{kind=link}

Preface to the New Version

The examine earlier than you, which has been printed because the State Enterprise Tax Local weather Index since 2003, was rebranded because the State Tax Competitiveness Index final yr to higher replicate what it assesses: states’ total tax competitiveness, not simply the enterprise tax local weather. This wasn’t simply an train in slapping a brand new title on the duvet and calling it a day. Slightly, we reworked the Index from the bottom as much as make it a greater product.

For greater than 20 years, the Index has helped policymakers consider their tax codes, serving as a street map for reform. Annually, the examine underwent methodological refinements—which we all the time outlined—to seize altering parts of the tax code, just like the introduction of world intangible low-taxed earnings or the design of distant vendor taxes following the Supreme Courtroom’s Wayfair determination. However the tempo of change has been speedy in recent times, with the adoption of the federal Tax Cuts and Jobs Act, the Supreme Courtroom’s Wayfair determination, the rise of distant work and different outgrowths of the worldwide pandemic (together with a roiling of unemployment insurance coverage tax regimes), the adoption of a nation’s-first digital promoting tax, and an rising curiosity in new or expanded taxes on wealth, unrealized positive factors, knowledge, digital merchandise, and extra.

We noticed a necessity to handle these extra comprehensively, and to offer further granularity in our analysis of tax provisions already encompassed by the Index. The previous Index did its job properly. Certainly, unbiased evaluations demonstrated a robust correlation between Index ranks and state financial outcomes. However we needed to increase and refresh the publication earlier than it acquired stale, to remain forward of recent developments in tax. A refresh additionally gave us an opportunity to higher systematize and rebalance the therapy of some outlier state tax provisions that needed to be shoehorned into the methodology of prior editions.

With final yr’s refresh, we did greater than replace the methodology and undertake a brand new identify. We additionally rethought the presentation of the Index’s treasure trove of tax coverage info. The Index’s 150+ variables are not hidden away in appendix tables, and the web publication, previously simply an interactive map accompanied by a prolonged PDF, was reimagined for a digital atmosphere.

Now, every state receives its personal abstract, highlighting a number of of essentially the most notable options of its tax code and explaining why it ranks because it does on the Index—together with some state-specific reforms that might enhance its tax competitiveness. And customers now have entry to interactive, sortable, filterable datasets. We invite you to discover. See your state’s coverage decisions on each variable within the Index. Add one other state or two and examine them. Or drill all the way down to a single variable or set of variables and see how all states carry out on them.

That is the second yr below the brand new methodology, however in case you’re evaluating our rankings this yr to previous editions from 2024 or earlier than, you would possibly discover that some ranks have shifted a bit greater than we often see from yr to yr. A few of that, in fact, is just because states have been extremely busy just lately, adopting important adjustments to their tax codes. However a few of it is because of our methodological adjustments.

To make sure an apples-to-apples comparability, and within the curiosity of transparency, we have now backcast states’ rankings below the brand new methodology going again six years previous to this present version. These are the controlling rankings, and are those that ought to be cited to point out precise motion by states in recent times. That is nothing new: we’ve all the time backcast to account for methodological revisions. What’s completely different this yr is the scope of the change, as we’ve added extra variables and made extra changes than in prior years.

Readers within the particulars of what has modified are invited to learn on to study our revised methodology, and for explanations of our variables. Most readers, nevertheless, will probably want to soar forward to the general rankings, their state’s web page, or the newly interactive datasets.

For all readers, we hope that the 2026 State Tax Competitiveness Index will function a helpful information for navigating state tax coverage. It ranks, each total and throughout 5 subindices—particular person earnings taxes, company taxes, gross sales and excise taxes, property and wealth taxes, and unemployment insurance coverage taxes—how states compete, and the place every has room to enhance. And for would-be reformers, our datasets (now far more accessible!) are a useful information to how states construction their tax codes, and the place they diverge—for good and for sick—from their friends.

Even a great street map, nevertheless, shouldn’t be all the time a enough substitute for a information. That’s why the Tax Basis has a workforce of state tax consultants whose main objective is to assist educate policymakers and the general public. As all the time, we invite you to succeed in out together with your questions. That’s why we’re right here.

Jared Walczak

Vice President of State Initiatives, Tax Basis

Government Abstract

The Tax Basis’s State Tax Competitiveness Index allows policymakers, taxpayers, and enterprise leaders to gauge how their states’ tax techniques examine. Whereas there are lots of methods to point out how a lot state governments gather in taxes, the Index evaluates how properly states construction their tax techniques and offers a street map for enchancment.

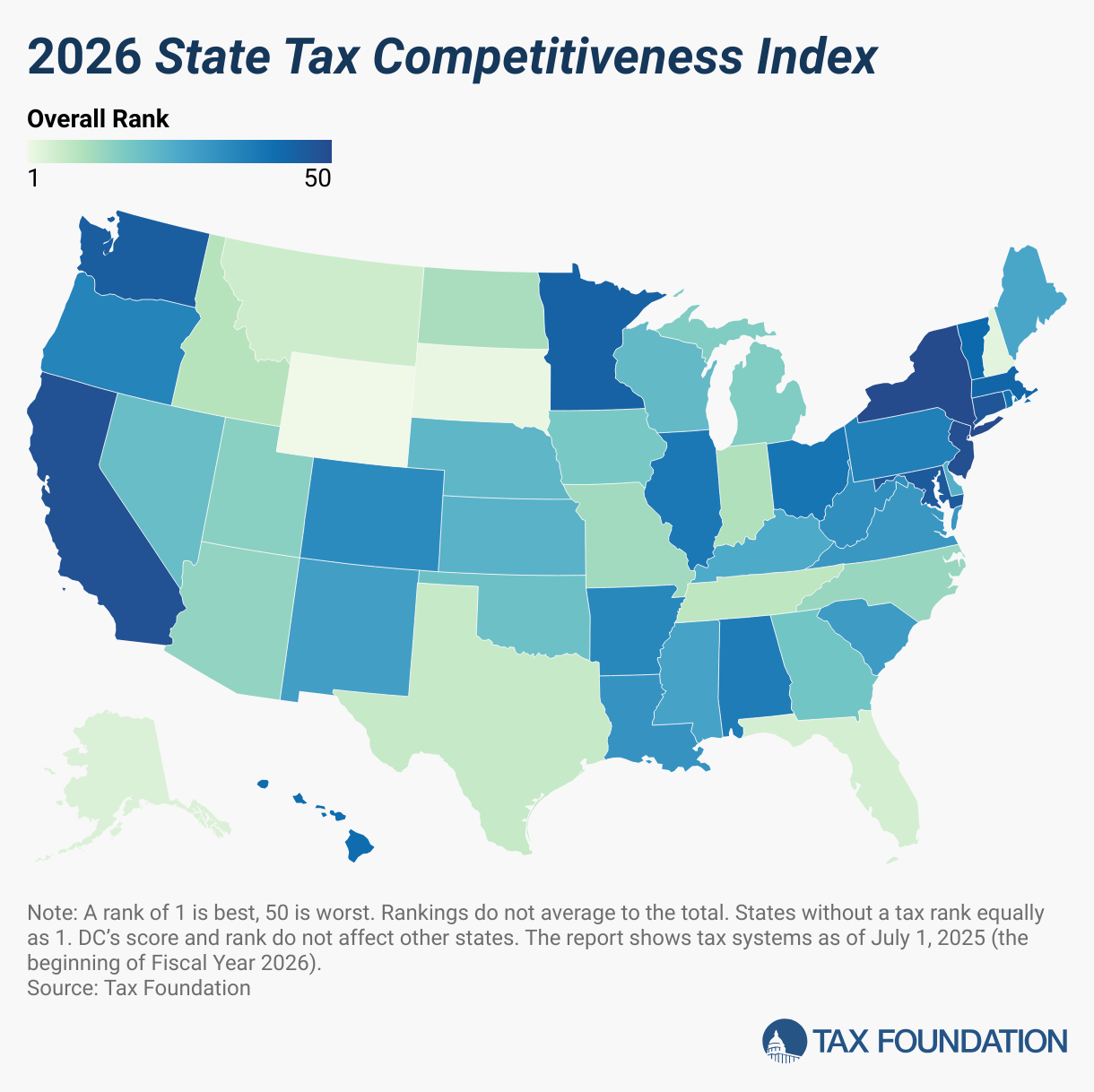

The ten finest states on this yr’s Index are:

