions,” Oct. 11, 2024, https://www.coxautoinc.com/market-insights/q3-2024-ev-sales/.

[43] William McBride, Alex Muresianu, Erica York, and Michael Hartt, ”Inflation Discount Act One Yr After Enactment,” Tax Basis, Aug. 16, 2023, https://taxfoundation.org/analysis/all/federal/inflation-reduction-act-taxes/.

[44] IRS, “Vitality Environment friendly Residence Enchancment Credit score,” up to date Might 29, 2025, https://www.irs.gov/credits-deductions/energy-efficient-home-improvement-credit.

[45] David Feldman, “Photo voltaic Put in System Value Evaluation,” Nationwide Renewable Vitality Laboratory, Apr. 3, 2025, https://www.nrel.gov/photo voltaic/market-research-analysis/solar-installed-system-cost.

[46] IRS, “SOI Tax Stats – Clear Vitality Tax Credit score Statistics.”

[47] Yale Finances Lab, “How Does OBBBA Have an effect on the Time It Takes to File a Tax Return,” Jul. 25, 2025, https://budgetlab.yale.edu/analysis/how-does-obbba-affect-time-it-takes-file-tax-return.

[48] Joint Committee on Taxation, “Estimates of Federal Tax Expenditures for Fiscal Years 2024-2028,” Dec. 11, 2024, https://www.jct.gov/getattachment/765709fb-9a4b-430a-8f9e-4d342ec97f7e/x-48-24.pdf.

Share this text