- Wyoming

- South Dakota

- New Hampshire

- Alaska

- Florida

- Montana

- Texas

- Tennessee

- Idaho

- Indiana

The absence of a serious tax is a typical issue amongst most of the prime 10 states. Property taxes and unemployment insurance coverage taxes are levied in each state, however there are a number of states that do with out a number of of the most important taxes: the company earnings taxA company earnings tax (CIT) is levied by federal and state governments on enterprise income. Many corporations usually are not topic to the CIT as a result of they’re taxed as pass-through companies, with earnings reportable below the person earnings tax., the particular person earnings taxA person earnings tax (or private earnings tax) is levied on the wages, salaries, investments, or different types of earnings a person or family earns. The U.S. imposes a progressive earnings tax the place charges improve with earnings. The Federal Earnings Tax was established in 1913 with the ratification of the sixteenth Modification. Although barely 100 years previous, particular person earnings taxes are the biggest supply, or the gross sales tax. South Dakota and Wyoming haven’t any company or particular person earnings tax; Alaska and New Hampshire haven’t any particular person earnings or state-level gross sales tax; Florida, Tennessee, and Texas haven’t any particular person earnings tax; and Montana has no gross sales tax.

This doesn’t imply, nevertheless, {that a} state can not rank properly whereas nonetheless levying all the most important taxes. Idaho and Indiana, for instance, levy all the most important tax sorts, as do all the opposite states that rank 11th to 16th: North Dakota, North Carolina, Missouri, Arizona, Utah, and Michigan.

The ten lowest-ranked, or worst, states on this yr’s Index are:

- Hawaii

- Vermont

- Massachusetts

- Minnesota

- Washington

- Maryland

- Connecticut

- California

- New Jersey

- New York

The states within the backside 10 are likely to have plenty of points in frequent: complicated, nonneutral taxes with comparatively excessive charges. New Jersey, for instance, is hampered by among the highest property taxA property tax is primarily levied on immovable property like land and buildings, in addition to on tangible private property that’s movable, like automobiles and gear. Property taxes are the one largest supply of state and native income within the U.S. and assist fund colleges, roads, police, and different companies. burdens within the nation, has the highest-rate company earnings tax within the nation, and has one of many highest-rate particular person earnings taxes. Moreover, the state has a very aggressive therapy of worldwide earnings, levies an inheritance taxAn inheritance tax is levied upon the worth of inherited belongings obtained by a beneficiary after a decedent’s dying. To not be confused with property taxes, that are paid by the decedent’s property primarily based on the dimensions of the whole property earlier than belongings are distributed, inheritance taxes are paid by the recipient or inheritor primarily based on the worth of the bequest obtained., and maintains among the nation’s worst-structured particular person earnings taxes.

2026 State Tax Competitiveness Index Ranks and Part Tax Ranks

Word: A rank of 1 is finest, 50 is worst. Rankings don’t common to the whole. States with no tax rank equally as 1. DC’s rating and rank don’t have an effect on different states. The report reveals tax techniques as of July 1, 2025 (the start of fiscal yr 2026).

Supply: Tax Basis.

Understanding the Index and Tax Competitors

Tax competitors is just a little like WAR—not battle, however Wins Above Substitute. The time period comes from baseball, the place it’s supposed as a sabermetric statistic to measure what number of extra wins a workforce can declare on account of a particular participant above the quantity that might be generated by a replacement-level participant. It’s a lot the identical approach in public finance: a well-structured tax code gained’t make the Wyoming Basin a metropolis, nor will poor tax construction make Manhattan a ghost city. However tax construction does play a job in a state’s financial successes or failures, and infrequently a considerable one. Each state can profit from a easy, impartial, clear, pro-growth tax construction.

The Index scores states throughout 5 subindices, every representing a serious element of state tax codes: company taxes, particular person earnings taxes, gross sales and excise taxes, property and wealth taxes, and unemployment insurance coverage taxes. Slightly than weighting every subindex equally, their weight is set in line with the variance throughout states in every class, which has the impact of assigning extra weight to areas the place states have extra alternatives wherein to compete.

After all, it’s tough to introduce any structural flaws to the design of a tax one doesn’t impose, so some states, by forgoing a tax altogether (the person earnings tax, the company earnings tax, or the gross sales tax) rating completely on a subindex or some portion of 1. That is why states like Wyoming and South Dakota, which each forgo earnings taxes, accomplish that properly on the Index. States that may keep away from imposing a number of of the most important taxes both must lean very closely on the opposite main tax sorts (which might imply decrease rankings on these parts), select to function on leaner budgets, make the most of pure sources like oil and fuel, or have demographics (like Florida) the place different taxes can generate a shocking quantity of income.

In different phrases, the Wyoming mannequin might not be potential in some states—however the Idaho, Indiana, and North Carolina fashions are. These states all rank within the prime 13 on the Index whereas imposing the entire main taxes, however at average charges with comparatively well-designed tax constructions.

For taxpayers, the Index is an efficient place to begin for understanding how their state compares to its friends. However for policymakers and others occupied with learn how to enhance the construction of their state’s tax code, it’s greater than that: it’s a helpful diagnostic software, with tables that permit readers to check their state to its friends on a variety of things—tax charges, sure, but in addition throwback guidelines, the therapy of web working losses, recapture provisions, indexation, spit roll taxation, comfort guidelines, expensing, and far more.

Should you saddled South Dakota with New York’s tax code, the state would wrestle. Individuals are clearly prepared to pay a premium to stay in New York—on actual property, on shopper purchases, and sure, on taxes. However there are limits, to say nothing of the truth that a system that’s bearable in Manhattan could also be significantly extra burdensome in Syracuse. And even in states like New York tax burdens, and tax constructions, matter.

Taxes usually are not all the things, however they do matter, and they’re inside the management of policymakers. Even inside a given income goal, there are higher and worse methods to boost income.

The Index measures tax construction, not all the opposite issues companies care about, like an informed workforce, high quality of life, proximity to related markets, and even the climate—and a few of these issues contain trade-offs. Taxes, nevertheless, are an necessary a part of the combo, and modernizing a state’s tax construction helps place it for progress. States that rank higher on the Index have better-structured tax codes, and states with better-structured tax codes get Wins Above Substitute.

Notable Adjustments in This 12 months’s Index

Delaware

Delaware fell 4 locations total (to 24th) as different states applied substantial reforms whereas Delaware largely stood nonetheless. Delaware is hampered by being one in every of solely two states to impose each earnings taxes and a state-level gross receipts taxGross receipts taxes are utilized to an organization’s product sales, with out deductions for a agency’s enterprise bills, like compensation, prices of products offered, and overhead prices. In contrast to a gross sales tax, a gross receipts tax is assessed on companies and applies to transactions at each stage of the manufacturing course of, resulting in tax pyramiding., and by having a relatively low unemployment belief fund solvency ratio, amongst different elements.

Georgia

Georgia’s company earnings tax and particular person earnings tax charges continued to section down in 2025, with each declining from 5.39 to five.19 %. These charges will proceed to lower within the coming years if the state meets sure income objectives. The speed reductions drove a 3-spot enchancment within the state’s company earnings rank, a 1-place enchancment in its particular person earnings tax rank, and an enchancment from 23rd to 18th total. Though it didn’t enhance the property tax rank, Georgia additionally elevated its tangible private property tax de minimis exemption from a low $7,500 to a extra beneficiant $20,000.

Idaho

Idaho, which has applied a variety of reforms in recent times, lowered its now-flat particular person and company earnings tax charges from 5.695 to five.3 % in 2025, boosting it two further locations on the Index, transferring from 11th to 9th total.

Indiana

Indiana’s state particular person earnings tax price decreased from 3.05 to three % in 2025, however rising native earnings tax charges, paired with price reductions in different states—together with Louisiana, which additionally adopted a 3 % single-rate earnings tax in 2025—noticed Indiana’s total rank fall barely, from 9th to 10th. Future deliberate price reductions to 2.9 % ought to assist the Hoosier State, if not offset by additional earnings tax will increase on the native degree.

Illinois

Illinois added world intangible low-taxed earnings (GILTI) to its tax base, which has since transitioned to a tax on web CFC-tested earnings (NCTI) on the federal degree on account of adjustments below the One Massive Lovely Invoice Act (OBBBA). This transformation lowered Illinois’ rating on our Index, however not sufficient to vary its rank.

Iowa

Iowa improved two locations on the Index, from 19th to 17th total, because the state applied a flat 3.8 % particular person earnings tax in 2025. This represents the continuation of a number of years of ongoing reforms which have seen a dramatic enchancment in Iowa’s rankings. The state’s company tax element rank slid as different states made enhancements, however the deliberate consolidation of the state’s company earnings tax bracketsA tax bracket is the vary of incomes taxed at given charges, which usually differ relying on submitting standing. In a progressive particular person or company earnings tax system, charges rise as earnings will increase. There are seven federal particular person earnings tax brackets; the federal company earnings tax system is flat. right into a 5.5 % single-rate tax will additional enhance Iowa’s rankings within the coming years.

Louisiana

Louisiana improved six ranks on the 2026 Index, with additional enchancment anticipated in subsequent yr’s version, on account of reforms adopted in a late 2024 particular session centered on tax competitiveness. Lawmakers enacted sweeping reform, which included a brand new flat particular person earnings tax price of three %, a company earnings tax price of 5.5 %, and everlasting full expensingFull expensing permits companies to right away deduct the total value of sure investments in new or improved know-how, gear, or buildings. It alleviates a bias within the tax code and incentivizes corporations to take a position extra, which, in the long term, raises employee productiveness, boosts wages, and creates extra jobs.. These reforms improved Louisiana from 32nd to fifteenth on the person earnings tax element of the Index and from 29th to 10th on the company tax element. In 2026, the state’s franchise (capital inventory) tax might be repealed, and Louisiana will conform to odd therapy of S companies reasonably than requiring them to file as C companies, each of which is able to yield significant additional enchancment within the state’s Index rank.

Maine

Maine improved from 31st to 26th, primarily on account of a decline in property tax collections as a share of non-public earnings at a time when most states noticed important will increase in property tax collections on account of hovering assessed values insufficiently offset by mill levy (price) reductions.

Maryland

Maryland adopted the nation’s most aggressive package deal of tax will increase in 2025. Lawmakers added two further tax brackets on excessive earners, yielding a prime marginal particular person earnings tax price of 6.5 %, whereas additionally growing the cap on county earnings tax charges to three.3 %. The state additionally established a 2 % surtax on excessive earners’ capital positive factors, and imposed a brand new alternate-rate 3 % gross sales tax on knowledge, IT, and different business-to-business digital companies. These adjustments dropped Maryland from 45th to 46th total, sliding one place on the person earnings tax element (from 46th to 47th) and 5 locations on the gross sales tax element (from 35th to 40th).

Michigan

Michigan’s total rank slid two locations, partially on account of new focused company incentives however largely from price competitors in different states, with a number of—significantly Georgia, Idaho, Louisiana, Nebraska, and Utah—decreasing particular person and company earnings tax charges whereas Michigan didn’t.

Montana

Montana slid one place on the 2026 Index, from 5th to sixth. The state applied a tiered property tax construction with completely different charges making use of relying on the worth of the property, successfully shifting the tax burden reasonably than offering significant reduction. Concurrently, New Hampshire leapfrogged Montana and a number of other different high-ranking states on the Index with the repeal of its tax on curiosity and dividend earnings.

Nebraska

Though the state lowered its prime marginal particular person earnings tax price to five.2 %, Nebraska retained its total place of twenty-twond on the Index. In 2026, the person earnings tax price will lower from 4.99 %, and the company price might be trimmed to 4.55 %, with additional reductions scheduled for 2027.

New Hampshire

New Hampshire joined the ranks of states with out a person earnings tax with the elimination of its curiosity and dividends (I&D) tax on January 1, 2025. In consequence, New Hampshire improved three locations total and 12 locations on the person earnings tax element.

New Mexico

New Mexico minimize towards broader nationwide developments in enacting a company earnings tax improve by eliminating the good thing about a 4.8 % decrease price and taxing all company earnings at 5.9 %, however the state’s two-place slide within the Index was not pushed by this coverage change, however reasonably by enhancements within the tax constructions of competitor states.

Ohio

Ohio improved two locations, from 35th to 33rd, on the person earnings tax element because the state’s prime particular person earnings tax price declined from 3.5 % to three.125 %. Nevertheless, whereas that is among the many decrease prime charges amongst income-taxing states, Ohio municipalities and faculty districts additionally possess particular person earnings tax authority, yielding a lot larger mixed charges than could be indicated by state charges alone. Subsequent yr, Ohio’s two remaining particular person earnings tax charges might be consolidated because the state adopts a flat-rate 2.75 % earnings tax.

Oregon

For the second yr in a row, Oregon’s rank dropped on account of aggressive reforms in different states as Oregon stood nonetheless. On the time of publication, Oregon lawmakers have been contemplating adjustments in conformity to the federal Inner Income Code that would additional hurt the state’s tax competitiveness in future years.

Pennsylvania

In recent times, Pennsylvania has adopted significant reforms to its company earnings tax system, together with aligning its beforehand stingy web working loss (NOL) carryforwards with federal requirements and phasing in reductions to the company earnings tax price, which as soon as stood at 9.99 %. In 2025, the company price fell from 8.49 to 7.99 %, with future 0.5 share level reductions scheduled till the speed reaches 4.99 %. Pennsylvania improved 4 locations on the company tax element with this yr’s price discount.

Rhode Island

Rhode Island’s web working loss (NOL) carryforward interval was elevated from 5 to twenty years, efficient January 1, 2025, bettering its company tax element rating by three locations. Moreover, the state just lately elevated its gas and cigarette excise tax charges, hurting its gross sales and excise tax rating. Nevertheless, Rhode Island’s total rating didn’t change.

South Carolina

As half of a bigger finances invoice, South Carolina quickly lowered its prime particular person earnings tax price from 6.2 % to six %, efficient July 1, 2025, and lasting till July 1, 2026. Nevertheless, this variation didn’t drive an enchancment within the state’s particular person earnings or total scores on account of motion from different states.

Utah

Utah lawmakers proceed to implement incremental reductions within the state’s particular person and company earnings tax charges. The reductions in 2025, from 4.55 to 4.5 % for each taxes, have been sufficient to enhance Utah’s total Index rank from 16th to fifteenth.

Washington

In Washington, lawmakers applied a brand new 9.9 % price on the capital positive factors taxA capital positive factors tax is levied on the revenue constituted of promoting an asset and is usually along with company earnings taxes, incessantly leading to double taxation. These taxes create a bias towards saving, resulting in a decrease degree of nationwide earnings by encouraging current consumption over funding. , inflicting the state to slip two locations on the person earnings tax element of the Index. The state’s prime property tax price—already tied for the nation’s highest—was additionally elevated from 20 to 35 %. Nonetheless, a number of tax will increase in Maryland resulted in Washington swapping locations with it and bettering by one rank. Washington’s adoption of recent gross sales taxes on enterprise purchases of digital merchandise, together with digital promoting, went into impact on October 1, after the July 1, 2025, snapshot date of this Index, however will have an effect on Washington’s rank in future editions.

Forthcoming Adjustments and Adjustments Not But Mirrored

Connecticut

Connecticut’s capital inventory tax price continued to drop in 2025, from 0.26 % to 0.21 %. Whereas this small discount didn’t have an effect on its property tax or total rankings, the state will see extra motion on subsequent yr’s Index when it phases out the tax fully in 2026.

Florida

Florida accomplished the repeal of its industrial lease tax efficient October 2025. This uncommon tax shouldn’t be scored on the Index, however its elimination represents an enchancment within the state’s total tax competitiveness.

Kansas

Throughout the 2025 legislative session, Kansas legislators overrode the governor’s veto of a invoice to section in a low, flat particular person earnings tax price, in addition to to cut back the state’s company earnings tax and privilege tax charges over time, topic to income triggers and Price range Stabilization Fund situations. These adjustments will take impact in future years, with the timing of such adjustments topic to varied situations being met.

Kentucky

Kentucky’s particular person earnings tax price might be lowered from 4 to three.5 % on January 1, 2026, which is able to enhance the Commonwealth’s particular person earnings tax element rating. This transformation is the results of a triggered tax discount regulation that was initially adopted in 2022, in addition to policymakers’ proactive approval in 2025 of laws to permit the forthcoming triggered discount to take impact.

Louisiana

As a part of a reform package deal already adopted, Louisiana’s franchise (capital inventory) tax might be repealed in 2026, and the state will conform to odd therapy of S companies reasonably than requiring them to file as C companies, each of which is able to yield significant additional enchancment within the state’s Index rank.

Ohio

Subsequent yr, Ohio is slated to implement a flat-rate 2.75 % state particular person earnings tax. Whereas municipal and faculty district earnings taxes nonetheless contribute considerably to the general earnings tax burden in Ohio, this forthcoming change will enhance Ohio’s rating in subsequent editions of the Index.

Oklahoma

In 2025, lawmakers adopted a brand new spherical of particular person earnings tax reforms, lowering the highest marginal price to 4.5 %, consolidating six brackets into three, and offering fiscal safeguards for future triggered price reductions. These adjustments take impact in 2026 and might be mirrored within the subsequent version of the Index.

Washington

Throughout the 2025 legislative session, Washington lawmakers enacted SB 5814, increasing the gross sales tax base to embody a variety of enterprise digital automated companies, together with digital promoting. These adjustments went into impact on October 1, 2025, after the July 1 snapshot date of the present Index, and might be mirrored in subsequent editions.

Wisconsin

Included in Wisconsin’s finances for the 2025-27 biennium is a provision that retroactively lowered particular person earnings tax collections, beginning in tax yr 2025, by growing the quantity of marginal earnings at which Wisconsin’s second-highest earnings tax price kicks in, widening the second-lowest earnings tax bracket. Whereas this variation will cut back particular person earnings tax collections, its constructive financial results might be restricted because it doesn’t cut back the highest marginal price. This transformation was adopted on July 3, 2025, after the snapshot date for the 2026 Index, so the adjustments to Wisconsin’s particular person earnings tax brackets might be mirrored in subsequent yr’s Index tables.

State Tax Competitiveness Index (2020-2026)

Word: A rank of 1 is finest, 50 is worst. All scores are for fiscal years. DC’s rating and rank don’t have an effect on different states.

Supply: Tax Basis.

Introduction

Taxation is inevitable, however the specifics of a state’s tax construction matter significantly. The measure of whole taxes paid is related, however different parts of a state tax system may improve or hurt the competitiveness of a state’s enterprise atmosphere. The State Tax Competitiveness Index distills many complicated concerns to an easy-to-understand rating.

The fashionable market is characterised by cellular capital and labor, with all forms of companies, small and enormous, tending to find the place they’ve the best aggressive benefit. The proof reveals that states with the perfect tax techniques would be the best at attracting new companies and handiest at producing financial and employment progress. It’s true that taxes are however one consider enterprise decision-making. Different considerations additionally matter–resembling entry to uncooked supplies or infrastructure or a talented labor pool–however a easy, wise tax system can positively impression enterprise operations with regard to those sources. Moreover, in contrast to adjustments to a state’s health-care, transportation, or training techniques, which might take a long time to implement, adjustments to the tax code can rapidly enhance a state’s competitiveness.

You will need to keep in mind that even in our world economic system, states’ stiffest competitors usually comes from different states. The Division of Labor experiences that almost all mass job relocations are from one US state to a different reasonably than to a international location.[1] Definitely, job creation is speedy abroad, as beforehand underdeveloped nations enter the world economic system, although within the aftermath of federal tax reform, US companies not face the third-highest company tax price on this planet, however reasonably one according to averages for industrialized nations.[2] State lawmakers are proper to be involved about how their states rank within the world competitors for jobs and capital, however they should be extra involved with corporations transferring from Detroit, Michigan, to Dayton, Ohio, than from Detroit to New Delhi, India. Because of this state lawmakers should concentrate on how their states’ enterprise climates match up towards their speedy neighbors and to different regional competitor states.

Anecdotes concerning the impression of state tax techniques on enterprise funding are plentiful. In Illinois within the early 2000s, a whole bunch of hundreds of thousands of {dollars} of capital investments have been delayed when then-Governor Rod Blagojevich (D) proposed a hefty gross receipts tax.[3] Solely when the legislature resoundingly defeated the invoice did the funding resume. In 2005, California-based Intel determined to construct a multibillion-dollar chip-making facility in Arizona on account of its favorable company earnings tax system.[4] In 2010, Northrup Grumman selected to maneuver its headquarters to Virginia over Maryland, citing the higher enterprise tax local weather.[5] In 2015, Basic Electrical and Aetna threatened to decamp from Connecticut if the governor signed a finances that might improve company tax burdens, and Basic Electrical really did so.[6] Anecdotes resembling these reinforce what we all know from financial principle: taxes matter to companies, and people locations with essentially the most aggressive tax techniques will reap the advantages of business-friendly tax climates.

Tax competitors is an disagreeable actuality for state income and finances officers, however it’s an efficient restraint on state and native taxes. When a state imposes larger taxes than a neighboring state, companies will cross the border to some extent. Subsequently, states with extra aggressive tax techniques rating properly within the Index as a result of they’re finest suited to generate financial progress.

State lawmakers are aware of their states’ tax competitiveness, however they’re typically tempted to lure companies with profitable tax incentives and subsidies as a substitute of broad-based tax reform. This is usually a harmful proposition, as the instance of Dell Computer systems and North Carolina illustrates. North Carolina agreed to $240 million price of incentives to lure Dell to the state. Lots of the incentives got here within the type of tax credit from the state and native governments. Sadly, Dell introduced in 2009 that it will be closing the plant after solely 4 years of operations.[7] A 2007 USA TODAY article chronicled related issues different states have had with corporations that obtain beneficiant tax incentives.[8]

Lawmakers make these offers below the banner of job creation and financial improvement, however the reality is that if a state wants to supply such packages, it’s almost definitely overlaying for an undesirable enterprise tax local weather. A much more efficient strategy is the systematic enchancment of the state’s enterprise tax local weather for the long run to enhance the state’s competitiveness. When assessing which adjustments to make, lawmakers want to recollect two guidelines:

- Taxes matter to enterprise. Enterprise taxes have an effect on enterprise choices, job creation and retention, plant location, competitiveness, the transparency of the tax system, and the long-term well being of a state’s economic system. Most significantly, taxes diminish income. If taxes take a bigger portion of income, that value is handed alongside to both shoppers (via larger costs), staff (via decrease wages or fewer jobs), shareholders (via decrease dividends or share worth), or some mixture of the above. Thus, a state with decrease tax prices might be extra enticing to enterprise funding and extra more likely to expertise financial progress.

- States don’t enact tax adjustments (will increase or cuts) in a vacuum. Each tax regulation will in a roundabout way change a state’s aggressive place relative to its speedy neighbors, its area, and even globally. Finally, it’ll have an effect on the state’s nationwide standing as a spot to stay and to do enterprise. Entrepreneurial states can make the most of the tax will increase of their neighbors to lure companies out of high-tax states.

To some extent, tax-induced financial distortions are a reality of life, however policymakers ought to try to maximise the events when companies and people are guided by enterprise ideas and decrease these instances the place financial choices are influenced, micromanaged, and even dictated by a tax system. The extra riddled a tax system is with politically motivated preferences, the much less probably it’s that enterprise choices might be made in response to market forces. The Index rewards these states that decrease tax-induced financial distortions.

Rating the competitiveness of fifty very completely different tax techniques presents many challenges, particularly when a state dispenses with a serious tax totally. Ought to Indiana’s tax system, which incorporates three comparatively impartial taxes on gross sales, particular person earnings, and company earnings, be thought of kind of aggressive than Alaska’s tax system, which features a significantly burdensome company earnings tax however no statewide tax on particular person earnings or gross sales?

The Index offers with such questions by evaluating the states on greater than 150 variables within the 5 main areas of taxation (company taxes, particular person earnings taxes, gross sales and excise taxes, unemployment insurance coverage taxes, and property and wealth taxes) after which including the outcomes to yield a ultimate, total rating. This strategy rewards states on significantly robust points of their tax techniques (or penalizes them on significantly weak points), whereas measuring the overall competitiveness of their total tax techniques. The result’s a rating that may be in comparison with different states’ scores. Finally, each Alaska and Indiana rating properly.

Literature Evaluation

Economists haven’t all the time agreed on how people and companies react to taxes. As early as 1956, Charles Tiebout postulated that if residents have been confronted with an array of communities that supplied differing types or ranges of public items and companies at completely different prices or tax ranges, then all residents would select the neighborhood that finest glad their explicit calls for, revealing their preferences by “voting with their ft.” Tiebout’s article is the seminal work on the subject of how taxes have an effect on the placement choices of taxpayers.

Tiebout advised that residents with excessive calls for for public items would focus in communities with excessive ranges of public companies and excessive taxes, whereas these with low calls for would select communities with low ranges of public companies and low taxes. Competitors amongst jurisdictions leads to quite a lot of communities, every with residents who all worth public companies equally.

Nevertheless, companies type out the prices and advantages of taxes otherwise from people. For companies, which could be extra cellular and should earn income to justify their existence, taxes cut back profitability. Theoretically, companies could possibly be anticipated to be extra responsive than people to the lure of low-tax jurisdictions. Analysis means that companies interact in “yardstick competitors,” evaluating the prices of presidency companies throughout jurisdictions. Shleifer (1985) first proposed evaluating regulated franchises to be able to decide effectivity. Salmon (1987) prolonged Shleifer’s work to have a look at subnational governments. Besley and Case (1995) confirmed that “yardstick competitors” impacts voting habits, and Bosch and Sole-Olle (2006) additional confirmed the outcomes discovered by Besley and Case. Tax adjustments which can be out of sync with neighboring jurisdictions will impression voting habits. In a current examine, De Paula et al. (2025) discovered that the character of tax competitors amongst US states adjustments over time and that “financial” neighbors could play an much more necessary function in tax-setting habits than geographic neighbors.

The financial literature over the previous 60 years has slowly cohered round this speculation. Ladd (1998) summarizes the post-World Struggle II empirical tax analysis literature in a wonderful survey article, breaking it down into three distinct durations of differing concepts about taxation: (1) taxes don’t change habits; (2) taxes could or could not change enterprise habits relying on the circumstances; and (3) taxes positively change habits.

Interval one, excluding Tiebout, included the Nineteen Fifties, Nineteen Sixties, and Seventies and is summarized succinctly in three survey articles: Due (1961), Oakland (1978), and Wasylenko (1981). Due’s was a polemic towards tax giveaways to companies, and his analytical strategies consisted of fundamental correlations, interview research, and the examination of taxes relative to different prices. He discovered no proof to assist the notion that taxes affect enterprise location. Oakland was skeptical of the assertion that tax differentials on the native degree had no affect in any respect. Nevertheless, as a result of econometric evaluation was comparatively unsophisticated on the time, he discovered no important outcomes to assist his instinct. Wasylenko’s survey of the literature discovered among the first proof indicating that taxes do affect enterprise location choices. Nevertheless, the statistical significance was decrease than that of different elements, resembling labor provide and agglomeration economies. Subsequently, he dismissed taxes as a secondary issue at most.

Interval two was a short transition in the course of the early to mid-Eighties. This was a time of nice ferment in tax coverage as Congress handed main tax payments, together with the so-called Reagan tax minimize in 1981 and a dramatic reform of the federal tax code in 1986. Articles revealing the financial significance of tax coverage proliferated and have become extra subtle. For instance, Wasylenko and McGuire (1985) prolonged the normal enterprise location literature to nonmanufacturing sectors and located, “Greater wages, utility costs, private earnings tax charges, and a rise within the total degree of taxation discourage employment progress in a number of industries.” Nevertheless, Newman and Sullivan (1988) nonetheless discovered a combined bag in “their statement that important tax results [only] emerged when fashions have been fastidiously specified.”

Ladd was writing in 1998, so her “interval three” began within the late Eighties and continued as much as 1998, when the amount and high quality of articles elevated considerably. Articles that match into interval three start to floor as early as 1985, as Helms (1985) and Bartik (1985) put forth forceful arguments primarily based on empirical analysis that taxes information enterprise choices. Helms concluded {that a} state’s means to draw, retain, and encourage enterprise exercise is considerably affected by its sample of taxation. Moreover, tax will increase considerably retard financial progress when the income is used to fund switch funds. Bartik concluded that the traditional view that state and native taxes have little impact on enterprise is fake.

Papke and Papke (1986) discovered that tax differentials amongst places could also be an necessary enterprise location issue, concluding that persistently excessive enterprise taxes can symbolize a hindrance to the placement of business. Apparently, they use the identical kind of after-tax mannequin utilized by Tannenwald (1996), who reaches a special conclusion.

Bartik (1989) offers robust proof that taxes have a damaging impression on enterprise start-ups. He finds particularly that property taxes, as a result of they’re paid no matter revenue, have the strongest damaging impact on enterprise. Bartik’s econometric mannequin additionally predicts tax elasticities of -0.1 to -0.5 that suggest a ten % minimize in tax charges will improve enterprise exercise by 1 to five %. Bartik’s findings, in addition to these of Mark, McGuire, and Papke (2000), and ample anecdotal proof of the significance of property taxes, buttress the argument for inclusion of a property index dedicated to property-type taxes within the Index.

By the early Nineteen Nineties, the literature had expanded sufficiently for Bartik (1991) to determine 57 research on which to base his literature survey. Ladd succinctly summarizes Bartik’s findings:

The big variety of research permitted Bartik to take a special strategy from the opposite authors. As a substitute of dwelling on the outcomes and limitations of every particular person examine, he checked out them within the combination and in teams. Though he acknowledged potential criticisms of particular person research, he convincingly argued that some systematic flaw must minimize throughout all research for the consensus outcomes to be invalid. In placing distinction to earlier reviewers, he concluded that taxes have fairly giant and important results on enterprise exercise.

Ladd’s “interval three” absolutely continues to today. Agostini and Tulayasathien (2001) examined the consequences of company earnings taxes on the placement of international direct funding in US states. They decided that for “international traders, the company tax price is essentially the most related tax of their funding determination.” Subsequently, they discovered that international direct funding was fairly delicate to states’ company tax charges. Extra just lately, Agostini (2007) introduced additional proof that international direct funding in manufacturing is delicate to adjustments in state company tax charges, and likewise confirmed that the apportionment components performs a key function in figuring out the efficient tax price confronted by companies and considerably influences the placement of international direct funding.

Mark, McGuire, and Papke (2000) discovered that taxes are a statistically important consider private-sector job progress. Particularly, they discovered that private property taxes and gross sales taxes have economically giant damaging results on the annual progress of personal employment.

Harden and Hoyt (2003) level to Phillips and Gross (1995) as one other examine contending that taxes impression state financial progress, they usually assert that the consensus amongst current literature is that state and native taxes negatively have an effect on employment ranges. Harden and Hoyt conclude that the company earnings tax has essentially the most important damaging impression on the speed of progress in employment.

Gupta and Hofmann (2003) regressed capital expenditures on quite a lot of elements, together with weights of apportionment formulation, the variety of tax incentives, and burden figures. Their mannequin lined 14 years of knowledge and decided that companies are likely to find property in states the place they’re topic to decrease earnings tax burdens. Moreover, Gupta and Hofmann counsel that throwback necessities are essentially the most influential on the placement of capital funding, adopted by apportionment weights and tax charges, and that investment-related incentives have the least impression.

Current analysis focuses on the connection between tax coverage and entrepreneurship. Curtis and Decker (2018) examine the consequences of various tax constructions on new agency exercise and discover that new agency employment is considerably and negatively affected by state company earnings tax charges, however not by particular person earnings or gross sales tax charges. The authors conclude that younger companies are extra aware of adjustments in state company taxes than extra mature companies. This discovering is according to the outcomes from a big cross-national examine (Djankov et al., 2010), which concludes {that a} 10 share level improve within the efficient company tax price reduces entry of recent companies by 17.5 %.

One other strand of analysis focuses on the tax therapy of capital funding. Chirinko and Wilson (2008) doc a rising significance of funding tax credit in state company tax codes. They discover that capital formation in a state is elevated by tax-induced reductions within the value of capital and is lowered by related reductions in competitor states. Particularly, the authors show that the variety of manufacturing institutions round state borders is larger on the facet of the border with the cheaper price of capital.

In a later paper, Chirinko and Wilson (2023) discover that the consequences of job creation tax credit are smaller within the quick run (that means these credit are much less efficient as a countercyclical software) and extra significant in the long term (implying they are often efficient as an financial improvement software). Nevertheless, Jolley et al. (2015), of their survey of enterprise executives in North Carolina, discover that these executives typically desire tax reductions to selective tax incentives, no matter whether or not their agency really obtained any incentives from the state. The Index favors broad-based reduction over focused jobs incentives.

Different economists have discovered that taxes on particular merchandise can produce behavioral outcomes related to people who have been present in these normal research. For instance, Fleenor (1998) appeared on the impact of excise tax differentials between states on cross-border buying and the smuggling of cigarettes. Moody and Warcholik (2004) examined the cross-border results of beer excises. Their outcomes, supported by the literature in each instances, confirmed important cross-border buying and smuggling between low-tax states and high-tax states.

Fleenor discovered that buying areas sprouted in counties of low-tax states that shared a border with a high-tax state, and that roughly 13.3 % of the cigarettes consumed in the USA throughout FY 1997 have been procured through some kind of cross-border exercise. Equally, Moody and Warcholik discovered that in 2000, 19.9 million instances of beer, on web, moved from low- to high-tax states. This amounted to some $40 million in gross sales and excise tax income misplaced in high-tax states.

Though the literature has largely congealed round a normal consensus that taxes are a considerable issue within the decision-making course of for companies, disputes stay, and a few students are unconvinced.

Based mostly on a considerable overview of the literature on enterprise climates and taxes, Wasylenko (1997) concludes that taxes don’t seem to have a considerable impact on financial exercise amongst states. Nevertheless, his conclusion is premised on there being few important variations in state tax techniques. He concedes that high-tax states will lose financial exercise to common or low-tax states “so long as the elasticity is damaging and considerably completely different from zero.” Certainly, he approvingly cites a State Coverage Reviews article that finds that the highest-tax states have acknowledged that prime taxes could also be accountable for the low charges of job creation in these states.[9]

Wasylenko’s rejoinder is that policymakers routinely overestimate the diploma to which tax coverage impacts enterprise location choices and that on account of this misperception, they reply readily to public stress for jobs and financial progress by proposing decrease taxes. In keeping with Wasylenko, different legislative actions are more likely to accomplish extra constructive financial outcomes as a result of in actuality, taxes don’t drive financial progress.

Nevertheless, there may be ample proof that states compete for companies utilizing their tax techniques. A notable instance comes from Illinois, the place in early 2011 lawmakers handed two main tax will increase. The person earnings tax price elevated from 3 % to five %, and the company earnings tax price rose from 7.3 % to 9.5 %.[10] The outcome was that many companies threatened to depart the state, together with some very high-profile Illinois corporations resembling Sears and the Chicago Mercantile Trade. By the top of the yr, lawmakers had minimize offers with each companies, totaling $235 million over the following decade, to maintain them from leaving the state.[11]

Funderburg et al. (2013) examine the consequences of state and native enterprise taxes on worth added in 15 manufacturing sectors throughout a subset of states and discover {that a} 10 % discount in tax legal responsibility on new funding corresponds to a 3.5–5.3 % improve in worth added by the manufacturing sector. These estimates symbolize the upper finish of the vary present in prior analysis (Bartik 1991; Wasylenko 1997).

Giroud and Rauh (2019) use microdata on multistate companies to estimate the impression of state taxes on enterprise exercise and discover that C company employment and institutions have short-run company tax elasticities of -0.4 to -0.5, whereas pass-through entities present elasticities of -0.2 to -0.4. Because of this, for every percentage-point improve within the price, employment decreases by 0.4 to 0.5 % for C companies topic to the company earnings tax, and by 0.2 to 0.4 % inside pass-through companies topic to the person earnings tax.

Chow et al. (2022) discover that state company earnings taxes considerably have an effect on companies’ choices on the place to find their headquarters, an necessary consideration for each companies and states. Particularly, they discover {that a} 1 share level improve within the company earnings tax price raises the probability of companies relocating their headquarters out of the state by 16.8 %, whereas a corresponding lower lowers that probability by 9.1 %. This outcome enhances the broader literature (usually carried out in a federal or worldwide context) which reveals that lowering the efficient company earnings tax price results in larger capital funding, decrease debt (Ohrn 2018), and elevated entrepreneurial exercise, together with that financed by international direct funding (Djankov et al. 2010).

A brand new literature overview, Kleven et al. (2020), summarizes current proof for tax-driven migration. Whereas the empirical outcomes reviewed on this article are context-specific and don’t all the time present a major relationship between taxes and migration, there’s a normal consensus that high-income people are significantly delicate to tax will increase, each internationally and inside nations. Particularly, inventors, entrepreneurs, sport stars, and billionaires have been proven to be extremely cellular inside the USA and aware of main earnings and property tax adjustments (Moretti and Wilson 2017; Akcigit et al. 2022; Moretti and Wilson 2023; Agrawal and Tester 2024).

Rauh and Shyu (2024) analyze Proposition 30 in California, which elevated the highest marginal earnings tax price by three share factors in 2012, and show that prime earners reported $321,000–$436,000 much less in taxable earnings within the first three years following the reform—about 10 % of their baseline earnings of $4.15 million—in response to this main tax improve. Additionally they present that there was a significant outmigration impact, which elevated with earnings and was concentrated amongst prime earners. Collectively, these responses eroded roughly 61 % of the potential windfall tax income from Proposition 30 inside two years of the reform.

Measuring the Impression of Tax Differentials

Some current contributions to the literature on state taxation criticize enterprise and tax local weather research basically.[12] Authors of such research contend that comparative experiences just like the State Tax Competitiveness Index don’t have in mind these elements that straight impression a state’s enterprise local weather. Nevertheless, a cautious examination of those criticisms reveals that the authors imagine taxes are unimportant to companies and due to this fact dismiss the research as merely being designed to advocate low taxes.

Peter Fisher’s Grading Locations: What Do the Enterprise Local weather Rankings Actually Inform Us? now printed by Good Jobs First, criticizes 4 indices: The U.S. Enterprise Coverage Index printed by the Small Enterprise and Entrepreneurship Council, Beacon Hill’s Competitiveness Report, the American Legislative Trade Council’s Wealthy States, Poor States, and the earlier model of the examine. The primary version additionally critiqued the Cato Institute’s Fiscal Coverage Report Card and the Financial Freedom Index by the Pacific Analysis Institute. Within the report’s first version, printed earlier than Fisher summarized his objections: “The underlying downside with the … indexes, in fact, is twofold: none of them really do an excellent job of measuring what it’s they declare to measure, and they don’t, for essentially the most half, got down to measure the best issues to start with” (Fisher 2005). Within the second version, he recognized three overarching questions: (1) whether or not the indices included related variables, and solely related variables; (2) whether or not these variables measured what they purport to measure; and (3) how the index combines these measures right into a single index quantity (Fisher 2013). Fisher’s main argument is that if the indexes did what they presupposed to do, then all 5 would rank the states equally.

Fisher’s conclusion holds little weight as a result of the 5 indices serve such dissimilar functions, and every group has a special space of experience. There isn’t a motive to imagine that the Tax Basis’s Index, which relies upon totally on state tax legal guidelines, would rank the states in the identical or related order as an index that features crime charges, electrical energy prices, and well being care (the Small Enterprise and Entrepreneurship Council’s Small Enterprise Survival Index), or toddler mortality charges and the proportion of adults within the workforce (Beacon Hill’s State Competitiveness Report), or constitution colleges, tort reform, and minimal wage legal guidelines (the Pacific Analysis Institute’s Financial Freedom Index).

The Tax Basis’s State Tax Competitiveness Index is an indicator of which states’ tax techniques are essentially the most hospitable to financial progress. The Index doesn’t purport to measure financial alternative or freedom, and even the broad enterprise local weather, however reasonably tax competitiveness, and its variables replicate this focus. We accomplish that not solely as a result of the Tax Basis’s experience is in taxes, however as a result of each element of the Index is topic to speedy change by state lawmakers. It’s on no account clear what the perfect plan of action is for state lawmakers who wish to thwart crime, for instance, both within the quick or long run, however they will change their tax codes now. Opposite to Fisher’s Seventies view that the consequences of taxes are “small or non-existent,” our examine displays robust proof that enterprise choices are considerably impacted by tax concerns.

Though Fisher doesn’t really feel tax climates are necessary to states’ financial progress, different authors contend the alternative. Bittlingmayer, Eathington, Corridor, and Orazem (2005) discover of their evaluation of a number of enterprise local weather research {that a} state’s tax local weather does have an effect on its financial progress price and that a number of indices are capable of predict progress, and that this examine’s predecessor “explains progress persistently.” This discovering was confirmed by Anderson (2006) in a examine for the Michigan Home of Representatives, and extra just lately by Kolko, Neumark, and Mejia (2013), who, in an evaluation of the flexibility of 10 enterprise local weather indices to foretell financial progress, concluded that this examine’s predecessor, State Enterprise Tax Local weather Index, yielded “constructive, sizable, and statistically important estimates for each specification” they measured, and particularly cited the Index as one in every of two enterprise local weather indices (out of 10) with significantly robust and sturdy proof of predictive energy. Neumark and Muz (2016) discover that robust efficiency on tax-and-cost-related indices (together with the predecessor of this Index) is certainly related to larger financial progress, however it could even be linked to elevated earnings inequality—highlighting potential trade-offs in tax coverage.

Surfield and Reddy (2016) use ranks from this examine’s predecessor and one other index to look at the consequences of enterprise local weather on job losses within the manufacturing sector. They discover that states with extra aggressive company tax codes expertise fewer unemployment insurance coverage claims, whereas states that underutilize their gross sales taxes are likely to have extra such claims. The authors attribute the latter impact to the likelihood that decrease gross sales tax income limits a state’s means to fund different public sector areas (resembling training and infrastructure) that assist a constructive manufacturing local weather. It may be {that a} larger reliance on gross sales taxes incessantly entails a decrease reliance on much less economically environment friendly, extra capital-intensive taxes. Bittlingmayer et al. additionally discovered that relative tax competitiveness issues, particularly on the borders, and due to this fact, indices that place a excessive premium on tax insurance policies do a greater job of explaining progress. Additionally they noticed that research centered on a single subject do higher at explaining financial progress at borders. Lastly, the article concludes that a very powerful parts of the enterprise local weather are tax and regulatory burdens on enterprise (Bittlingmayer et al. 2005). These findings assist the argument that taxes impression enterprise choices and financial progress, they usually assist the validity of the Index.

Fisher and Bittlingmayer et al. maintain opposing views concerning the impression of taxes on financial progress. Fisher finds assist from Robert Tannenwald, previously of the Boston Federal Reserve, who argues that taxes usually are not as necessary to companies as public expenditures. Tannenwald compares 22 states by measuring the after-tax price of return to money stream of a brand new facility constructed by a consultant agency in every state. This very completely different strategy makes an attempt to compute the marginal efficient tax price of a hypothetical agency and yields outcomes that make taxes seem trivial.

The taxes paid by companies ought to be a priority to everybody as a result of they’re in the end borne by people via decrease wages, elevated costs, and decreased shareholder worth. States don’t institute tax coverage in a vacuum. Each change to a state’s tax system makes its enterprise tax local weather kind of aggressive in comparison with different states and makes the state kind of enticing to enterprise. Finally, anecdotal and empirical proof, together with the cohesion of current literature across the conclusion that taxes matter an amazing deal to enterprise, present that the Index is a vital and useful gizmo for policymakers who wish to make their states’ tax techniques welcoming to enterprise.

Methodological Adjustments

The State Tax Competitiveness Index (STCI) is the successor to the State Enterprise Tax Local weather Index (SBTCI), which was printed by the Tax Basis from 2003 to 2023. Persevering with within the custom of its predecessor, the brand new Index assesses state tax competitiveness and the soundness of states’ tax codes. Whereas it maintains the identical normal construction because the previous Index, it incorporates significant methodological adjustments geared toward making a extra clear and trendy strategy to evaluating state tax competitiveness. No methodological adjustments have been adopted between the 2025 and 2026 editions of the Index, however an outline of the variations between the SBTCI and the STCI is supplied beneath.

What Remained the Identical

Just like the SBTCI, the State Tax Competitiveness Index comprises 5 main parts:

- Company Taxes (consists of company earnings taxes and gross receipts taxes)

- Particular person Earnings Taxes

- Gross sales, Use, and Excise Taxes

- Property and Wealth Taxes

- Unemployment Insurance coverage Taxes

Every element, as earlier than, has two equally weighted subindices: the speed subindex and the bottom subindex. The place relevant, each state and common native tax charges are used to evaluate the state’s tax competitiveness. Nevertheless, parts usually are not weighted equally. As a substitute, every element is weighted primarily based on the variability (commonplace deviation) of the 50 states’ scores from the imply. This leads to a heavier weighting of parts with higher variability. Historically, particular person earnings taxes and gross sales taxes have had the very best weights, whereas unemployment insurance coverage taxes have had the bottom weight. This stays true within the new Index.

Different weighting schemes, resembling equal weights or weights primarily based on the revenue-generating significance of a tax, are potential, however sensitivity assessments present they produce comparatively related outcomes. For instance, the correlation between the precise Index ranks and people utilizing equal weights is about 0.85, with most states within the prime 10 and backside 10 retaining their ranks. Nevertheless, we imagine the present weighting scheme higher displays the significance of tax competitors and offers stronger rewards and penalties in areas the place competitors for human, bodily, and monetary capital is most intense.

What Modified

Company Taxes

Since company earnings taxes and gross receipts taxes are essentially completely different techniques for taxing companies, we assess them individually, with every now receiving a 50-percent weight in each the speed and base subindices. Within the earlier model of the Index, gross receipts taxes have been underweighted in comparison with company earnings taxes, particularly within the base subindex, with explicit challenges arising within the two states (Delaware and Oregon) that impose each company earnings and gross receipts taxes on the state degree.

Moreover, important adjustments have been made to the therapy of web working losses and their respective deductions. Since carryforward provisions are far more necessary than carryback provisions within the federal tax code, we now assign an 80-percent weight to carryforwards and a 20-percent weight to carrybacks when assessing web working loss deductions. Each provisions assist companies pay taxes primarily based on their common, reasonably than annual, profitability. Nevertheless, carrybacks are hardly ever utilized by states and performance equally to carryforwards. A beneficiant carryforward interval (of 20 years or above) with no statutory greenback cap now permits a state to attain extremely on the bottom subindex, even when it doesn’t provide a carryback. This differs from the previous Index, the place carryback therapy was given higher weight, and the place conformity to federal therapy was assessed on par with essentially the most beneficiant state-specific carryforward therapy reasonably than assessing the discrete parts (carryforward interval and carryforward cap) individually.

Particular person Earnings Taxes

Within the price subindex, the highest price variable now consists of the state’s prime marginal earnings tax price and the typical native earnings tax price within the two largest jurisdictions. Beforehand, we used the typical native earnings tax price within the largest jurisdiction and the state capital. Our new strategy notably impacts states like Pennsylvania and Kentucky, the place the biggest cities are likely to have the very best native earnings tax charges. The speed subindex now features a new variable that displays the progressivity of the person earnings tax price construction. This variable is calculated by dividing the state’s prime marginal earnings tax price by the marginal price for joint filers with a median family earnings (which varies by state). The upper the ratio, the higher the progressivity of the speed construction and the stronger the inducement for prime earners to contemplate relocating to different jurisdictions. The speed subindex provides equal weight to the highest price variable and the progressivity index, which accounts for the speed construction’s progressivity, the variety of brackets, the highest tax bracket threshold, and earnings recapture.

The bottom subindex, along with beforehand used marriage penaltyA wedding penalty is when a family’s total tax invoice will increase due to a few marrying and submitting taxes collectively. A wedding penalty usually happens when two people with related incomes marry; that is true for each high- and low-income {couples}., indexation, double taxationDouble taxation is when taxes are paid twice on the identical greenback of earnings, no matter whether or not that’s company or particular person earnings., different minimal tax, Part 179 expensing, and different variables, now consists of the submitting and withholdingWithholding is the earnings an employer takes out of an worker’s paycheck and remits to the federal, state, and/or native authorities. It’s calculated primarily based on the quantity of earnings earned, the taxpayer’s submitting standing, the variety of allowances claimed, and any further quantity the worker requests. threshold index. This variable assesses states’ particular person earnings tax submitting and withholding necessities for nonresidents who carry out a restricted quantity of labor within the state. States that rating properly on this variable present significant submitting and withholding reduction to most nonresidents who spend a restricted period of time working within the state.

Gross sales and Excise Taxes

The speed subindex now consists of each the overall state and native gross sales tax price index and the excise tax index, weighted at 75 % and 25 %, respectively, to roughly replicate the revenue-generating potential of those taxes. The excise tax index, along with beforehand included taxes on gasoline, diesel, tobacco, beer, and distilled spirits, now incorporates the vape tax price, reflecting the rising significance of this tax. Moreover, if the state imposes a digital promoting tax (at present solely Maryland, though Washington has handed an promoting tax that might be in impact for the following version of the Index), it’s penalized by as much as 15 % of the rating on this subindex, relying on the tax price.

The bottom subindex now accounts for a number of further enterprise inputs, items, and companies, significantly within the digital area. The Index has historically penalized states for taxing manufacturing equipment, uncooked supplies, farm gear, workplace gear, industrial utilities, and data companies, amongst others. Now, the class of enterprise inputs has been expanded to incorporate software-as-a-service (SaaS), platform-as-a-service (PaaS), payroll companies, and different business-to-business digital items. Taxing these new business-to-business transactions results in tax pyramidingTax pyramiding happens when the identical ultimate good or service is taxed a number of instances alongside the manufacturing course of. This yields vastly completely different efficient tax charges relying on the size of the availability chain and disproportionately harms low-margin companies. Gross receipts taxes are a major instance of tax pyramiding in motion. and ought to be prevented. Closing consumption items and companies, which could possibly be used for modest base broadening (and for which states are rewarded within the Index), now embody e-books and digital video.

Property and Wealth Taxes

The speed subindex, as earlier than, consists of the efficient property tax price index and the capital inventory tax index. We now use property taxes paid as a share of non-public earnings as the only real measure of the efficient property tax burden. We eliminated the per capita property tax collections variable for simplicity, as the 2 variables have been extremely collinear (with a correlation coefficient of 0.94), and there was restricted justification for utilizing each.

The bottom subindex now offers a extra complete therapy of tangible private property (TPP) taxation. Along with the dummy variable indicating whether or not the state taxes one of these property (as earlier than, states are penalized for doing so), we now account for the prevalence and measurement of TPP de minimis exemptions, which decrease compliance prices for small and medium-sized companies (states are rewarded for having larger de minimis exemptions). Moreover, as a substitute of utilizing dummy variables for property and inheritance taxes (the place states have been penalized for having these taxes whatever the price), we now examine most property and inheritance tax charges and penalize states with larger bequest tax charges.

Unemployment Insurance coverage Taxes

The largest adjustments have occurred within the price subindex. When assessing precise UI tax charges, we at the moment are factoring within the interplay between minimal and most UI tax charges and the taxable wage base in every state. These interactions present a extra exact estimate of the whole tax burden on various kinds of companies. Primarily, we now penalize low-rate states if their taxable wage base is considerably larger than the federal degree of $7,000. Equally, we penalize high-rate states, however the measurement of the penalty will increase with the taxable wage base. For instance, a state with a most UI tax price of 10 % and a taxable wage base of $20,000 would carry out in addition to a state with a most UI tax price of 5.4 % and a taxable wage base of $37,000.

Moreover, the speed subindex now accounts for efficient tax burdens as estimated by the US Division of Labor. We’re utilizing two variables—employer contribution charges as a share of taxable wages and whole wages—as a part of our precise UI tax price evaluation. States with comparatively low values for these variables (e.g., Alabama or Virginia) don’t overburden employers with excessive efficient UI tax charges, in contrast to states with comparatively excessive values (e.g., Hawaii and Pennsylvania).

The speed subindex now additionally accounts for the solvency of a state’s UI belief fund. When these funds turn out to be bancrupt (as within the instances of California and New York), states should borrow from the federal authorities after which discover methods to repay these federal loans, both by issuing bonds or elevating different taxes. There’s a really helpful degree of solvency, and we now reward states with larger ranges of UI belief fund solvency whereas penalizing these with bancrupt UI belief funds. This helps make sure that states are rewarded for making a secure UI tax atmosphere, reasonably than imposing artificially low UI taxes throughout expansionary durations and counting on surcharges and price will increase throughout financial downturns.

The precise UI tax price now performs a serious function within the price subindex (60 %), adopted by the potential UI tax price (20 %) and UI belief fund solvency (20 %).

The bottom subindex nonetheless makes use of the identical main variables as earlier than, together with the expertise ranking components utilized in a state, a number of forms of charging strategies and advantages excluded from charging, and different smaller parts of the bottom, such because the solvency tax, taxes for socialized prices, reserve taxes, and voluntary contributions. We adjusted a number of weights inside the base subindex to simplify the UI tax element of the Index and make it extra clear.

Methodology

The Tax Basis’s State Tax Competitiveness Index has a hierarchical construction constructed from 5 parts:

- Particular person Earnings Taxes

- Gross sales and Excise Taxes

- Company Taxes

- Property and Wealth Taxes

- Unemployment Insurance coverage Taxes

Utilizing the financial literature as our information, we designed these 5 parts to attain every state’s tax competitiveness on a scale of 0 (worst) to 10 (finest). Every element is dedicated to a serious space of state taxation and consists of quite a few tax price and tax base variables. General, there are 154 variables measured on this report.

The 5 parts usually are not weighted equally, as they’re in some indices. Slightly, every element is weighted primarily based on the variability of the 50 states’ scores from the imply. The usual deviation of every element is calculated and a weight for every element is created from that measure. The result’s a heavier weighting of these parts with higher variability. The weighting of every of the 5 main parts is:

- 31.8% — Particular person Earnings Taxes

- 21.2% — Gross sales and Excise Taxes

- 21.1% — Company Taxes

- 14.5% — Property and Wealth Taxes

- 11.4% — Unemployment Insurance coverage Taxes

This improves the explanatory energy of the State Tax Competitiveness Index as an entire as a result of parts with larger commonplace deviations are these areas of tax regulation the place some states have important aggressive benefits. Companies which can be evaluating states for brand spanking new or expanded places should give higher emphasis to tax climates when the variations are giant. However, parts wherein the 50 state scores are clustered collectively—intently distributed across the imply—are these areas of tax regulation the place companies usually tend to de-emphasize tax elements of their location choices.

For instance, Delaware is understood to have a major benefit in gross sales tax competitors, as a result of its tax price of zero attracts companies and buyers from all around the Mid-Atlantic area. That benefit and its drawing energy improve each time one other state raises its gross sales tax. Texas, in the meantime, goes with out particular person or company earnings taxes, although it does impose an uncompetitive “margins” tax on gross receipts. When different states’ earnings taxes rise, the Texas benefit turns into extra alluring.

In distinction with this variability in state earnings and gross sales tax charges, unemployment insurance coverage tax techniques are comparatively related across the nation, so a small change in a single state’s regulation may change its element rating dramatically—however, because of the Index’s weights, with solely a modest impression on total ranks.

Inside every element are two equally weighted subindices dedicated to measuring the impression of the tax charges and the tax bases. Every subindex consists of a number of dummy or scalar variables. Dummy variables, which might take the values of 0 or 1, describe numerous binary tax provisions (e.g., whether or not a state indexes its particular person earnings tax brackets for inflation or affords particular job or R&D credit to companies), whereas scalar variables describe tax charges, tax progressivity, efficient tax burdens (within the property and unemployment insurance coverage tax parts), and different categorical or discrete tax provisions.

Relative Versus Absolute Indexing

The State Tax Competitiveness Index is designed as a relative index reasonably than an absolute or preferrred index. In different phrases, every variable is ranked relative to the variable’s vary in different states. The relative scoring scale is from 0 to 10, with zero that means not “worst potential” however reasonably worst among the many 50 states.

Many states’ tax charges are so shut to one another that an absolute index wouldn’t present sufficient details about the variations among the many states’ tax techniques, particularly for pragmatic enterprise house owners and people who wish to know which states have the perfect tax system in every area.